Markets

Markets

Persistent Systems investors must look beyond its shiny new AI acquisition

Summary

- Persistent acquired US software company Starfish Associates earlier this week for $20.7 million, boosting sentiment for its already red-hot stock.

- Investors should keep in mind that beyond the AI hype, the acquisition is relatively small and that margins are likely to be under pressure in FY25.

Persistent Systems Ltd stock was in focus on Thursday, gaining more than 3% and hitting a new 52-week high of ₹4,760. This week, the information technology (IT) company’s wholly owned subsidiary announced that it has signed an agreement to acquire US-based Starfish Associates, LLC for $20.7 million.

Starfish is a global software company that provides enterprise communication solutions. The acquisition is expected to augment Persistent’s artificial intelligence (AI) offerings and give it access to various Fortune 500 clients, thus widening the scope for cross-selling.

Considering Starfish’s margin profile, the acquisition is expected to increase Persistent’s earnings per share, ICICI Securities Ltd said. The speed at which Starfish is integrated – and its actual impact on earnings – need to be tracked closely.

Also read: Can Dr Reddy’s buy its way out of a slump?

Persistent is no stranger to inorganic growth, having been on an acquisition spree in recent years. “Persistent Systems has acquired eight companies in the past five years, including Starfish, spending a total of $ 260.5 million and acquiring revenues worth $123.13 million (at the point of acquisition)," said the ICICI report, dated 4 July.

Beyond the AI hype

While the growing traction on AI could be boosting sentiment for the stock, it should be noted that the latest acquisition is small in the overall scheme of things. Against this backdrop, the June quarter (Q1 FY25) earnings performance and demand outlook will be a crucial near-term trigger.

Also read | Q1 results preview: From TCS to HCL Tech, IT sector revenue growth expected to improve sequentially

In Q4 FY24, management had said the macro environment continued to be challenging. Persistent aims to achieve a $2 billion revenue run-rate by FY27. Management reiterated its aspirational earnings before interest and tax (Ebit) margin improvement guidance of 200-300 basis points over the next two to three years. Investors should track these numbers to check if the targets are achieved on time.

In Q1 FY25, Motilal Oswal Financial Services expects Persistent to lead the pack of mid-tier IT companies with 5% sequential constant-currency revenue growth, largely driven by deal ramp-ups in the healthcare vertical. However, it expects the Ebit margin to contract by 50 bps sequentially. Margins are likely to be under pressure due to the initial ramp-up costs for large deals.

Also read: IT companies' revenue revival seen delayed to FY26

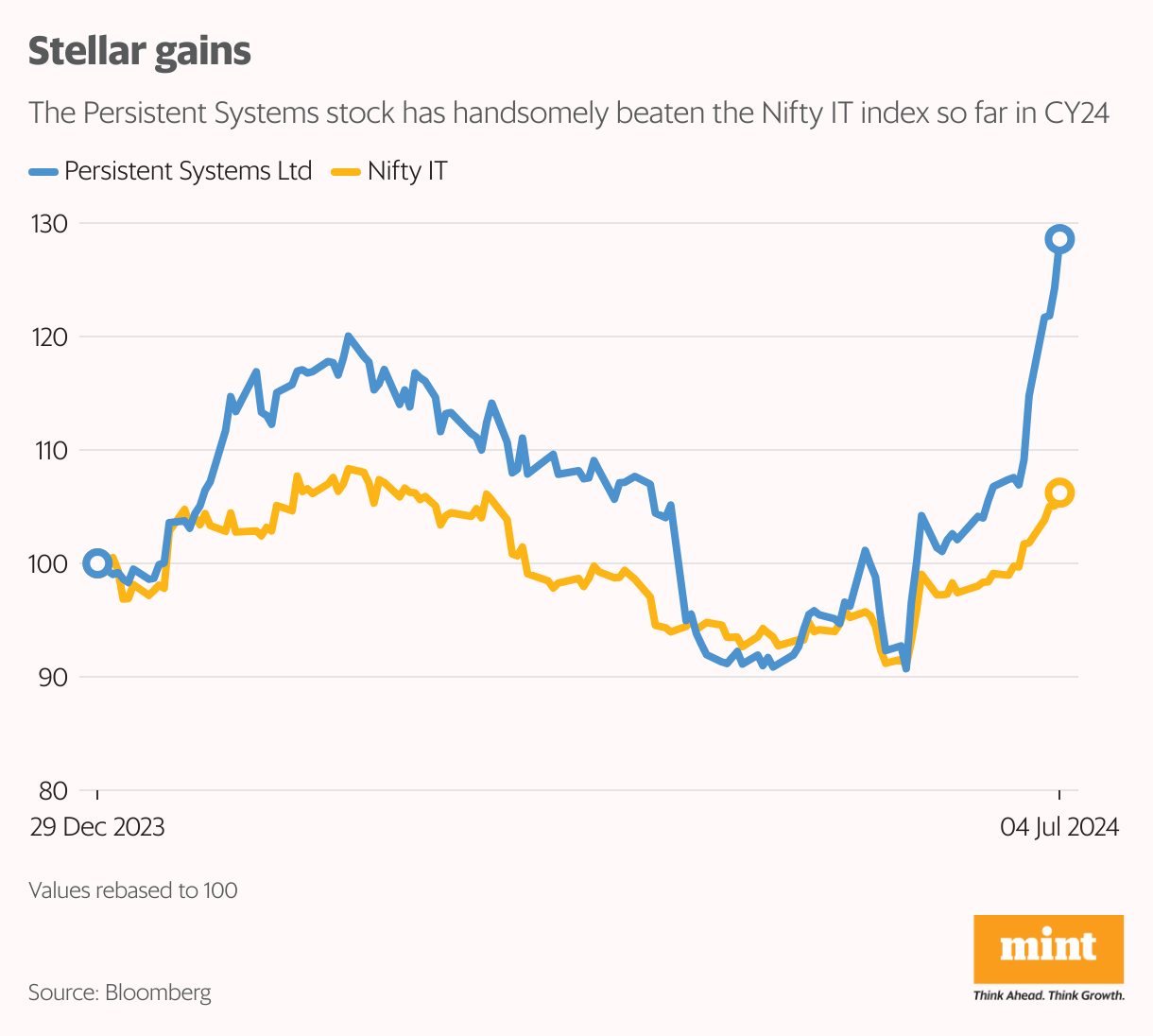

Persistent’s shares have rallied 29% so far in 2024, comfortably beating the Nifty IT index, which has fetched single-digit returns. The stock trades at a price-to-earnings multiple of 43 times estimated FY26 earnings, showed Bloomberg data. The stock has enjoyed a premium over its tier-1 IT peer mainly due to its relatively better revenue growth trajectory. Still, a meaningful revival in demand is crucial for earnings upgrades.