SRF’s growth momentum is strong, but global uncertainties pose risk

")

SRF reported a 41% rise in Ebitda to ₹1,000 crore. Revenue increased by 21% to ₹4,300 crore, benefiting from enhanced demand in chemicals and a boost in the HFC business.

SRF Ltd’s shares have declined 4% since it announced stellar March quarter results on Monday. This could be because of the slight weakness in the broader equity markets and the 35% rise in the SRF stock in 2025 till the Q4 results.

The industrial and specialty chemicals manufacturing company’s consolidated Q4 Ebitda rose 41% year-on-year to ₹1,000 crore (adjusted for currency fluctuations), aided by improved pricing and better operating leverage. Revenue grew by 21% to ₹4,300 crore. In contrast, 9MFY25 revenue growth was 8% and Ebitda had declined 6%, affected by inventory destocking across the industry.

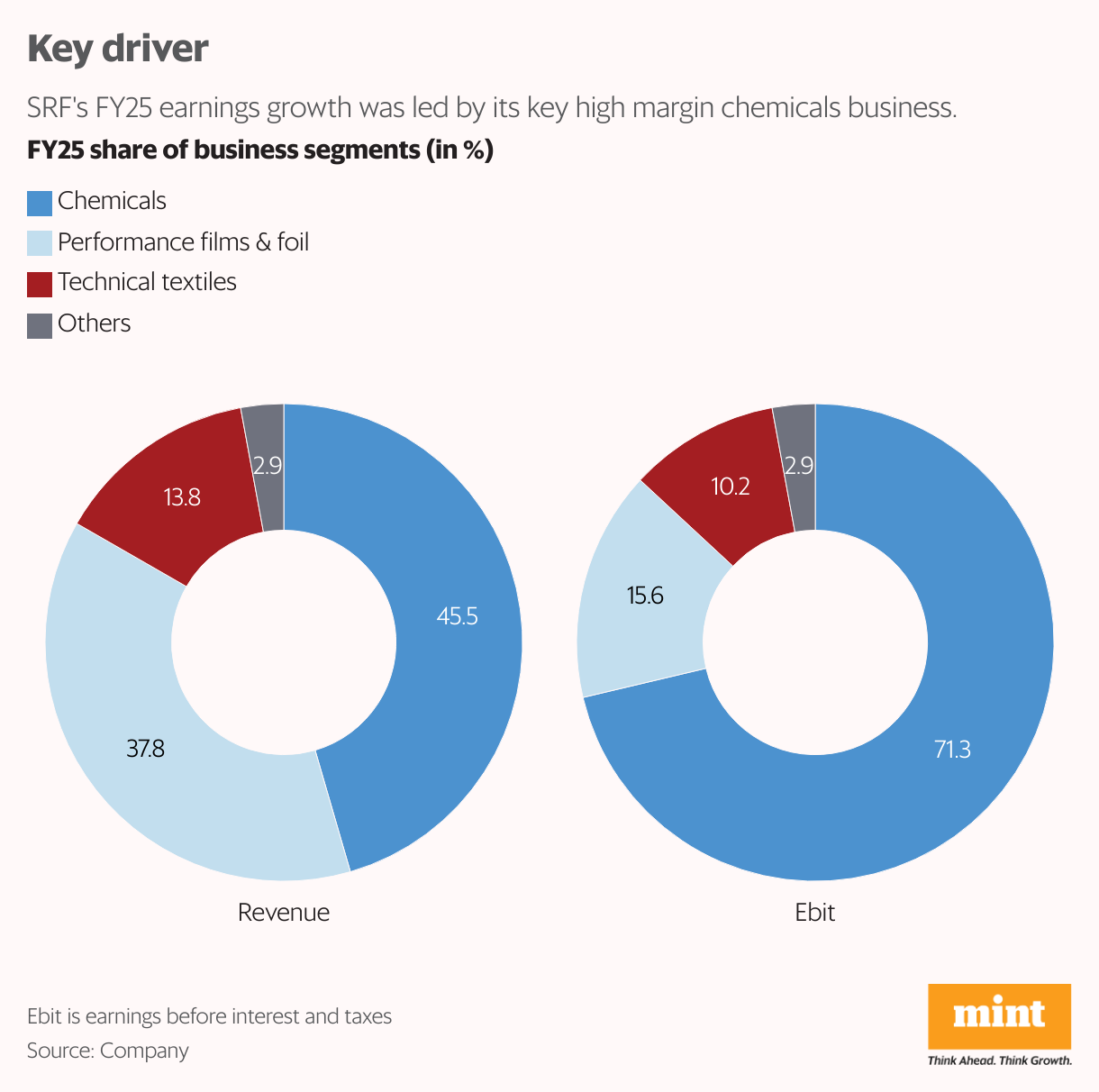

SRF projected revenue growth of 20% in FY26 for its key segment, chemicals, which comprises specialty chemicals and fluorochemicals. Chemicals formed 46% of FY25 revenue and 71% of Ebit.

Also Read | SRF acquires Kanpur Plastipack's CPP business to bolster offerings

Chemicals revenue was up 30% in Q4, while operating profit increased 50%, driven by better demand for certain key agrochemical intermediates, a positive momentum in recently launched products and a pick-up in exports. The HFC (hydrofluorocarbon) business got a boost with lower supplies from China helping to improve prices.

There’s been an uptick in demand in the HFC business, thanks to the government mandate to fit air-conditioned cabins in all new medium and heavy trucks, starting October. SRF commissioned the third plant for anhydrous hydrogen fluoride, an intermediate product, which would help it increase HFC production.

It is trying to maximize its HFC output during the baseline period of 2024-26 because this would determine the quota each producer would get after the initiation of the production phase-down from 2028. SRF is also trying to increase the share of the pharma portfolio within speciality chemicals, which provide better margins with a higher degree of backward integration.

Performance films

The performance films and foil business, accounting for 38% of FY25 revenue, clocked strong growth of 19% during Q4, with higher volumes and realisations, aided by higher sales of value-added grades. While the segment’s Ebit almost tripled in Q4, the margin was only one-fourth that of the chemicals business.

The margin for performance films may stay under pressure as new capacities are commissioned globally over the next 18-36 months.

Also Read | Worst is over; specialty chemicals, new products to drive growth: UPL

SRF’s capex stood at ₹1,200 crore in FY25, primarily going towards debottlenecking and increasing the capacity of the chemicals division by 30%. It has forecast an investment of ₹2,200 crore in FY26.

SRF’s shares trade at 47x FY26 earnings estimates, as per Bloomberg consensus. Valuations are pricey and the volatile global economic environment poses significant risks given that exports form about half of the revenue from the chemicals business.