Markets

Markets

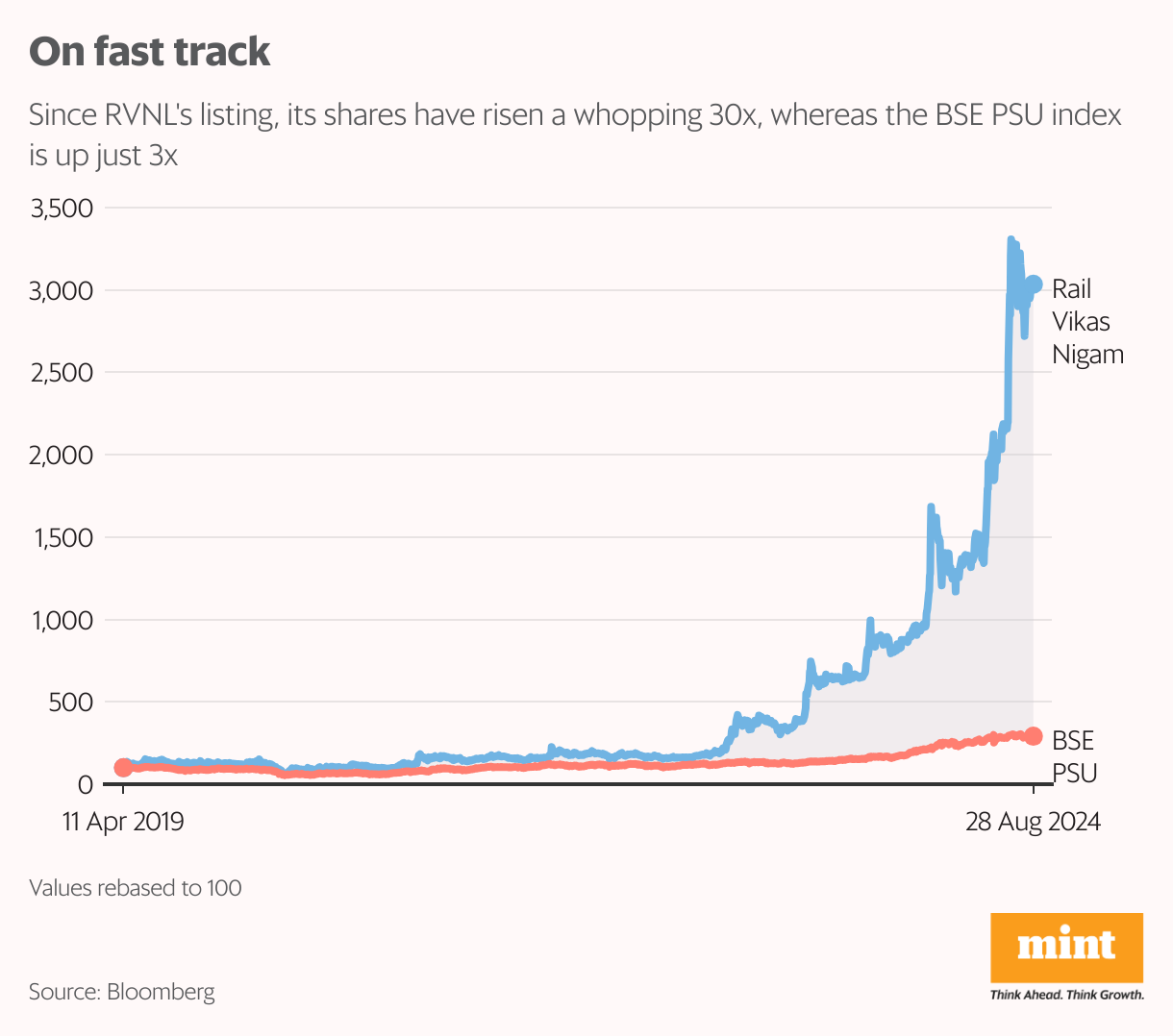

Rail Vikas Nigam: How high can this railway stock go?

Summary

- The public sector undertaking’s stock is up more than three-fold this year and 30-fold since its public market debut in 2019. Is there more upside or should investors stay well away?

Shares of Rail Vikas Nigam Ltd (RVNL) have more than tripled in price so far this year, taking the company’s market capitalisation above the psychologically important ₹1 trillion mark. The stock has delivered staggering 30-fold returns since its listing in 2019.

Is this steep rise justified? To answer that we first need to understand RVNL’s business model. The central public sector undertaking serves as the construction arm of the railways ministry, so it must be evaluated on parameters such as order book and Ebitda margin, like any other engineering, procurement and construction (EPC) company.

Nearly 60% of its ₹85,000 crore order book is from nominated orders or those from the government since it’s a public company dedicated to laying new railway lines, gauge conversion, and so on. The remaining orders are from winning bids for metro projects and non-railway projects such as highways, irrigation and power. The company has strong revenue visibility – the size of the order book is four times of its FY24 revenue.

Also read: JSW Energy banks on increased capacity and government’s renewables push

According to management, the June quarter (Q1) is typically weak for RVNL. Revenue recognition in accounts picks up after a certain threshold is achieved on project execution, so it’s better to focus on annual performance. Q1FY25 numbers were adversely affected by various approval delays in the Indore and Kolkata metro rail projects owing to the general elections.

Revenue fell by 25% year-on-year to ₹4,064 crore and Ebitda by 50% to ₹176 crore. The Ebitda margin contracted to 4.3%, from 6.4% in Q1FY24. Despite the drop in revenue, management has guided for flattish revenue in FY25 at about ₹22,000 crore. The Ebitda margin trajectory is difficult to predict as the margin in non-nominated projects could be different from the fixed margin of around 5% for nominated projects.

Overseas ambition

The company wants to spread its wings overseas but has seen little traction so far. Nevertheless, international orders are a potential catalyst for the stock, with a possible project win in Kyrgyzstan. RVNL has established a 50:50 joint venture with Kyrgyzindustry. If successful, it could add about 15% to RVNL’s existing order book, assuming a 50% share in the ₹25,000-crore order for projects spanning 1,000 km. However, the timeline of securing the actual order needs to be seen.

RVNL is also scouting for railway, solar, and port EPC work in Africa and central Asia, but has had no significant breakthroughs so far.

Also read: Can Apollo Hospitals’ stock sustain its upward momentum without triggers?

It plans to manufacture Vande Bharat trains through a joint venture with Transmashholding of Russia. RVNL will have a 25% stake in the joint venture, which will manufacture 120 Vande Bharat passenger sleeper train sets. The order size could be around ₹35,000 crore for supply and maintenance, meaning RVNL’s share could be nearly ₹9,000 crore. However, as the design has been changed from 16 coaches to 24 coaches, the prototype and manufacturing could be delayed and is unlikely to have a meaningful impact on financials at least until FY26.

Also read: Shriram Finance’s rising non-commercial vehicle share is aiding the stock

Returning to the question of whether the stock’s sharp rally is justified, Antique Stock Broking estimates RVNL’s earnings per share at ₹8.7 for FY26. Even at a hefty price-to-earnings multiple of 40x the stock price works out to ₹348, or nearly 40% less than the current market price of ₹580. Note that a price-to-earnings multiple of 40x is a substantial premium to the 25x-30x multiple assigned to Larsen & Toubro Ltd's core EPC business by brokerages such as Motilal Oswal Financial Services, Prabhudas Lilladher and Sharekhan.