Shree Cement: Caught between a rock and a hard place

")

- Shree Cement's unclear strategy between increasing market share and improving margins has some investors concerned. Also, demand for cement is expected to remain weak until early 2025, which would affect profitability and growth.

Shree Cement Ltd is a casualty of rising competitive pressures in a weak demand environment.

In the June quarter, its standalone Ebitda of ₹9,164 crore was 22% below consensus estimates. This was largely due to a 6.3% year-on-year drop in its cement realization, a measure of pricing, as the hunger for sales volumes continued to keep the sector’s prices muted.

But the fall in Shree’s realizations was higher than what analysts had estimated and sharper than that of some peers.

In its first-quarter earnings call, Shree’s management acknowledged that the company was facing tough competition in the northern markets from two large cement makers—UltraTech Cement Ltd and Ambuja Cements Ltd. This prompted Shree to sell more cement in the eastern markets, where prices are lower.

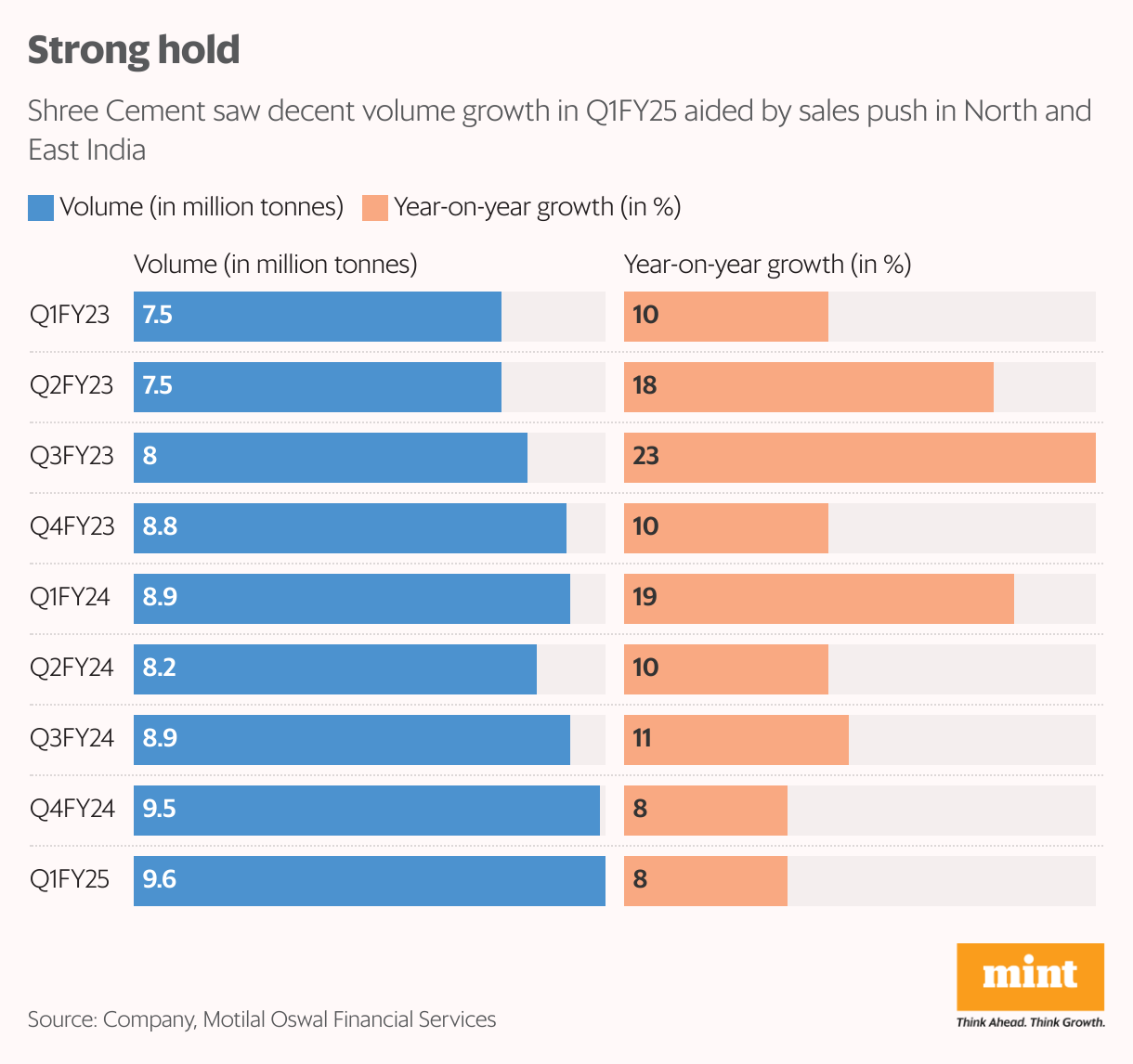

Consequently, the share of the eastern markets in Shree’s overall volume mix in the June quarter stood at 35%, while the northern regions contributed 55%. The balance came from Maharashtra and the southern markets. The shift in the regional mix meant a spike in freight costs and higher lead distance for the Kolkata-headquartered Shree Cement.

The fallout

First-quarter cement volumes at 9.6 million tonnes rose 8% year-on-year, higher than the industry average of 5-6%. However, Shree’s market share gains came at a cost of realizations, leading to steep earnings downgrades by some brokerages.

“Factoring in the lower realization, we cut our Ebitda estimates by 19% for FY25 and by 13% for FY26," Emkay Global Financial Services said in a report dated 7 August.

True, petroleum coke and coal prices have stabilized and inventory lag could lead to some cost savings, acting as a lever for Shree’s profit margin, but the good news ends there.

Muted pricing trends are a negative for the entire sector. But investors worry that this tussle between choosing market share gains and margins may hurt Shree more than others.

“Shree Cement appears confused, with no clear strategy on whether it wants to gain market share or improve pricing gap. In Q1FY25 it tried to grow market share, but now it plans to grow in-line with market," said analysts at Ambit Capital.

Shree targets volume growth to be in-line with the industry growth in 2024-25 versus its earlier guidance of 8-10% growth.

According to the company’s management, cement demand until the end of 2024 is expected to stay weak due to the monsoon, slow government spending, and the upcoming festive season, which usually results in labour shortages, impacting construction activities.

In fact, Shree’s management expects volumes to drop in the second quarter. A full recovery in demand is expected only in January-March next year.

Since price is a function of volume growth, it is better to keep expectations low on the company’s realizations.

Expansions amid profit concerns

Meanwhile, Shree’s expansion plans are on schedule across geographies.

Between April and June, Shree commissioned an integrated cement unit in Guntur, Andhra Pradesh, having a cement production capacity of about 3 million tonnes per annum (mtpa). The company targets reaching 80 mtpa by FY28. It maintained its capital expenditure guidance at ₹4,000 crore each year over FY25-FY27, which will be funded mainly through internally generated funds.

Sure, timely expansion is a positive given the aggressive capacity additions by Shree’s peers. But, for now, there are concerns on profitability.

In reaction to the company’s first-quarter earnings, Shree’s shares have fallen by about 7% in the last three trading sessions, taking its losses so far in 2024 to 14%.

In comparison, UltraTech, ACC Ltd and Ambuja stocks have gained this year.

On the valuations front, Shree’s trading at an FY26 enterprise multiple (enterprise value/Ebitda) of about 15 times, showed Bloomberg data. Industry bellwether UltraTech trades at a multiple of nearly 18 times.

The gap is attributed to Shree gradually losing its cost leadership advantage. Though Shree’s valuation has moderated, in the current backdrop, it is not too comforting.