Markets

Markets

Red-hot Dixon stock has risks too

Summary

- The stock’s expensive valuation multiple could act as a deterrent to fetch meaningfully higher returns from hereon, especially if earnings growth fails to meet the Street's elevated expectations.

Dixon Technologies (India) Ltd investors are sitting on handsome gains. The stock has delivered almost 150% in the last one year, and nearly 30% in the last one month. Dixon is engaged in electronic manufacturing services (EMS), and the prospects for the sector are bright thanks to the government’s initiatives to boost manufacturing through various production-linked incentives (PLI) schemes. But there is a problem—the stock’s expensive valuation multiple, which could act as a deterrent to fetch meaningfully higher returns from hereon, especially if earnings growth fails to meet the Street's elevated expectations.

A recent analysis by Kotak Institutional Equities seeks to illustrate this issue. There are 104 companies trading at one-year forward price-to-earnings (P/E) multiple of greater than 50 times and nine companies with greater than 100 times P/E, according to Kotak. One such company, with a P/E of 100, is Dixon. The company has low debt and there is no significant debt repayment, so P/E is a better valuation metric than EV/Ebitda. The point that needs to be highlighted here is that the company’s P/E of 100 is after factoring in almost 90% growth in Bloomberg consensus EPS estimates for FY25.

Read | Shareholders got record-high dividends in FY24. Will the trend continue?

