For steel companies, Q4 was an inflexion point as prices, demand firm up

")

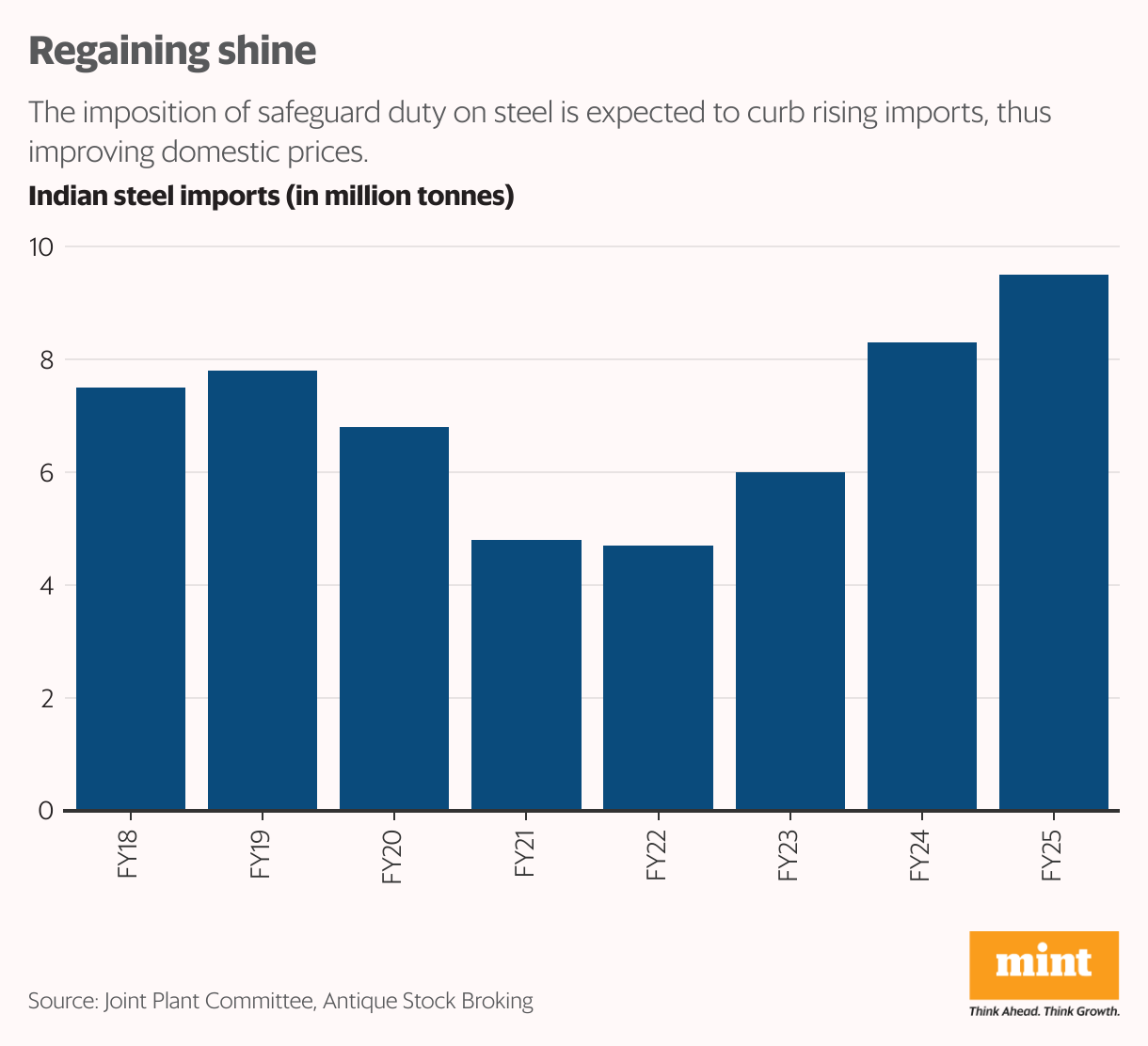

Firm steel prices and a decline in imports are expected to further improve the profitability of four integrated steel players JSW Steel, Tata Steel, Steel Authority of India and Jindal Steel moving ahead

Steel producers saw a turnaround in their performance during the March quarter (Q4FY25), aided by a decline in raw material prices and continued momentum in domestic demand.

While realization remained under pressure, prices started climbing from March, in anticipation of the safeguard duty, announced in April.

The combined Ebitda of the four integrated steel players, JSW Steel Ltd, Tata Steel Ltd, Steel Authority of India Ltd (SAIL) and Jindal Steel & Power Ltd (JSPL) rose only marginally by 1% during the quarter.

This, however, marks a significant improvement after a decline of 14% in Q3FY25. What’s more, firm steel prices and a decline in imports are expected to further improve their profitability moving ahead.

Average realization in Q4FY25 for steel producers declined by 9% year-on-year, lower than the 11% decline in Q3FY25. Flat products producers, which accounted for 95% of imports, suffered the most. Despite the lower realisation, profitability was supported by lower raw material prices with benchmark Australian coking coal prices averaging about $200 per tonne in Q4, almost 40% lower year-on-year, whereas domestic iron ore prices declined by about 7%.

Raw material prices have remained subdued in Q1FY26 till date with coking coal and iron ore prices down about 23% and 11% year-on-year, respectively, in the international market.

Strong volume growth of 10% also helped cushion the impact of lower realization during the quarter. Domestic demand is expected to remain strong, with the World Steel Association projecting India’s steel demand to increase by 8.5% in 2025, on top of 8% growth in 2024, and against a global growth of 1.3%.

However, the subdued pricing environment led to sharp moderation in investments, with the sector’s capex growing by only 2% in FY25, a sharp decline from 22% in FY24, as per a Nuvama Institutional Equities Q4FY25 earnings review report.

Also Read: India likely to seek removal of US steel tariffs in trade talks rather than immediate retaliation

Bright future

The outlook for the industry remains strong with average flat products prices moving up by over 7% sequentially in Q1FY26-to-date to ₹52,000 per tonne, after the imposition of safeguard duty. While this is still lower by about 3% year-on-year, the industry expects prices to firm up further after the monsoon.

Steel imports have also dropped by 21% in April, reflecting the impact of the safeguard duty, as per provisional Joint Plant Committee data. The Nuvama report projects steel industry companies to report strong earnings growth of 20% in FY26 against 5% in FY25, with revenue growth of 8% against 3% in FY25. Among the outperformers are SAIL and JSW Steel with projected earnings per share growth of 38% and 31%, respectively.

Amid the improving outlook, SAIL and Tata Steel shares have gained 18% and 16% so far in 2025, respectively. JSW Steel, weighed down by the Supreme Court’s verdict on Bhushan Steel, is up at a smaller rate of 7%. Steel and raw material price movement will determine the performance of stocks in the coming months.