FMCG companies in choppy waters, and there doesn't seem to be any respite soon

companies put on a muted volume show in the three months ended December (Q3FY24) despite it being a festive quarter. (Photo: Mint)")

Investors in the stocks of fast-moving consumer goods companies are treading cautiously, with no big triggers for demand reviving in the near-term.

For consumer staples companies, it will be a while before the choppy waters calm down. Not only is demand for packaged consumer goods weak in rural markets, but there's stress in urban markets as well.

Companies selling fast-moving consumer goods (FMCG) put on a muted volume show in the three months ended December (Q3FY24) despite it being a festive quarter.

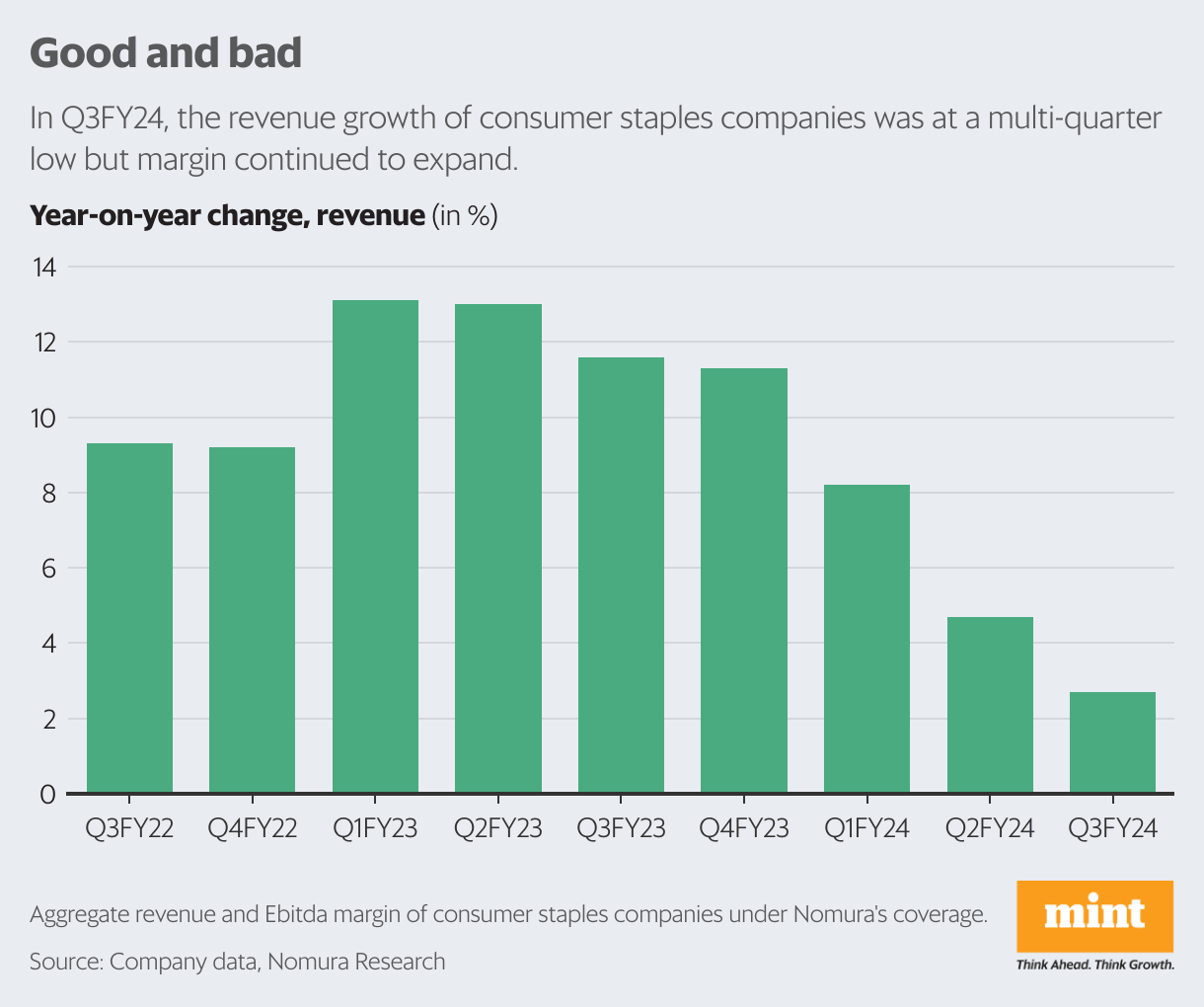

Rural growth continues to lag urban. Overall, the FMCG industry volume growth stood at 6.4% year-on-year in Q3 versus 8.6% in Q2, said Mihir Shah, an analyst at Nomura Financial Advisory and Securities (India) in a report. However, on an absolute basis, volume consumption has remained at the same level in the past three quarters, said Shah.

Specifically, things were a tad different for Dabur India Ltd as it saw comparatively better rural demand. Still, this does not imply that a rural recovery is on the cards as Dabur’s rural growth comes on the back of distribution expansion.

In general, the benign commodity cost environment meant increasing competition from local players in some categories. This means muted volume performance coupled with price cuts impacted revenue.

The aggregate Q3 revenue growth of FMCG companies under Nomura’s coverage stood at 2.7%, the lowest in nine quarters at least. The path ahead hinges entirely on volume performance as the room for price hikes appears narrow.

