A catalyst for Ramco Cements stock is set to play out. But is that enough?

")

Ramco Cement's recent price hikes and ongoing balance sheet deleveraging are key near-term catalysts that could support the stocks’ performance, said Motilal Oswal

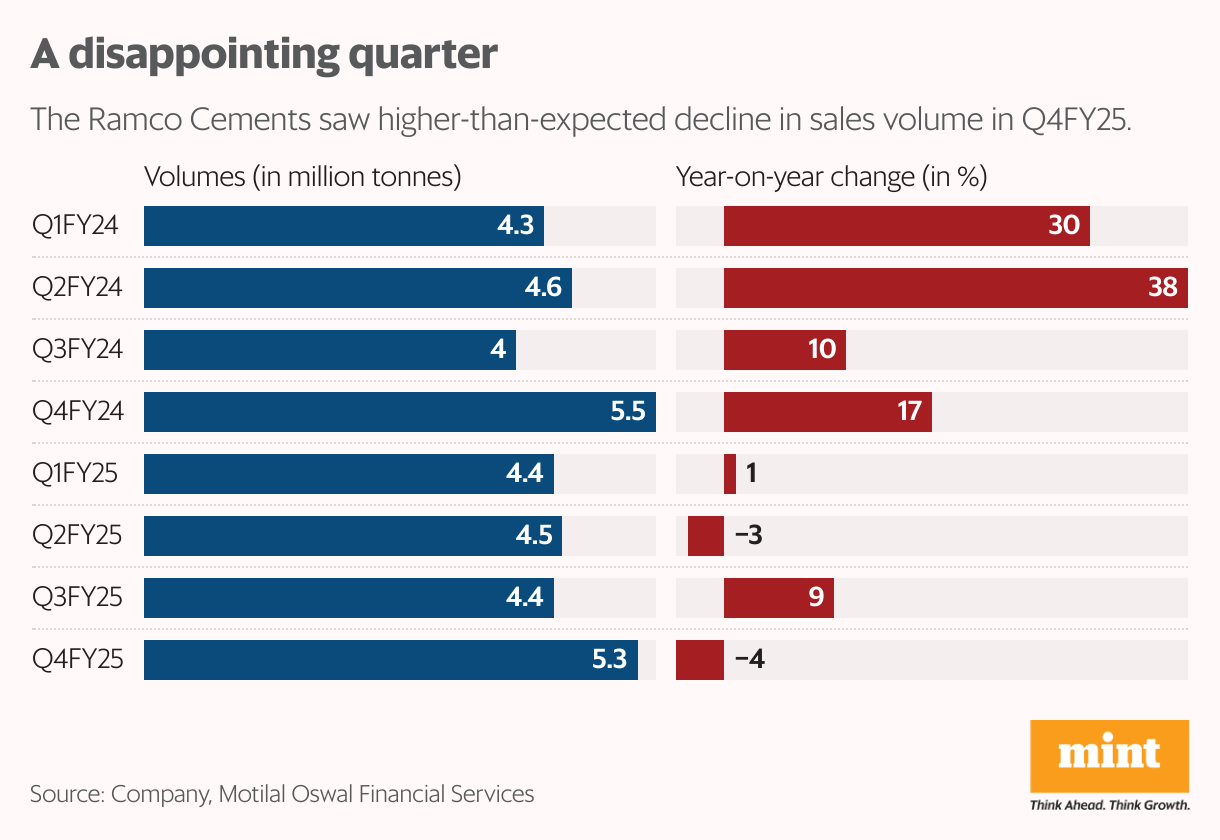

South India-focused The Ramco Cements Ltd had a tough March quarter (Q4FY25). Cement sales volume declined more than expected by around 4% year-on-year to 5.29 million tonnes.

The region has seen an increased pace of consolidation lately, and elevated competition for market share gains has kept cement prices under pressure.

In fact, according to Nomura Global Markets Research, Ramco is the only major cement producer in its coverage to report a decline in year-on-year volumes in Q4FY25; Ramco’s decline was as against 5% year-on-year growth for the industry.

“Blended realization (at ₹4,522 per tonne) came in 4% below our estimate and was flat quarter-on-quarter, as against a 3% improvement quarter-on-quarter for the industry," added the Nomura report.

The Ramco management said that at the start of FY26, price hikes of ₹30-35/bag in the trade segment and ₹60-70 per bag in the non-trade segment were implemented in the south. If these sustain, there is a scope of Ramco’s realisations to mend. Plus, increased thrust on green energy should help the company manage operating costs better.

Here, it is worth noting that the government of Tamil Nadu imposed a new levy – the mineral bearing land tax of Rs160 per tonne of limestone with effect from 4 April 2025. The management expects this to result in additional cost implication of around Rs200 per tonne of cement produced in Tamil Nadu, where Ramco has significant exposure.

Cement manufacturers in Tamil Nadu, through industry association, have represented to the government seeking relief, which is under consideration, it added.

Also Read: UltraTech Cement set for higher volumes, tighter grip on costs

Reducing debt

A company-specific monitorable for Ramco is the pace of debt reduction. It is comforting that Ramco is deleveraging by paring non-core assets. Net debt declined sequentially to ₹4,481 crore as of March 2025, aided by proceeds from the disposal of non-core assets.

The company has monetized ₹460 crore so far out of its targeted ₹1,000 crore. The management said that it is on track to achieve the target of monetizing non-core assets before July as committed earlier. It expects the key net debt-to-Ebitda ratio to ease to 2.50-2.75x in FY26 from 3.51x in FY25.

“We believe that recent price hikes and ongoing balance sheet deleveraging are key near-term catalysts that could support the stocks’ performance," said Motilal Oswal Financial Services Ltd report dated 23 May.

However, sustained profitability, disciplined capital allocation, and meaningful market share gains will be critical structural drivers for a more durable re-rating, it added. In this calendar year so far, the Ramco shares have given mere 3% returns.

While efforts to reduce debt are encouraging, Ramco’s capital expenditure intensity is likely to remain elevated as it adds more capacity. In FY25 Ramco’s capex stood at ₹1,024 crore and the management guided for ₹1,200 crore capex for FY26.

Ramco is expanding its clinker and grinding capacity by 3.2mtpa and 1.5mtpa respectively at Kolimigundla Line 2 in Andhra Pradesh. Mtpa is million tonnes per annum.

It also plans debottlenecking and adding grinding units at existing facilities with minimal capital expenditure. Ramco aims to reach its capacity target of 30 mtpa by March 2026 from 24 mtpa currently.

An Antique Stock Broking report dated 23 March points out that Ramco’s net debt is likely to remain greater than ₹4,000 crore over FY25–27E even after factoring in the sale of non-core assets worth ₹1,000 crore.

“The Ramco Cements currently trades at around 11.9x FY27 estimated EV/Ebitda and $105 EV/ton. The stock may continue to trade below its historical valuation given lower than historical profitability and higher leverage," added the Antique report. EV is enterprise value.

Also Read | Best cement stocks 2025: Demand revival, pricing trends and growth prospects