NTPC's project execution delays remain its Achilles heel

The company plans substantial capacity addition, but execution risks remain high, affecting overall market confidence.

NTPC Ltd’s investors remain unimpressed with the 22% jump in its consolidated net profit to ₹7,900 crore for the March quarter because the company missed its capacity addition target of 6 GW in FY25 due to land transfer and supply issues. NTPC added 4 GW of capacity last year, including 2.1 GW from the Ayana Renewable Power acquisition.

NTPC shares have been little changed so far in 2025 and trade at 1.7x their price-to-book value based on FY26 estimates, as per Bloomberg.

“Even as the valuations seem more reasonable, NTPC’s current market price continues to not sufficiently factor the risks from delayed execution and lower-than-expected returns from renewable assets," Kotak Institutional Equities said in a 26 May report.

Also Read | NTPC, France's EDF tie up for pumped storage, green and distribution projects

The company has set tall targets of adding 11.8 GW and 9.9 GW for FY26 and FY27, but execution risk remains high, especially given its recent performance. Revenue grew 5% to ₹1.9 trillion in FY25. Ebitda growth was slightly higher at 6% to ₹54,000 crore, aided by higher captive coal production.

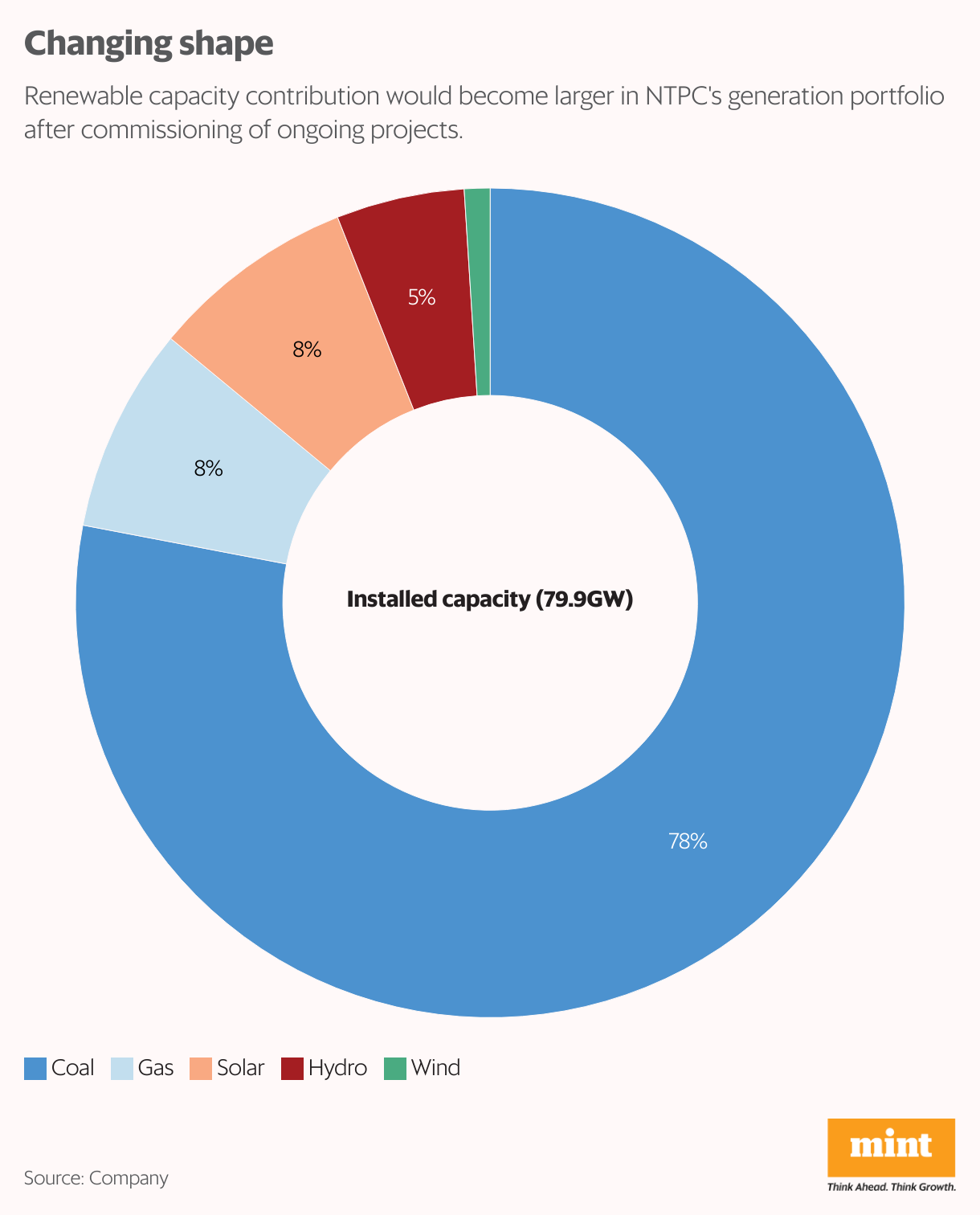

NTPC’s coal mining output grew 35% to 46 million tonnes (mt) in FY25 and is expected to reach 60 mt over the next three years. Coal-based plants form 78% of the company’s installed capacity of 80 GW.

About 34 GW of capacity is under construction, including 14.6 GW of solar and wind energy, which will take their share to almost 20% after commissioning from below 10% now.

NTPC is also taking initiatives to expand its portfolio including nuclear energy.

Consolidated capital expenditure rose to ₹44,600 crore in FY25 from ₹35,400 crore in FY24. NTPC’s FY26 capex target is higher at ₹56,000 crore. Net debt-to-equity ratio was 1.24x at March-end, lower than 1.38x a year ago.

Regulated equity

NTPC’s FY25 return on equity (RoE) was 11.7%, less than the assured RoE of 15.5% on regulated power projects as this is calculated on the equity corresponding to power generating assets, called regulated equity (RE), and not the entire equity.

Consolidated FY25 RE grew 4% to ₹1.09 trillion versus total equity growth of almost 16% to ₹1.91 trillion. The RoE can rise ahead, with under-construction projects coming online and the corresponding rise in RE.

Also Read | NTPC in talks with EDF, Rosatom, Westinghouse to develop small modular reactors in India

Motilal Oswal Financial Services maintained its neutral stance on the stock due to sluggish installed capacity expansion over FY25-27 and its view that the valuation for NTPC Green Energy Ltd—accounting for about 17% of its sum-of-the-parts valuation—will remain under pressure amid execution challenges.