Markets

Markets

Page Industries’ search for demand continues

Summary

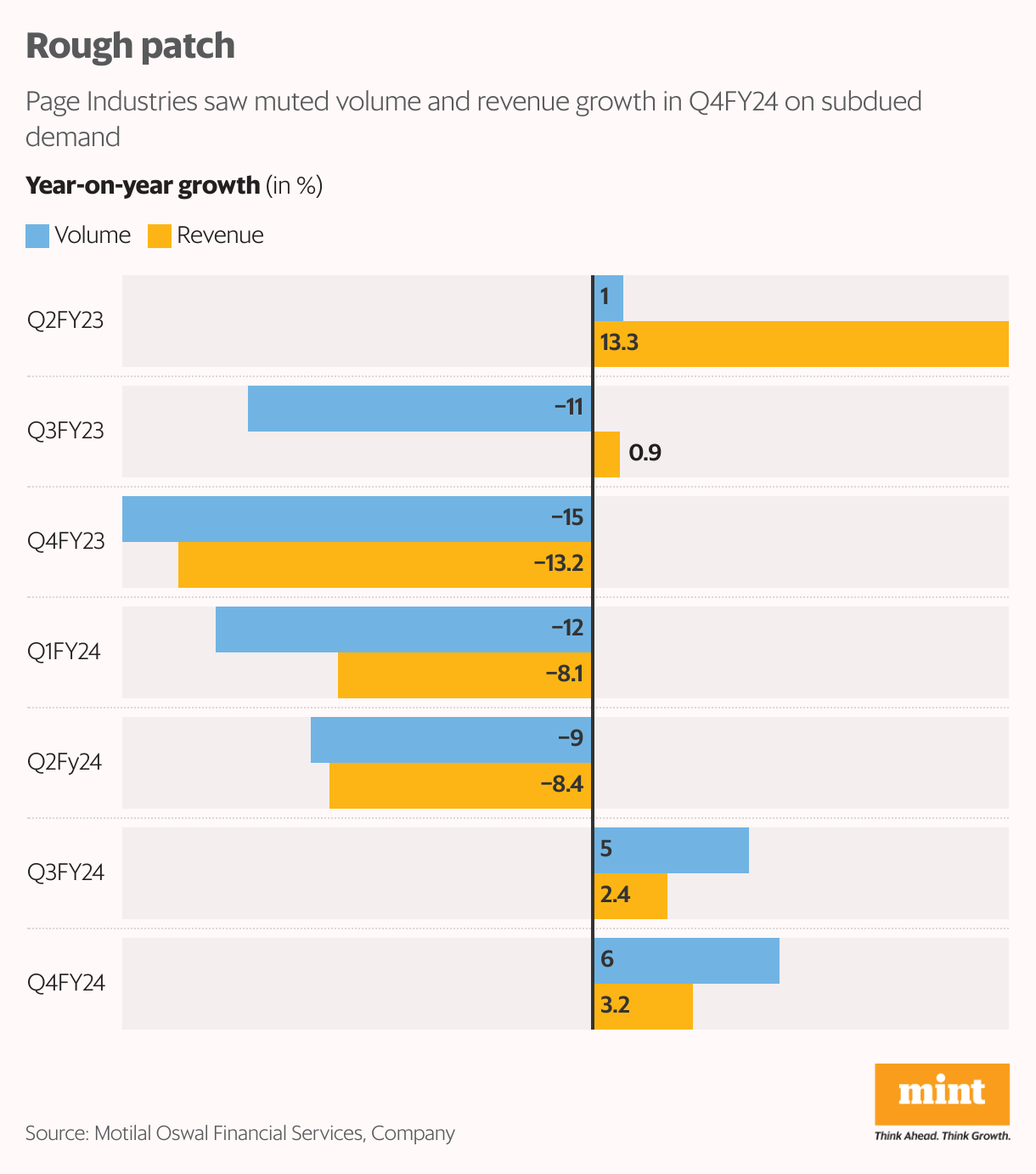

- In Q4FY24, an unfavourable product mix hurt realization growth for Page Industries. Sales volumes rose about 6%, less than anticipated, to 45.3 million pieces.

