Hunky-dory equities? Look before you leap

")

- Strong inflows from institutional investors are propelling Indian equities to new highs, despite global risks.

- India's expensive valuations need stronger earnings growth to justify the high premiums, especially after weak Q1FY25 results.

Indian equity benchmarks scaling new highs is no longer surprising. The upshot: the Nifty50 and S&P BSE Sensex have gained 13%-15% in 2024 so far. Notably, India’s share of global market capitalization hit a record 4.6% in August. September kicked off with fresh peaks, with the Nifty50 and Sensex reaching all-time highs of 25,333.65 and 82,725.28, respectively, during Monday’s trading session.

Relentless liquidity inflow remains the key driving force. For the third month in a row,foreign institutional investors were net buyers of Indian stocks in August, parking ₹11,677 crore, as per data from NSDL. Domestic institutional investors did the heavy-lifting by pumping ₹48,277 crore, up from ₹23,485 crore in July.

Read this | SME IPOs: The craziest corner of the bull market is getting crazier

Amid worries of a potential recession in the US and elevated geopolitical uncertainty, India's relatively better macro-economic position can offer comfort to investors. The World Bank has revised India’s FY25 gross domestic product (GDP) growth projection to 7% from 6.6%, citing a pick-up in rural demand. This follows a moderation in India’s Q1FY25 economic growth to 6.7% year-on-year, the slowest in five quarters.

The complacency of equity investors is well captured in the fear gauge Nifty volatility index (VIX) which is down about 30% in the past month and 4% in 2024 so far. The flood of liquidity has overshadowed the pitfalls, such as the rally in mid-cap and small-cap stocks, which may not be underpinned by strong fundamentals.

Kotak Institutional Equities, in a 2 September report, flagged the unusual nature of the Nifty Midcap 150 Index rally over the past year, with top contributors coming from consumption or outsourcing, while traditional market favourite sectors like building and construction materials, apparel, quick service restaurants, and specialty chemicals lagged despite broader market exuberance.

“This is despite the general optimism in the market and irrational exuberance in the mid-cap space," said the Kotak report.

And this | ‘Small caps’ returns have gone into a different planet’

