Tata Motors’ windscreen is hazy amid the fog of tariffs

Amid looming uncertainties, JLR’s Q4FY25 performance isn’t exciting. Revenue was up just 2%, Ebitda declined 5% and volume growth was barely 1%

Tata Motors Ltd’s stock has largely become a derivative of Jaguar Land Rover (JLR), its luxury car unit that contributed nearly 70% to consolidated revenue and 80% to Ebitda in FY25.

Tata Motors’ Q4FY25 results have not triggered a big reaction from the Street as the focus of analysts/investors has clearly shifted to the trade deals featuring UK-India, UK-US and EU-US, and the resultant impact on JLR.

The UK-India deal has limited impact for now on JLR sales in India as most of the vehicles sold in the country are anyway assembled here and the drop in import duty is only applicable to completely built imported vehicles. It will be beneficial in future when JLR decides to export cars from the UK to India as they will be imported at a duty of 10%.

The UK-US trade deal would mean 10% import duties on all UK-made cars sold in the US up to a cap of 100,000 units per year, versus the earlier import duty rate of 2.5%.

JLR sold 129,000 vehicles in North America in FY25, which is 32% of its total sales. Though sales data for the US alone is not available, a bulk of North America sales should be in the US markets. Exports to the US are either from the UK or JLR’s plant in Slovakia. Exports from Slovakia could face a higher import duty rate of 27.5% as the EU-US trade deal is yet to be finalized.

Also read | Jaguar Land Rover tariff hit compounds Tata Motors’ domestic woes

Not very exciting

Amid these looming uncertainties, JLR’s Q4FY25 performance isn’t exciting. Revenue was up just 2% year-on-year to ₹84,957 crore, and Ebitda declined 5% to ₹12,962 crore. Volume growth was barely 1% to 111,400 units—a negative surprise given the company pushed wholesales to dealers in the US to beat the tariff deadline. Note that JLR had paused its shipments to the US for nearly a month in Q1FY26, which should adversely impact the quarter’s results.

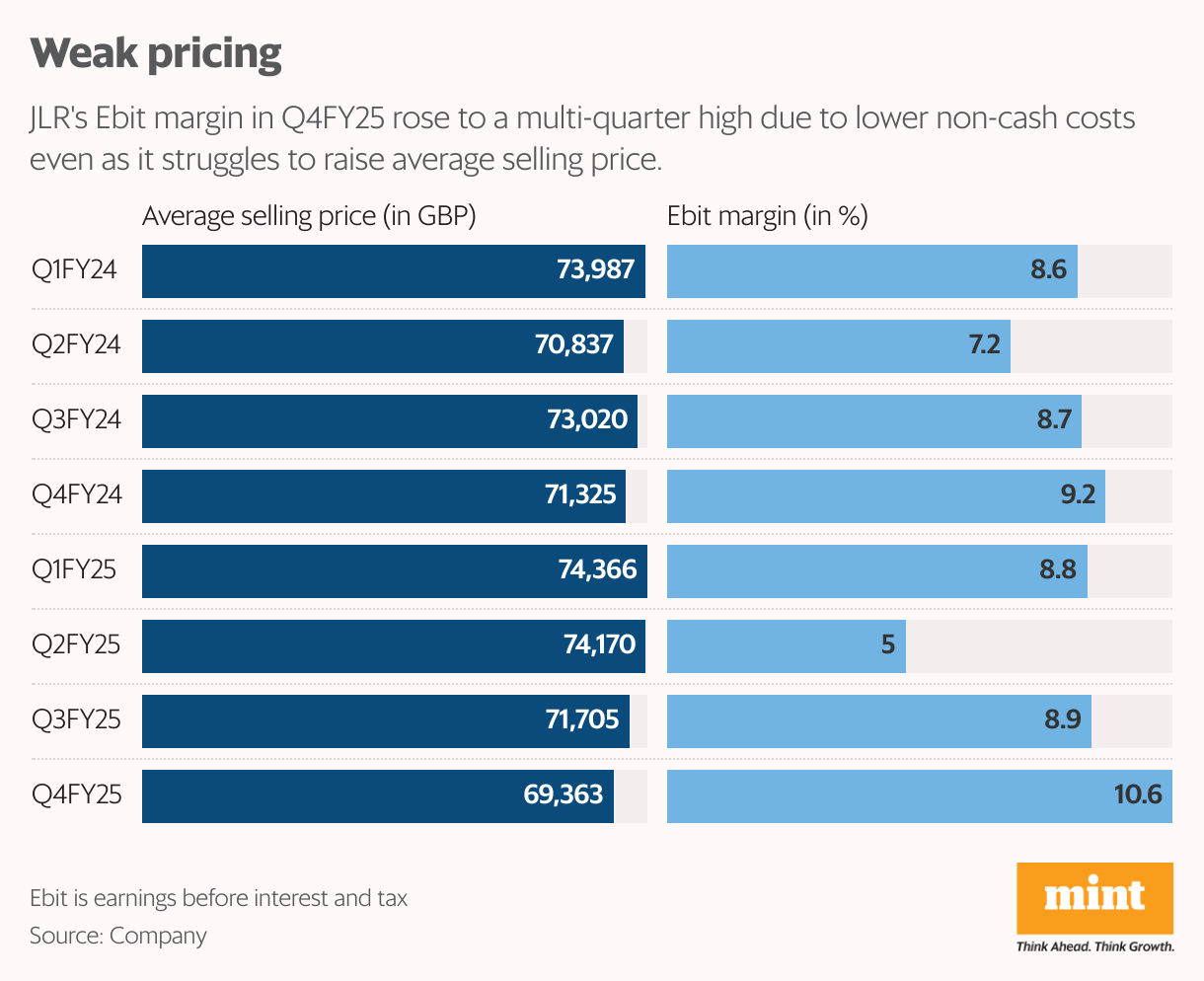

JLR’s Q4FY25 Ebitda margin was down 100bps year-on-year to 15.2%, but Ebit margin expanded almost 140bps to 10.6%. The strong Q4 Ebit margin, aided in meeting the full-year Ebit margin guidance of 8.5%, although that was on expected lines.

While Q4FY25 Ebitda fell 5% year-on-year, a 35% drop in depreciation and amortisation (D&A) charge ensured that Ebit went up, explaining the divergence between Ebitda margin and Ebit margin. Ebit is derived by deducting non-cash expense of D&A from Ebitda.

JLR’s FY26 capex intensity is likely to be at FY25 level. The management indicated that FY26 capex could be £3.8 billion and will be funded from internal accruals.

Also Read: Tata Motors considers new ICE models as EV adoption slows, competition intensifies

Tata Motors continues to struggle in commercial vehicle (CV) and passenger vehicle business in India. CV revenue and Ebitda were flat at ₹21,485 crore and ₹2,622 crore, respectively, in Q4FY25. Further, PV revenue and Ebitda fell by 13% and 6% year-on-year, respectively.

The CV business prospects have improved with freight rates increasing moderately by about 2% QoQ and better utilization rates of vehicles. The management expects FY26 growth rate to be in single-digit. The PV business is suffering from rising competition and the company plans to beat the industry growth rate by launching new models and refreshing and upgrading the existing ones.

To be sure, it is not worth focusing on Tata Motors’ current valuation on a consolidated basis as the company’s effective date for demerger into CV and PV business is coming up this October. That will give an opportunity to investors to buy into the more fancied standalone car business, including JLR, rather than the cyclical CV business.