Markets

Markets

TCS’ Q2 margin miss drives earnings downgrades

")

Summary

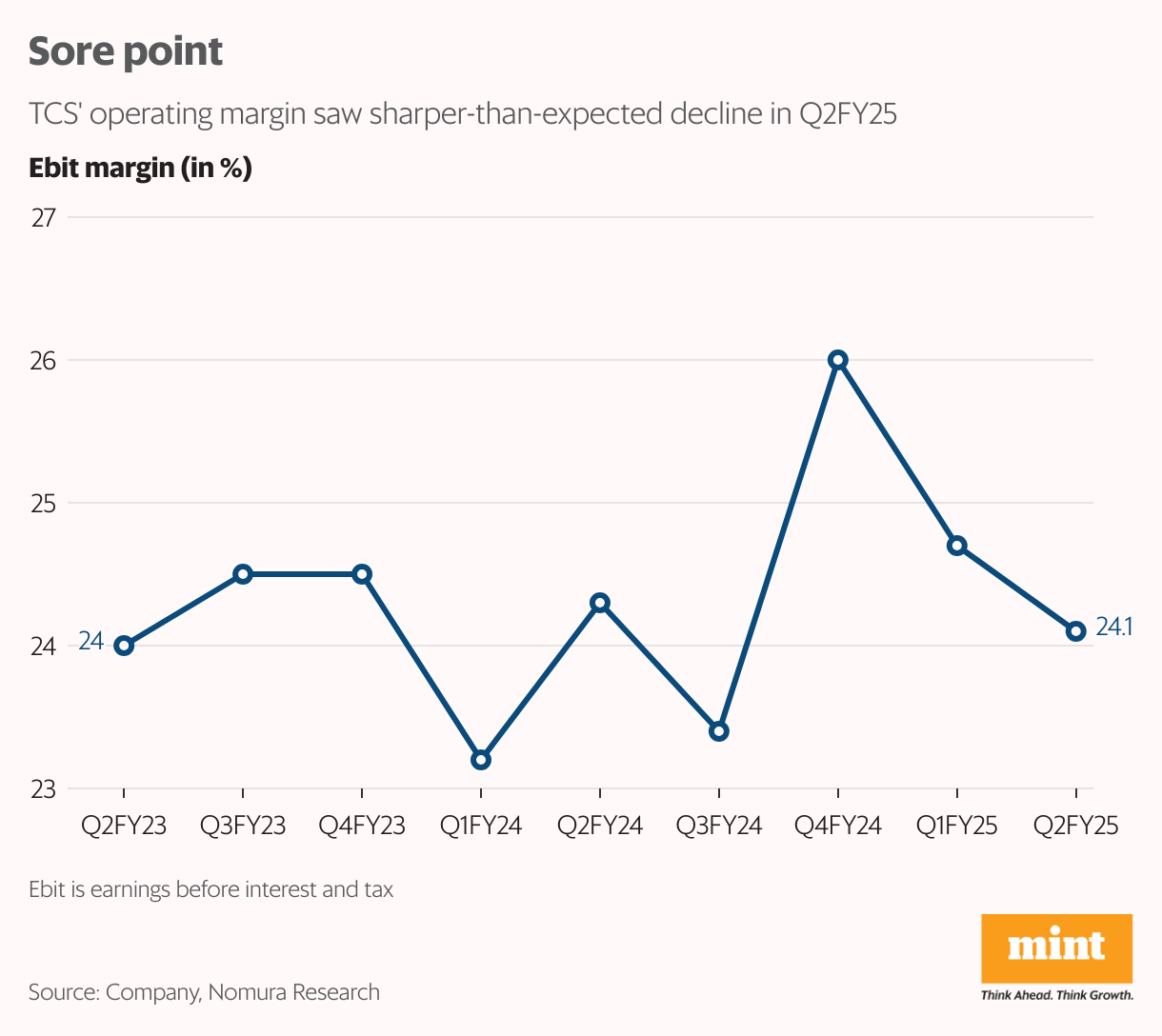

- TCS' earnings before interest and tax, or Ebit, margin at 24.1%, which fell 60 basis points sequentially, and was much lower than Street’s estimate of 24.9%.

MUMBAI : IT bellwether Tata Consultancy Services Ltd (TCS) raised the curtains on the sector's September quarter (Q2FY25) earnings with subdued performance.

Sequential constant currency revenue growth at 1.1% slightly missed the consensus estimate of 1.3%. Weaker growth in the North American market dragged overall growth even as the traction in the low-margin BSNL project improved.

The management said Q2FY25 was impacted by a few client issues in the Life Sciences vertical and in an account in the UK.

Also Read: Hitachi is high on energy, but valuation is low on comfort

While there were signs of recovery in BFSI (banking, financial services, and insurance), client caution on discretionary spending prevailed, and demand for these services remained muted. Clients continue to focus on cost transformation programmes, it said.

This points to a gradual revenue recovery especially amid the ongoing geopolitical tensions that add to global macro uncertainty. “We see that TCS’ growth indicators are softer versus Q1FY25, which saw more broad-based growth," ICICI Securities said in a report on 11 October.

Deals pipeline

The total contract value (TCV) of deal wins in Q2FY25 was soft at $8.6 billion, down around 24% year-on-year, but within the company’s comfort band of $7-9 billion. The management said, its deal pipeline is near record-high levels, but the market condition remains volatile, as seen in Q1FY25, with deals taking longer to close. A delayed conversion of deals into revenue growth thus remains a niggling worry for IT investors. It is worth noting here that the deal TCV in Q2FY24 got a boost from mega deals worth around $2 billion. Whether TCS is able to strike mega deals in H2FY25 will be a crucial monitorable.

Also Read: Is the recent correction a blip for Indian equities?

But a bigger disappointment was earnings before interest and tax (Ebit) margin at 24.1%, which fell 60 basis points sequentially, and was much lower than Street’s estimate of 24.9%. Here, higher third-party expenses and subcontracting costs were partly offset by currency tailwinds.

Earnings downgrades

The margin miss along with a bleak near-term outlook, drove earnings downgrades for TCS. According to a Nomura Global Markets Research report, the BSNL project will be a key revenue driver in H2FY25 but it will be a hindrance in TCS hitting its 26-28% aspirational margin band. “We cut our FY25-26F earning sper share by 1.6%-2.4% driven largely by margin cut," said the Nomura report dated 10 October.

Striking a similar note of caution, analysts at Prabhudas Lilladher also trimmed TCS' FY25/FY26 earnings estimates on a meaningful margin miss in Q2.

Also Read: For GCPL, growth initiatives offer a ray of hope but cost pressures loom

Meanwhile, the stock fell 1% intraday on the National Stock Exchange on Friday, reacting to Q2FY25 results as earnings downgrades marred hopes of quick revenue revival. So far in 2024, the TCS stock has underperformed the Nifty IT index fetching returns of 11%. At FY26 price-to-earnings, the stock trades at a multiple of 27 times, according to ICICI Securities.

Valuations have moderated from recent peaks, but the risk of a further decline in valuations due to subdued earnings growth remains.