Is the worst behind Page Industries Ltd? That’s the answer investors are seeking. Unfortunately, the March quarter (Q4FY24) results offer little comfort. The problem is the same: subdued demand.

After Q4, analysts have trimmed earnings estimates for FY25 and FY26. Sure, Q4’s year-on-year revenue growth was the best in the past six quarters but it stood at merely 3.2% to ₹995.4 crore, missing consensus estimates.Also, growth was on a lower base given that revenue had fallen 13% in Q4FY23.

In this year’s Q4, an unfavourable product mix hurt realization growth. Sales volumes rose about 6%, less than anticipated, to 45.3 million pieces. Plus, elevated competition in the organized and unorganized sectors has meant no respite from pricing pressure.

Page has the exclusive licence for the manufacture, marketing and distribution of the Jockey brand. The sole licence for the Speedo brand in India, too, is with the company. In Q4FY24, the innerwear segment did relatively better, but athleisure continued to face demand headwinds. Athleisure combines athletic and leisure styles of clothing, the usage of which had increased during the pandemic.

Read More: Muted demand outlook dampens Page’s turnaround hopes

ICICI Securities believes the relative underperformance in Page’s athleisure wear segment is higher than reported results of other apparel companies until now. The brokerage expects it to be a long gestation turnaround for Page and has trimmed FY25 and FY26 earnings estimates by 10% and 5%.

Problem of excessive inventory

In the earnings call, Page’s management said competitors are giving discounts and higher incentives to liquidate inventory. Page intends to offload the inventory organically given that it is not seasonal. As such, there has not been significant progress on the issue of excessive inventory, particularly in the athleisure segment, which Page has been struggling with lately. At the distributor level, inventory levels came down by three/six days in Q4 and FY24, respectively, aided by the implementation of the auto-replenishment system. This is still higher than the company’s desired levels.

Overall, Page ended FY24 with flattish net profit for the full year. The management expects a revival in demand by H2FY25, aided by inventory normalization and recovery in consumption. Even so, the ongoing channel rationalization is a bother and points to the underlying demand stress. In FY24, the company reduced its multi-brand outlets (MBO) by around 13,200 and the addition of exclusive brand outlets (EBO) was slower at 93. The company is trimming its distribution channels, which could help curtail operating costs, but volume growth may suffer when demand revives, caution analysts.

Also This: Page Industries faces uphill battle amid lingering earnings woes

Meanwhile, Page maintained its Ebitda margin guidance of 19-21%. While it continues to focus on cost-control measures, advertisement expenditure is monitorable. The management believes there is a need to invest in brand building and does not intend to tighten advertisement costs as much. In FY24,ad spending was 3.9% of revenue and is expected at 4.0-4.5% in FY25.

To conclude, triggers for growth are elusive and investors have noted this trend. In the last one year, the stock has declined by almost 14%, lagging the Nifty50 index’s 25% gain. “Page benefited remarkably during covid, particularly in the athleisure segment. Hereon though, growth shall be driven by initiatives to increase channel presence (EBO and online), SKUs (womenswear) and categories (athleisure)," said a report by Nuvama Institutional Equities. Currently, Page is facing challenges on these parameters. Little wonder then that Nuvama said there could be a revenue CAGR of 8% (FY23-26E) for Page versus 17% over FY15–19. CAGR is compound annual growth rate and SKU is stock keeping unit.

Against this backdrop, the lacklustre earnings show has led to a de-rating. Consequently, valuations have moderated from recent peaks but are still not enticing. Page’s shares trade at nearly 56 times the estimated earnings for FY25, according to Bloomberg data. A faster-than-expected recovery in demand should aid investor sentiment.