Markets

Markets

Paytm: Loan distribution business needs to hold the fort

")

Summary

- The success of Paytm's loan distribution business is crucial for offsetting losses from its payment services amid increased competition from new entrants and ongoing regulatory uncertainties

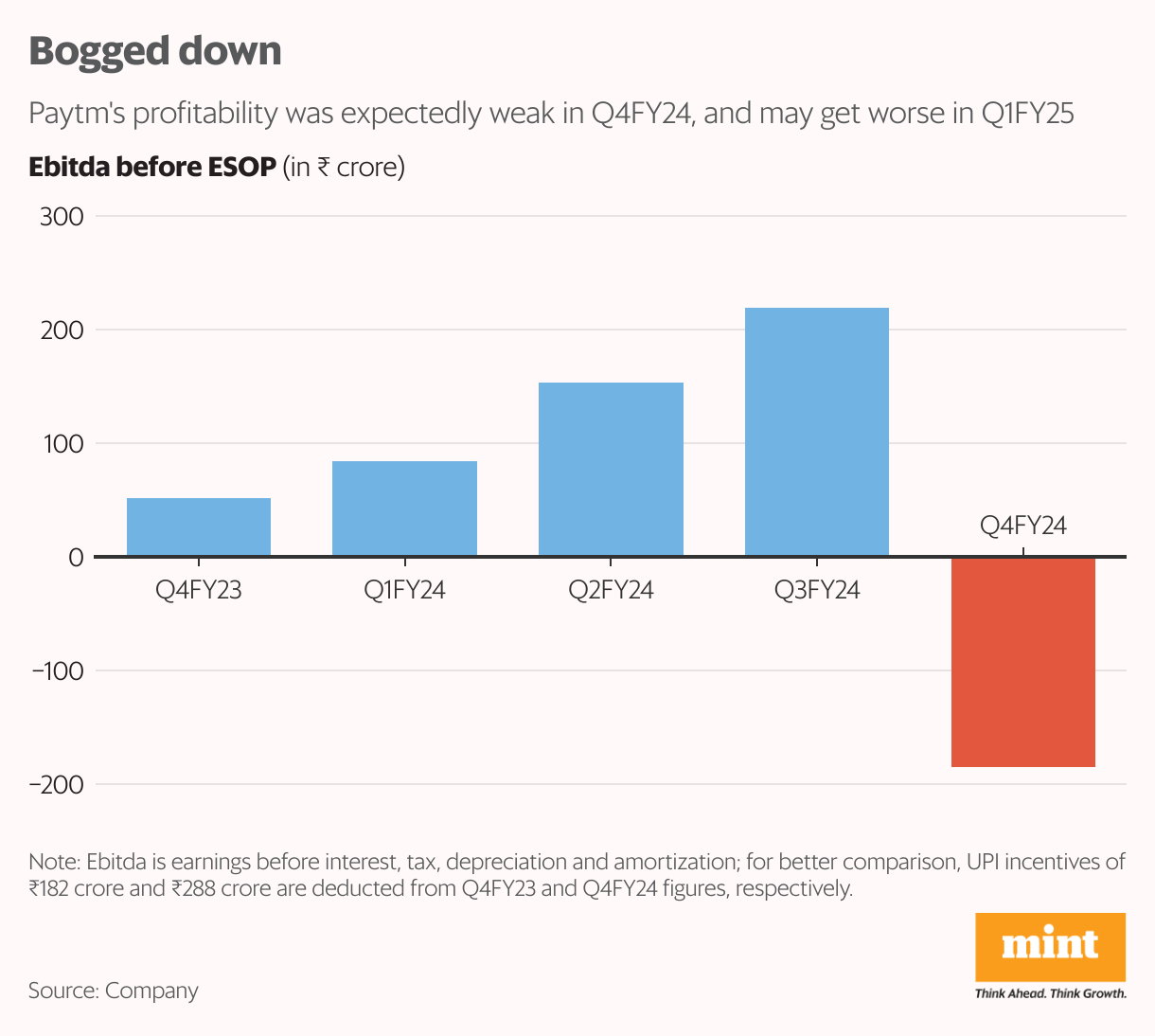

One 97 Communications Ltd, the parent company of Paytm, bore the brunt of the disruption in business following the Reserve Bank of India’s (RBI) restrictions on its payment bank. Expectedly, March quarter (Q4FY24) results were forgettable, but worse is on its way in the ongoing quarter of Q1FY25.

Prima facie, it appears that the management is guiding for the reversal of the positive Ebitda before ESOP (employee stock option plan) in Q4FY24 to negative in Q1FY25.

Paytm’s Ebitda before ESOP stood at ₹100 crore in Q4FY24 but the numbers have to be adjusted for the accounting of unified payments interface (UPI) incentives from the government for user payments made directly from a bank account. Though part of operating income, the need for the adjustment arises because the payment for the whole year is reflected in Q4. Adjusting for this, Paytm saw a loss of ₹186 crore in Q4 at the Ebitda before ESOP level. This loss, according to the management, is expected to widen ₹500-600 crore in Q1FY25.

Read This: Paytm, its payments bank employees seek greener pastures

Revenue guidance for Q1FY25 is at ₹1,500-1,600 crore, down from nearly ₹2,000 crore in Q4FY24, excluding UPI incentives. A significant chunk of the incremental loss in the current quarter may be attributed to the fall in payment service income, with data from the National Payments Council of India showing an almost 8% sequential drop in UPI transaction value on the Paytm app in April.

While the overall payment processing margin for the year is expected to be 5-6 basis points (bps) of gross merchandise value (GMV) including UPI incentives, quarterly payment processing margins, without UPI incentives, are expected to be more than 3 bps.

To be sure, Paytm’s payment services business is not the main focus for investors given the already wafer-thin margins and new competitors testing the waters such as Jio Payments Bank and PB Fintech. It was the cross- selling opportunity to develop the lucrative business of loan distribution or financial services that had caught everyone’s attention.

Paytm earns 4-5% take rates (including collection fees of 1-2% in some cases) on the loans disbursed by its lending partners with no first loss default guarantee (FLDG). FLDG is enforceable when a borrower defaults as the lending partner has the right to force Paytm to share a part of the loss. Following media reports about the potential loss to the company due to FLDG, jittery investors took the stock through a series of lower circuits in May. However, Paytm has denied extending any such guarantee.

Also This: Can Vijay Shekhar Sharma reinvent Paytm once again?

Meanwhile, with lending under buy now, pay later (BNPL) scheme falling by 90% sequentially to ₹720 crore in Q4FY24, Paytm will have to double down on merchant loans and personal loans to make up for the shortfall. There is a lot of scope to do that in view of the very low penetration levels with merchant loans at 5.5% of the total devices and personal loans at 1.1% of monthly transacting users (MTU).

Revenue from marketing services including advertising, credit card distribution and ticketing for travel, movies, events etc. was down 23% sequentially in Q4FY24 to ₹395 crore. The management attributed the fall to lower MTUs.

Investors are sitting on losses with the stock falling as much as 45% so far in 2024. The current market capitalization of ₹23,000 crore, adjusted for the cash in hand excluding customer funds of ₹8,300 crore leaves net enterprise value (EV) of ₹14,700 crore. Sure, the worst may be behind in terms of regulatory uncertainties. But the case for upside rests on scaling up of loan distribution business. Can the business hold fort for Paytm is the question investors need to answer.