Markets

Markets

For Ramco Cements, quick revival looks challenging

")

Summary

- A quick reversal in Ramco’s fortunes appears unlikely due to the multiple company-specific overhangs amid weak prices in core markets

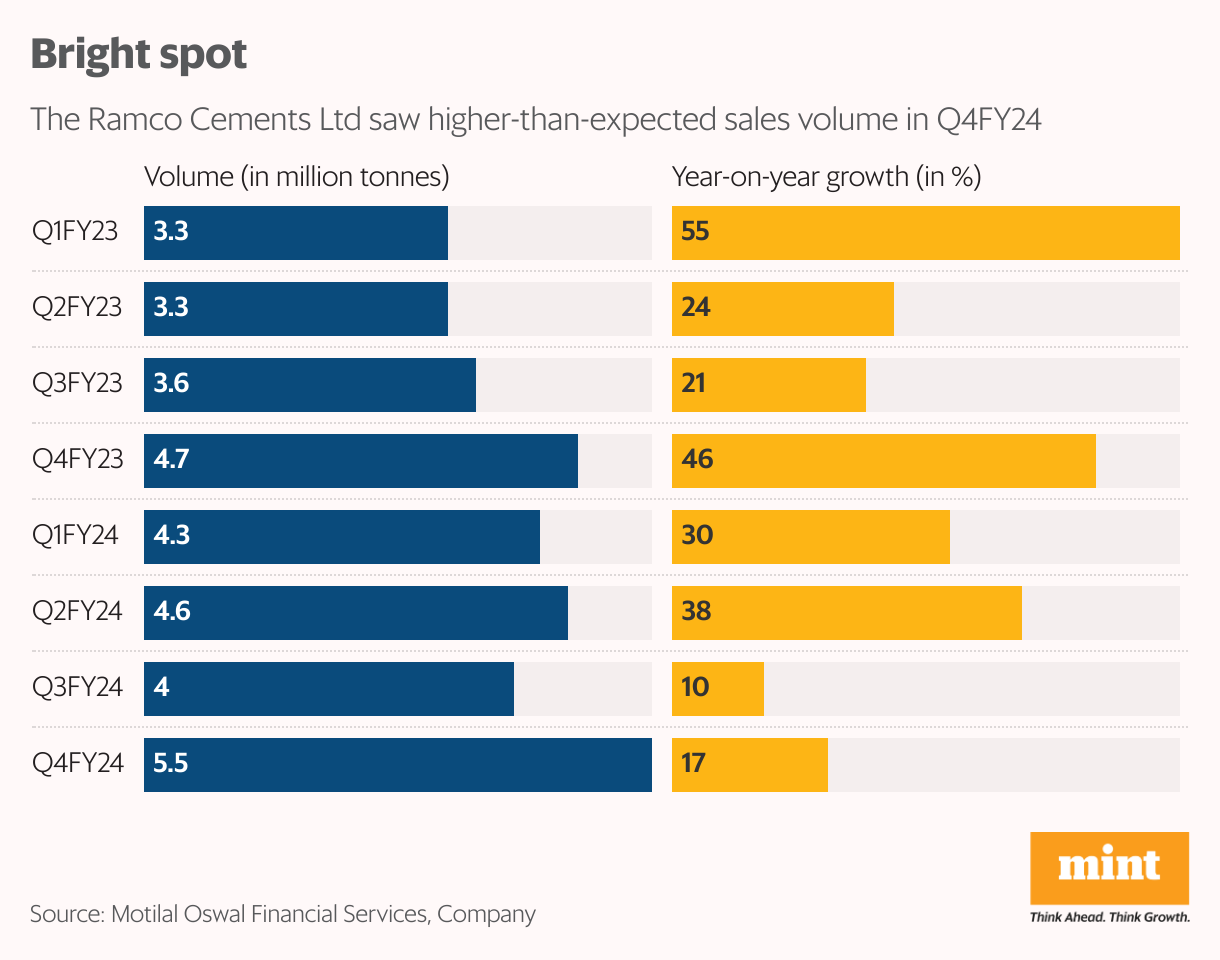

The Ramco Cements Ltd saw a better-than-anticipated volume of 5.5 million tonne, up 17% year-on-year in the March quarter (Q4FY24).

The growth outpaced the industry average of 12%, according to Nomura. This indicates market share gains for the company. But the good news ends here.

Akin to peers, Ramco’s realizations took a hit in Q4 due to muted prices in core markets of south and east India. Blended realization deteriorated 8% sequentially versus 5% sequential drop recorded by the industry, said the Nomura report.

Ramco’s management pointed out that demand is expected to be robust post the general elections, but prices remain under pressure in its key markets, except Odisha. Consequently, earnings estimates for FY25 and FY26 have been revised lower by slew of brokerages.

Centrum Broking has tweaked its assumptions/estimates for FY25 and FY26; and its Ebitda estimates are down by 15%/12%, respectively.

True, the entire cement sector is grappling with muted realizations as prices fail to recover. But Ramco’s investors have to deal with additional issues, apart from the weak profitability outlook, making its earnings growth trajectory bleaker.

Take, for instance, the capital expenditure (capex). Ramco had earlier guided for capex of ₹800- ₹850 crore for FY24, which was later increased to Rs1,650 crore. Eventually, including maintenance capex, the amount stood at ₹1,922 crore.

Also Read: As post-covid demand cements itself, this sector is eyeing a shift in gears

According to Centrum, Ramco has overspent on capex over the past four years resulting in lower return ratios.For FY25, the management has revised its capex guidance from ₹1,700 crore announced in Q3FY24 to ₹1,200 crore. But it is still elevated.

Further, net debt increased to ₹4,822 crore at March-end and the average cost of debt for FY24 rose to 7.70% compared to 6.35% in FY23.

In the current backdrop, where capacity additions continue, meaningful deleveraging looks unlikely in the near term. The company proposed to double the clinker capacity in Kolimigundla, Andhra Pradesh, to 6.30 mtpa and double the cement capacity to 3 mtpa with 15 MW of waste heat recovery system. This expansion is scheduled to be commissioned in FY26. Ramco’s aggregate installed capacity would reach 19 mtpa for clinker and 26 mtpa for cement by FY26.

A quick reversal in Ramco’s fortunes appears unlikely due to the multiple company-specific overhangs amid weak prices in core markets. So far in 2024, the stock has declined by 23%.

On the valuation front, the stock trades at an FY25 EV/Ebitda multiple of around 12 times, according to Bloomberg data. EV stands for enterprise value.

This is a discount to some south-focused peers and pan-India cement makers, but it is not encouraging enough.