Nykaa’s Q1 may be muted. Fashion biz needs a revamp

by FY28.. REUTERS/Anushree Fadnavis/File Photo (REUTERS)")

- Nykaa’s focus on customer acquisition and brand building may impact margins in Q1FY25

- Fashion business’s subdued performance can be attributed to weak demand and a seasonally slow period

The June quarter update from Nykaa's parent FSN E-Commerce Ventures Ltd paints a picture of resilience in its chief beauty and personal care (BPC) business. However, challenges in the fashion segment take some of the sheen off.

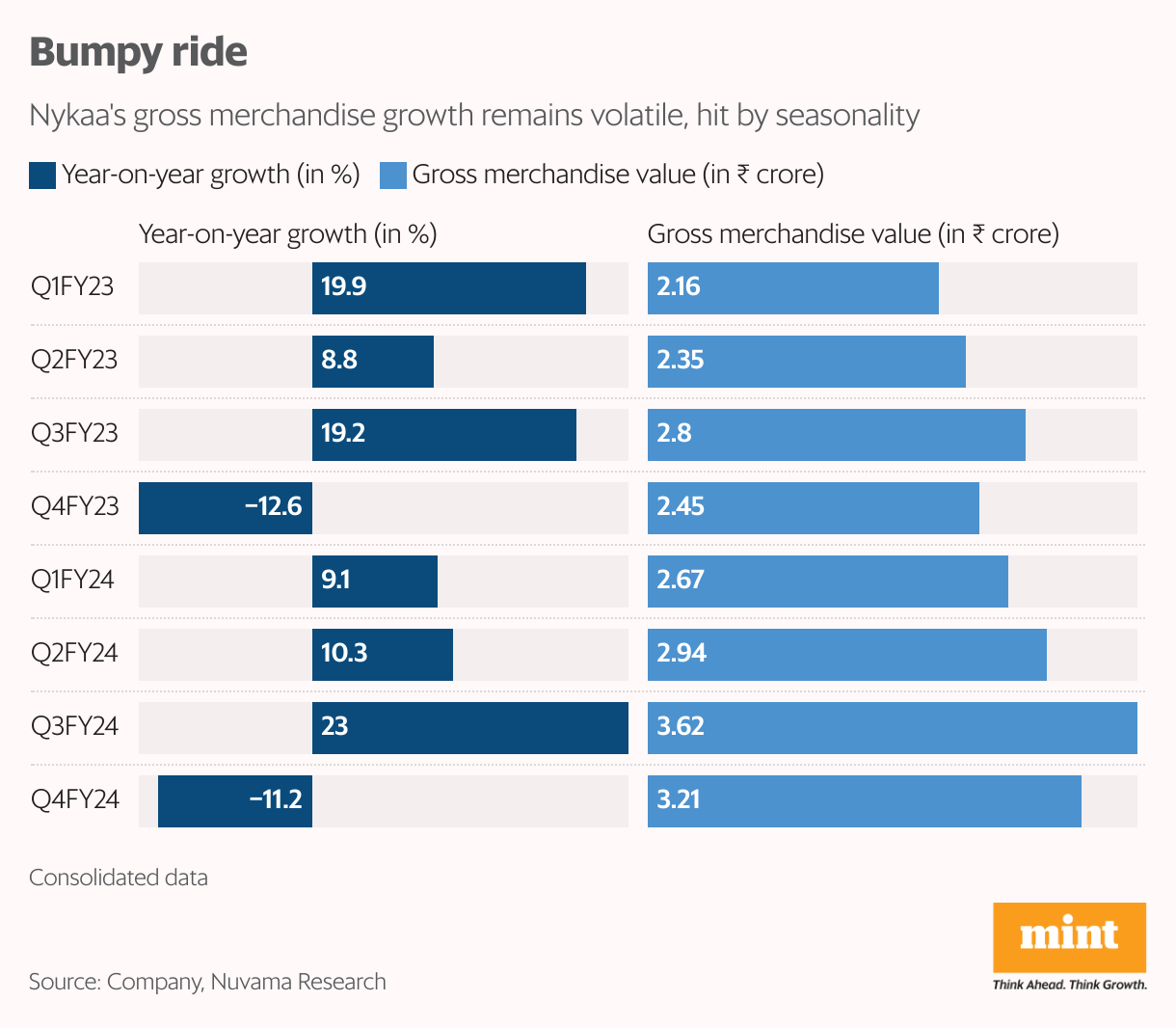

The company expects its consolidated Q1 revenue growth at 22-23% year-on-year, largely meeting its annual growth goal of 20-25%. Here, the BPC segment, contributing nearly 85% toFY24 revenue, is lifting growth substantially. The segment’s year-on-year gross merchandise value (GMV) growth is projected to be in the high twenties. This aligns with Nykaa's ambitious plan to beat the online BPC market growth (19-20% CAGR) with a mid-to-late 20s CAGR over FY24-28.

To achieve this, Nykaa plans to boost spending among existing customers through a wider product range, premiumization, and personalization strategies. Additionally, it will invest in attracting new customers via BPC category development initiatives while simultaneously expanding its physical presence to 400+ stores (187 in FY24) by FY28.

Read more: Dabur’s digital-first brands touch ₹100 crore in sales in FY24

While the BPC segment basks in the spotlight, the fashion segment has been a sore spot. In the June quarter (Q1FY25), year-on-year fashion GMV growth is projected in the mid-teens and revenue growth at 20%. Fashion’s subdued performance can be attributed to weak demand and a seasonally slow period due to fewer weddings and festivities during the last quarter.

Still, there is scope for the segment to end the year on a high note on the back of the upcoming festive season, which can potentially boost overall growth.

Overall, Nykaa’s focus on customer acquisition and brand building may impact margins in Q1FY25 and the immediate future.

For Q1FY25, analysts from Nomura Financial Advisory and Securities (India) expect consolidated revenue growth of 23% year-on-year and Ebitda 5.4%. These are trending much lower than the brokerage’s FY25 expectation of 29% year-on-year and Ebitda margin of 7.5%. “There are downside risks to our estimates if recovery is not stronger in H2FY25," said Nomura’s analysts in a report on 8 July.

Nykaa recently outlined a breakeven plan for the fashion segment, which posted an Ebitda loss of ₹101.6 crore in FY24. The company has guided to break even at the Ebitda level by FY26 and clock a mid-single-digit margin in FY27, helped mainly by growth in brand assortment and advertisement revenue.

While Q1 may not be a blockbuster quarter, Nykaa's BPC segment performance and long-term vision appear promising. As things stand, the company’s shares are about 10% below their 52-week highs seen in January. Two factors are worth watching. One is sustained momentum in the BPC segment despite competition from quick commerce. Two, signs of improvement in profit metrics in the fashion segment.