TCS commentary offers some optimism, but the Street isn’t buying it

- In the current backdrop, margin expansion amid weak revenue visibility and lower valuations is hardly encouraging.

The US tariffs-led uncertainty is temporary—this is the key message from India’s information technology giant Tata Consultancy Services Ltd (TCS). Despite muted earnings in the March quarter (Q4FY25), TCS management feels that the strong deal wins of the past two quarters should help the company report higher growth in FY26 from developed markets than FY25.

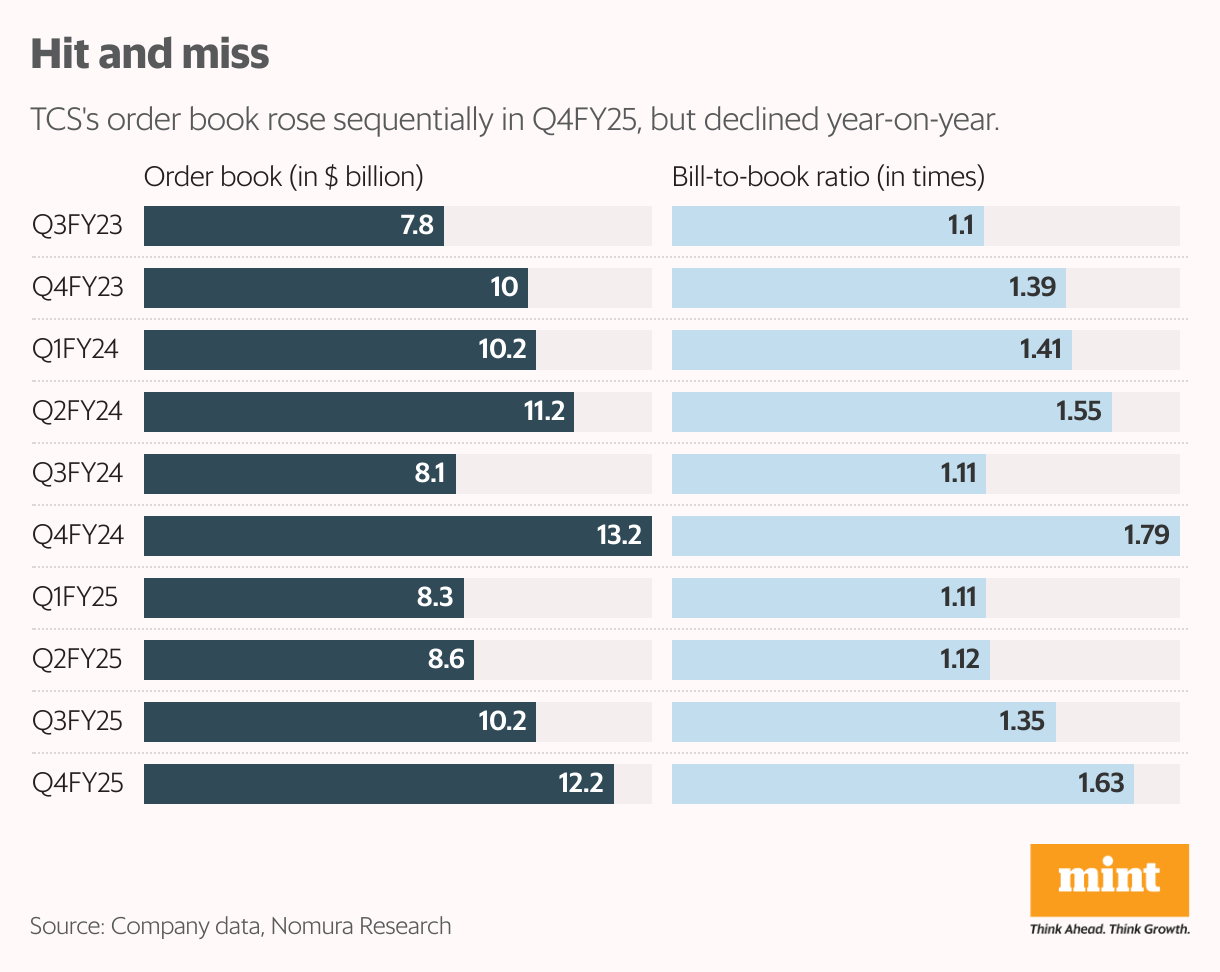

Total contract value (TCV) of deal wins at $12.2 billion in Q4FY25 rose 19.6% sequentially, but it dropped 7.6% year-on-year, implying a book-to-bill of 1.63x. Deal wins were higher in both the BFSI at $4 billion and the consumer segment at $1.7 billion. North American deal wins were the highest ever at $6.8 billion. The TCS management said it is seeing increased traction in artificial intelligence (AI) and has not seen deal cancellations in AI projects. BFSI stands for banking, financial services, and insurance.

However, the spate of earnings downgrades and trimming of target prices by various brokerages reflect that the Street doesn’t share this confidence. “We think it’s hard to say with certainty that slowness in client decision-making due to tariff tantrums will end quickly," said a Nomura Global Markets Research report on 10 April. Nomura has cut its FY26 revenue growth estimate by 100 basis points (bps) to 1.2% versus 4.2% seen in FY25 and FY26-27 earnings per share (EPS) by around 2-3%, factoring in revenue and margin changes. One basis point is one-hundredth of one percentage point.

Also Read: TCS CEO Krithivasan faces biggest challenge amid macroeconomic uncertainty, threat posed by GenAI

The tariff impact

TCS did not see any mega deal wins during the quarter. A worry is that adverse tariff policies and geopolitical tensions might influence client decisions, which TCS has already witnessed towards the end of Q4FY25. Due to muted consumer sentiment, the TCS management has also indicated challenges in some verticals, such as retail and consumer packaged goods, manufacturing, insurance and communications. Client budgets are expected to be flat in CY25, and enterprises are funding additional tech spending by investing in cost-saving initiatives, said the TCS management.

Meanwhile, the expectations from Q4FY25 results were low. TCS saw constant currency (CC) revenue decline 0.8% sequentially, missing the consensus estimate of -0.3%, adversely impacted largely by the ramp-down in the BSNL deal. Earnings before interest and tax (Ebit) margin at 24.2% was down 28bps sequentially, adversely impacted by promotions and higher marketing expenses, but was partially offset by favourable cross-currency movements.

Also Read: TCS, IBM, Applied Materials, KLA in race to modernize India’s state chip unit

The management expects the Ebit margin to be in the range of 26-28% for FY26. According to analysts at Motilal Oswal Financial Services Ltd, BSNL’s ramp-down would most certainly be accompanied by lower third-party expenses, and this should aid margin recovery in FY26. The research house expects margins of 25.3% in FY26, which is around 100bps on-year expansion.

The TCS stock has declined by 18% in the past one year, higher than close competitor Infosys Ltd's 5.6% fall and the the Nifty IT Index’s 6% decline. The TCS stock trades at 22.6 times the estimated FY26 earnings, showed Bloomberg data. Valuations have moderated after the steep fall.

Waning competitive advantage

But in the current backdrop, margin expansion amid weak revenue visibility and lower valuations is hardly encouraging. Kotak Institutional Equities highlights that TCS’s higher resilience is a result of a relatively better portfolio mix, strong and long-term client relationships, and strong execution.

Also Read: TCS, Infosys hop onto Adobe’s new platform to sell AI services to clients

“Yet, the relative resilience versus peers has narrowed compared with the past. Relative competitive advantage has declined. TCS did not lead growth in the past two years, even when demand was driven by cost take-outs," added the Kotak report dated 11 April.