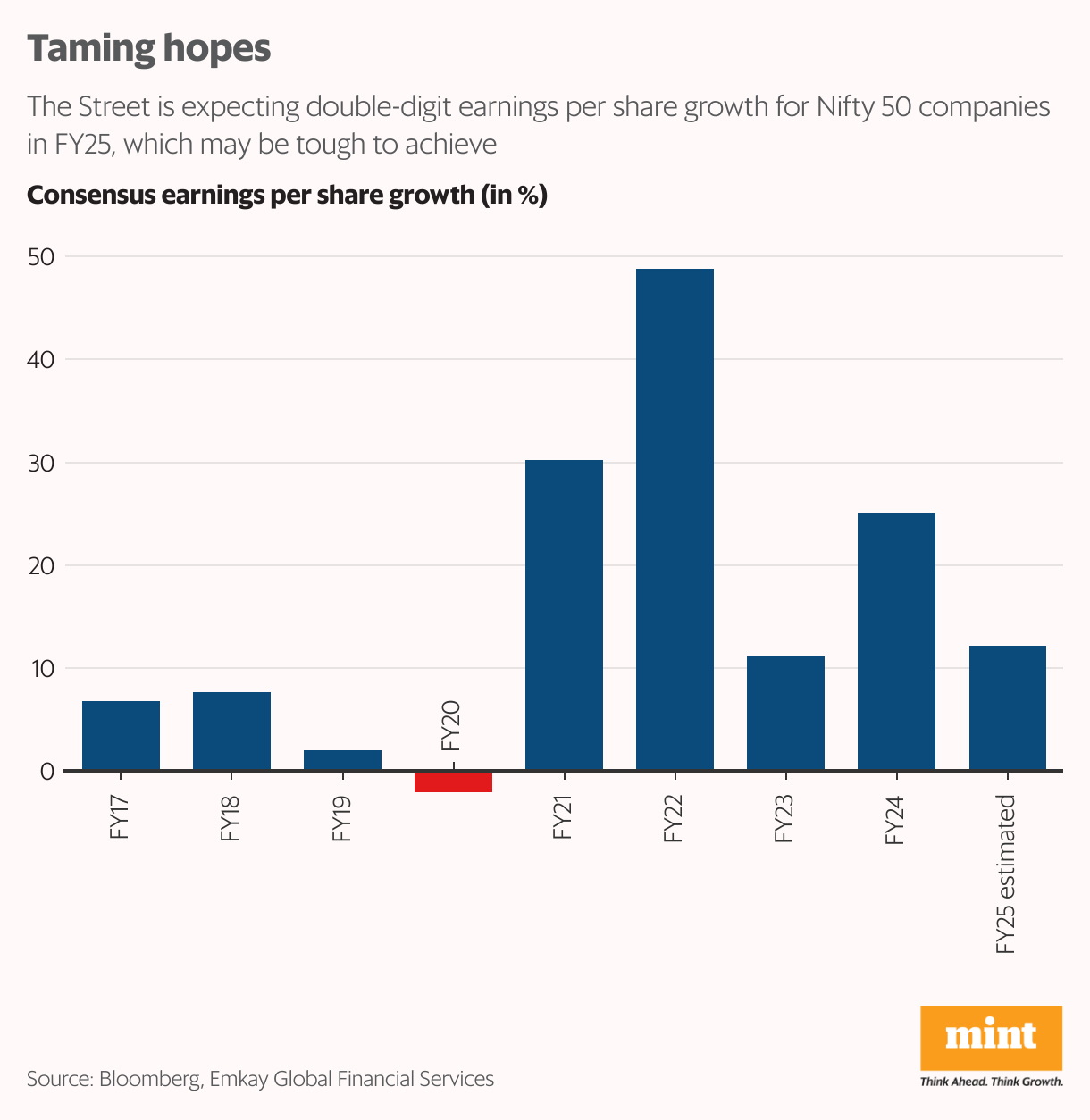

Overall, India’s pricey valuation is a sore point. The MSCI India index is trading at a one-year forward price-to-earnings multiple of around 25 times, a steep premium to MSCI Asia Ex-Japan and MSCI Emerging Markets indices, shows Bloomberg data. To justify these valuations, India Inc.'s earnings growth needs to catch up. Corporate performance in Q1FY25 was lukewarm, prompting downward revisions to consensus EPS estimates for FY25. As a result, the lofty double-digit EPS growth expectations for Nifty50 companies seem optimistic.

For now,all eyes are on the economic data from the US this week, followed by the US Federal Reserve meeting on 17-18 September. The central bank is highly anticipated to oblige with an interest rate cut this time.

“September kicks off with Wall Street near record highs, but also starts the clock on what's historically the worst month of the year for stocks. The S&P 500 hasn't posted a September gain since 2019," said Nathan Peterson, director of derivatives analysis at Schwab Center for Financial Research in a note dated 3 September. However, none of the last four Septembers included a Federal Reserve hinting at rate cuts, he added.

Easing monetary policy would certainly support risk-on sentiment across global equity markets. But for how long the cheer lasts would depend on the quantum of rate cut and Fed’s tone.Further, in a run-up to the US election there may be increased stock market volatility.Moreover, if Donald Trump wins, it may spell trouble for Asian equities.

Also read | Powell ignored the elephant in the Fed’s Jackson Hole lodge

“We think the fundamental impact on Asia ex-Japan (AeJ) stocks from a scenario in which Trump 2.0 policies are implemented is likely to be net-negative," said a Nomura Global Markets Research report. The spectre of higher tariffs amid lower economic growth rates and higher inflation will likely imply lower demand/margins for Asian corporates, especially Asian exporters, added the report dated 3 September.