Markets

Markets

Mahindra & Mahindra in the fast lane on higher capex, upcoming launches

, seven battery electric vehicles (BEVs) and seven light commercial vehicles (LCVs) by 2030. (Photo: AP)")

Summary

- A robust product pipeline comprising both internal combustion engine (ICE) models and EVs, planned capex of ₹37,000 crore over the next three years and targeted capacity expansion to 72,000 units per month by FY26-end would be the key drivers for the homegrown auto major.

Personal finance gurus often advice ‘buy stocks, not products of companies.’ Mahindra & Mahindra Ltd (M&M) is a case in point. If you had resisted the urge to buy a gleaming new sport utility vehicle (SUV) from the Mahindra stable one year ago, and had invested the sum instead in M&M’s shares, you would have doubled your money by now. While M&M has expanded its portfolio to cater to India’s SUV-crazy car market, investors looking to make similar outsized gains hereon are likely to be disappointed. Still, analysts are upbeat about the company’s prospects.

A robust product pipeline, comprising internal combustion engine (ICE) and electric vehicle (EV) models, a planned capital expenditure (capex) of ₹37,000 crore over the next three years, and targeted capacity expansion to 72,000 units per month by the end of FY26 (up from 49,000 per month in FY24) are the key drivers for the homegrown auto major.

M&M's increased focus on EVs is evident from its planned auto capex of ₹27,000 crore, with as much as ₹12,000 crore allocated for EVs. The company plans to launch nine ICE SUVs, seven battery electric vehicles (BEVs), and seven light commercial vehicles (LCVs) by 2030.

Also Read | For EV makers, the lithium price crash should be good news. It isn’t.

In FY25, the management is bullish on the upcoming five-door Thar and therecently-launched XUV 3XO compact SUV, which received 50,000 bookings in just 60 minutes. M&M is producing 9,000 units of this model per month and plans to increase it to 10,500 soon. In the compact SUV segment, the company is in the fifth position, and aims to be among the top two following the launch of 3XO.

“We see M&M’s production ramp up improving in FY25 along with new model launches. We also see M&M offering a differentiated BEV as a near-term catalyst, helping it build on its success amongst the urban affluent customer base," BNP Paribas said in a note.

