Markets

Markets

Reliance investors wait for oil-to-chemicals business profitability to bottom out

Summary

- If the company can curb further downside in the O2C business, the upside from telecom tariff hikes could have a meaningful impact on overall Ebitda in the coming quarters.

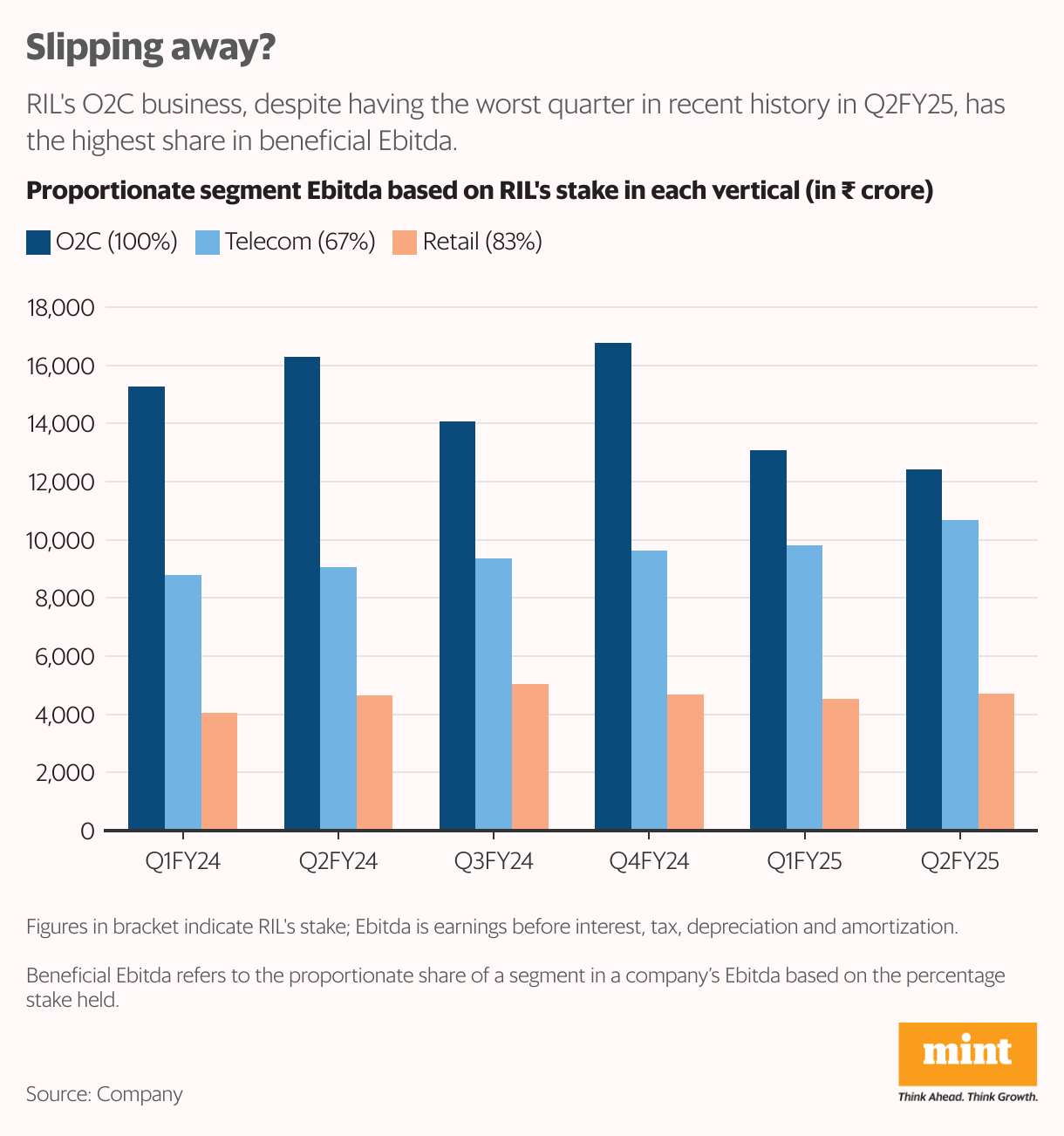

Reliance Industries Ltd’s (RIL's) shares hit an all-time high of ₹3,217.6 on 8 July but have fallen almost 16% since then. One problem has been weakness in the oil-to-chemicals (O2C) business, where Ebitda fell 19% year-on-year in the first half of FY25 and 24% year-on-year in the September quarter.

Despite the drop in profit, if the proportionate Ebitda of each business is considered, O2C remains the highest Ebitda contributor at ₹12,403 crore for Q2FY25 as the company has a 100% stake in the business. Still, the significance of the segment is masked as the consumer businesses, such as retail and telecom, command a higher multiple in RIL’s sum-of-the-parts valuation.

Also read: HCL Tech’s rich valuation clouds re-rating prospects

What’s worth considering is whether the O2C business has bottomed out hitting an at least six-quarter low. While the sequential fall in Ebitda moderated to about 5% in Q2FY25, the base for year-on-year comparison for the second half of FY25 is high, which could cause growth to appear tepid in the next couple of quarters. However, the company believes that the Chinese government’s stimulus offers hope of better profitability in the segment. It remains to be seen if the sharp decline in refining margin – led by almost 50% lower year-on-year transportation fuel product spreads and low margins in downstream petrochemicals – finds a floor.

Jio to the rescue?

If further downside in O2C can be curbed, the upside from telecom tariff hikes could have a meaningful impact on overall Ebitda. The average revenue per user (ARPU) of ₹195 in Q2FY25 versus ₹182 in Q1FY25 does not fully capture the recent tariff hike as longer-term recharges are yet to be renewed at higher prices. It’s likely that ARPU will increase to around ₹210 once the full impact of tariff hike is reflected.

Also read: Is India’s cement sector finally turning a corner?

The company has lost about 2% of its 48.97 crore subscribers from Q1FY25 owing to SIM consolidation (people with two SIM cards giving up one of them) following tariff hikes by telecom companies. If the subscriber base remains at the current level or grows, there is scope for significant upside in telecom Ebitda even in Q3FY25.

As such, cloud storage could be the next big growth driver for the telecom vertical. Jio has already announced an initial offer of up to 100 GB of free storage for Jio users. While monetising cloud services could be some time away, this should help the company retain mobile subscribers.

Retail therapy

The profitability of the retail vertical in terms of Ebitda margin has increased to 8.8% versus 8.4% year-on-year. However, operating revenue is down 3.5% to ₹66,502 crore as the company has increased its focus on rationalising operations and fine-tuning the B2B business to improve margin. RIL alluded to slack demand in the fashion and lifestyle segment, but the increasing popularity of quick commerce cannot be ruled out as a reason for the soft overall performance of retail in urban areas.

Also read: For DMart, quick commerce threat comes to the fore

The 14% growth in footfall despite meagre store additions offers hope that offline retail is still popular, but the higher footfall hasn’t translated into higher sales. JioMart is preparing to take on quick commerce companies by reducing delivery times through its network of stores.

After the Q2FY25 results, RIL’s shares fell 2% on Tuesday. A key upside catalyst is the commissioning of the new energy business, which is at least a couple of quarters away. The stock currently trades at 21 times Bloomberg’s consensus earnings-per-share estimate for FY26, which is in line with Nifty50’s price-to-earnings multiple.

Disclaimer: The author holds a position in RIL.