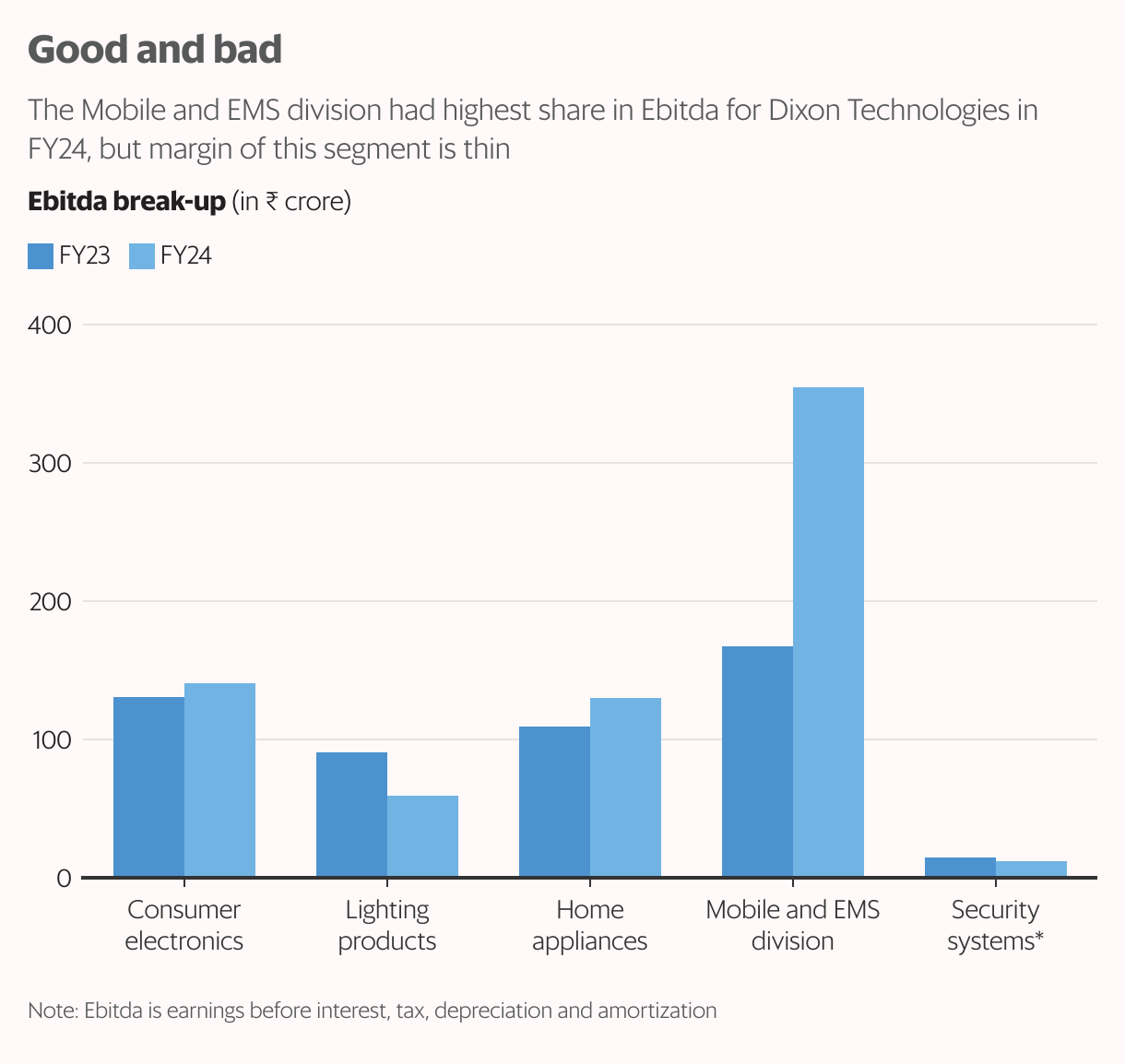

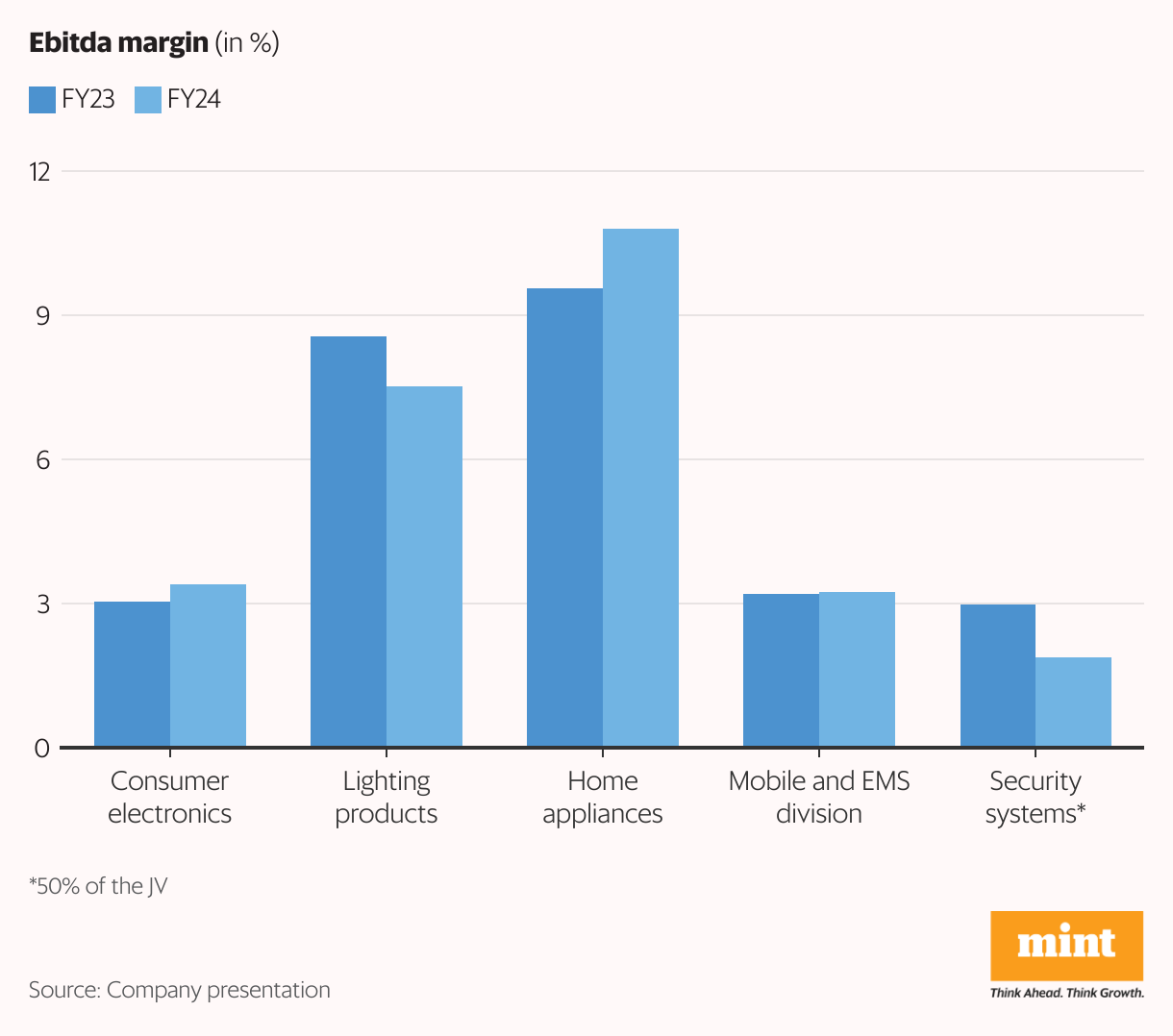

Coming to the financials, the company has grown its sales at a CAGR of 40% during FY20 to FY24, with net profit growth of a little over 30%. CAGR is short for compounded annual growth rate. The lower CAGR in net profit as compared to the sales is because the Ebitda margin in FY20 was 5.07%, which came down to 3.94% in FY24. The company is into contract manufacturing for various brands predominantly in the mobile phones wherein the Ebitda margins are thin. Mobile and EMS divisions accounted for nearly 60% of the total revenue for FY24. The company’s business is more of a volume game rather than the margin expansion with focus on overall RoCE, which is healthy at 34%. RoCE is return on capital employed.

Historical trends suggest that over a five-year horizon, the company can give 30% CAGR in EPS. However, if the P/E after five years declines to 30x from 100x currently, the return on investment in terms of CAGR is a meagre 2%. Even if the investment horizon is pushed to 10 years and 30% CAGR in EPS sustains during the period, the return on investments in terms of CAGR would be at 7%, almost equal to the current government bond yield for the same tenor assuming P/E after 10 years at 15x.