Hindustan Unilever Ltd (HUL) expects price growth to be slightly negative if the costs of commodities remain where they are.

Besides, competition would have a bearing on the market share of the listed FMCG companies.

From Antique Stock Broking’s latest on-ground interactions, the broking firm notes that the competitive intensity is high in biscuits, foods, detergents and soaps thus resulting in higher price cuts and promotional activities. This means stress for HUL and Britannia Industries Ltd.

In fact, HUL expects the quantum of businesses winning market shares to drop in the coming quarters from the levels of 60% seen in December.

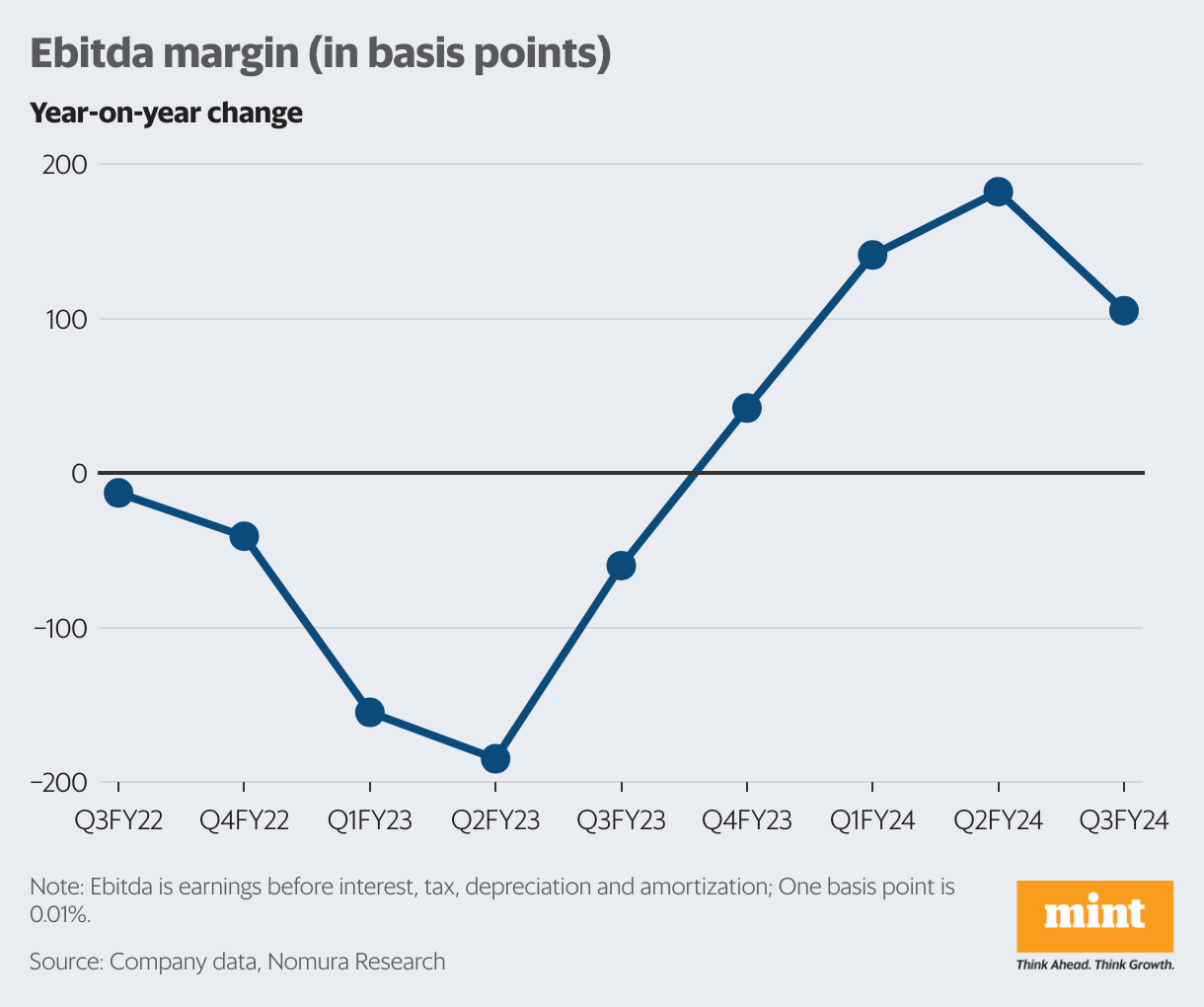

On the bright side, FMCG companies continued to see margin expansion despite product price cuts. But with companies stepping up their advertising and promotional expenses to tackle competition, the extent of rise at the gross margin level was not fully reflected at the operating profit level.

While margin expansion should continue ahead, the pace of increase may slow down due to the high base. Thus, a significant uptick in margin hereon would be category or company specific.

Investors in FMCG stocks are treading cautiously, with no big triggers for demand revival in the near-term. In the past one year, shares of HUL and Dabur are down by nearly 4% and 1%, respectively, while that of Marico Ltd are up by 6%.

Amid a muted demand environment, earnings delivery would remain margin-dependent, notes Emkay Global Financial Services.

The valuations of key FMCG stocks are not exactly cheap. Shares of HUL, Dabur, Marico and Britannia trade at 42-50 times their FY25 estimated earnings, according to Bloomberg data.

Emkay notes that valuations would hold on in case demand remains muted and rational competition helps margin-led earnings delivery.