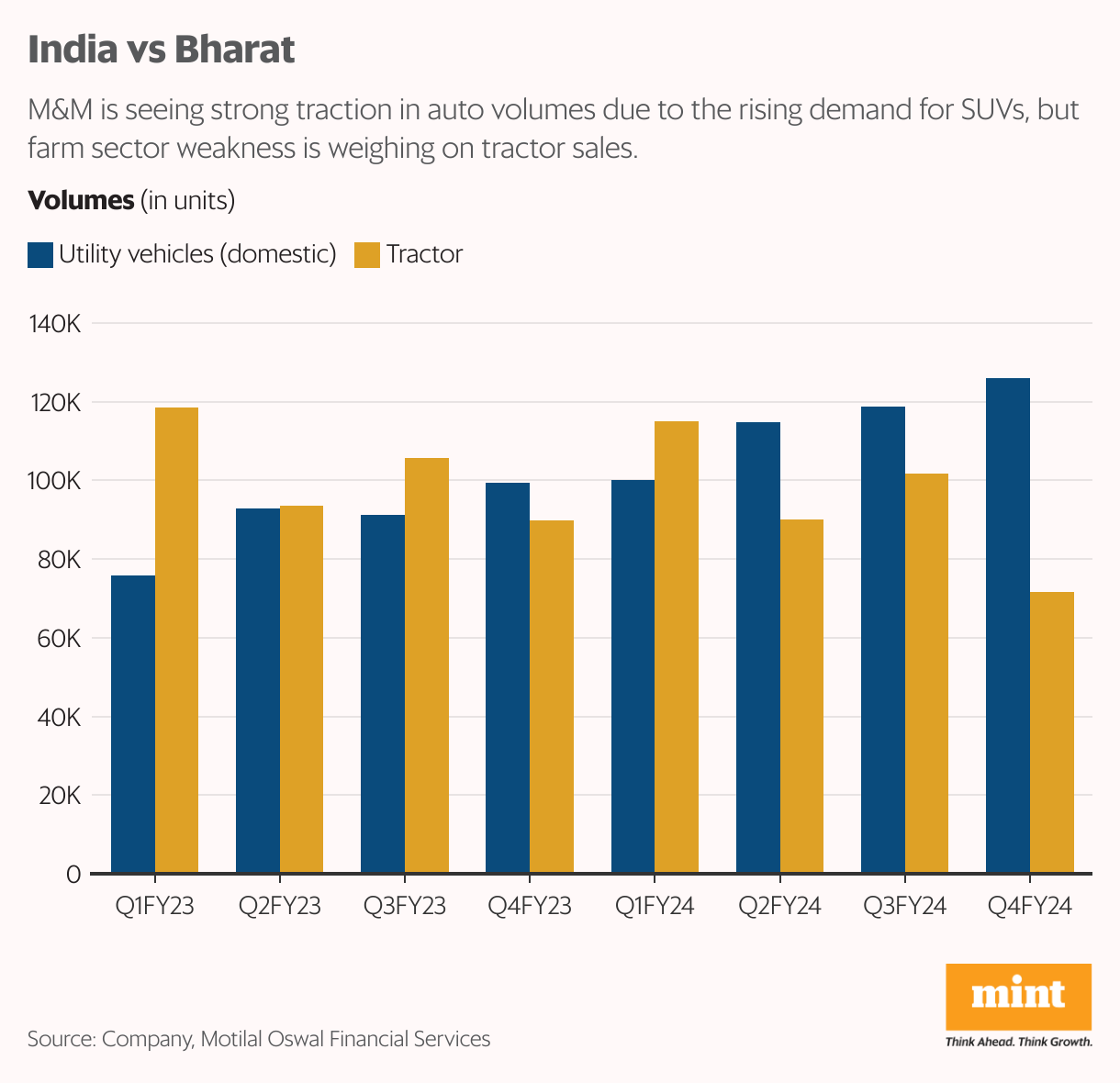

M&M has projected UV sales volume growth of mid-to high-teens in FY25. It has an order backlog of 220,000 units.

The company maintained its numero uno position in SUV revenue market share at 20.4%, up 80 basis points (bps) year-on-year during the March quarter (Q4FY24). Ebitda margin, at 12.9% (up 10 bps sequentially), beat consensus estimates, helped by 50 bps sequential rise in Ebit margin in the auto segment. In FY24, tractor industry volumes fell by 7% as the rural market remained under pressure. Despite this, M&M gained market share of 40 bps to reach 41.6%.

Ebitda is short for earnings before interest, taxes, depreciation, and amortization, while Ebit is earnings before interest and taxes.

In FY25, a revival in the rural sector, aided by India Meteorological Department (IMD)’s forecast of an ‘above normal’ monsoon, and expectations of higher farm sector allocation post-elections, can be additional catalysts.

“We continue to remain bullish on M&M as it should benefit from increasing its presence in high growth category, encouraging response from consumers..., capacity expansion to reduce the waiting period and timely execution of new products, diversification of powertrains and recovery in tractor volume along with strong sustainable margin," said a report by Prabhudas Lilladher.

The management said commodity prices should remain benign over the coming quarters, while better operating leverage and cost cutting initiatives shall keep the margin profile steady. M&M’s operational profile may be kicking into top gear, but that does not mean investors should expect a smooth ride. The sharp 35% rally in the last two months is making many analysts skeptical about the near-term upside left for the stock, which hit a new 52-week high of ₹2,557.95 on Friday.

“The impressive hit rate on new SUV products and the better-than-expected tractor demand recovery, we feel, is well captured by stock rerating in the last two months...With the 1-year forward P/E and P/BV valuations adjusted for subsidiaries’ value inching near +2 standard deviations above the 10-year mean, we remain cautious and retain HOLD rating on the stock," InCred Equities said.