Meanwhile, a look at the shareholding pattern over the past four quarters to March 24 shows that the institutional investors have been aggressively buying the stock. Their shareholding has gone up from 36% to 45% over the last one year. Before retail shareholders get excited looking at the data, they need to dig deeper. Mutual funds and foreign institutional investors have done majority of their incremental buying during March 2023 to September 2023, but at an average price of ₹4,095 per share. The stock hit a new 52-week high of ₹11,679.90 on Friday.

Also | Indian IPO market poised for strong growth as dust settles on election results

Sure, the stock has found favour among investors, but that doesn’t make it immune to risks. Though contract manufacturing does not involve marketing risk, the company’s revenue growth rate is directly linked to the prospects of its clients. “While Dixon has successfully diversified its business across product categories, its business continues to have a high customer concentration–typical for any EMS player–with c59% of total revenue coming from the top 3 customers (majorly Motorola, Samsung, and Xiaomi)," said a BNP Paribas Securities India report.

Since the company is seen as a key potential beneficiary of the PLI scheme, any tweaks would have a direct bearing on its profitability. The company got PLI of ₹71 crore in FY24 against ₹12 crore in FY23, with the bulk of it coming from mobile phone PLI at ₹ 52 crore. Apart from that, a slower-than-anticipated ramp-up of new capacities and weakness in end user demand due to change in technology are other downside risks.