Markets

Markets

Ujjivan SFB’s investors appear focused on short-term challenges

")

Summary

- The negative reaction of the Ujjivan stock has widened its valuation gap with Equitas SFB, its closest peer in terms of both the balance sheet size and market capitalization.

Ujjivan Small Finance Bank Ltd (SFB) stock fell 5% on Monday following the double whammy of the downward revision in loan growth guidance and upward revision in credit cost for FY25. Surprisingly, the revision came within just five weeks of the previous guidance.

The bank had earlier guided for 25% loan growth and a credit cost of 1.5%. However, during its recent analysts meeting, these figures were revised to 20% and 1.7%, respectively. Notwithstanding the unchanged net interest margin guidance at 9%, the adverse impact of the guidance turning negative on the two parameters will also mean a reduction in return on equity (RoE) guidance from 22% to 20%.

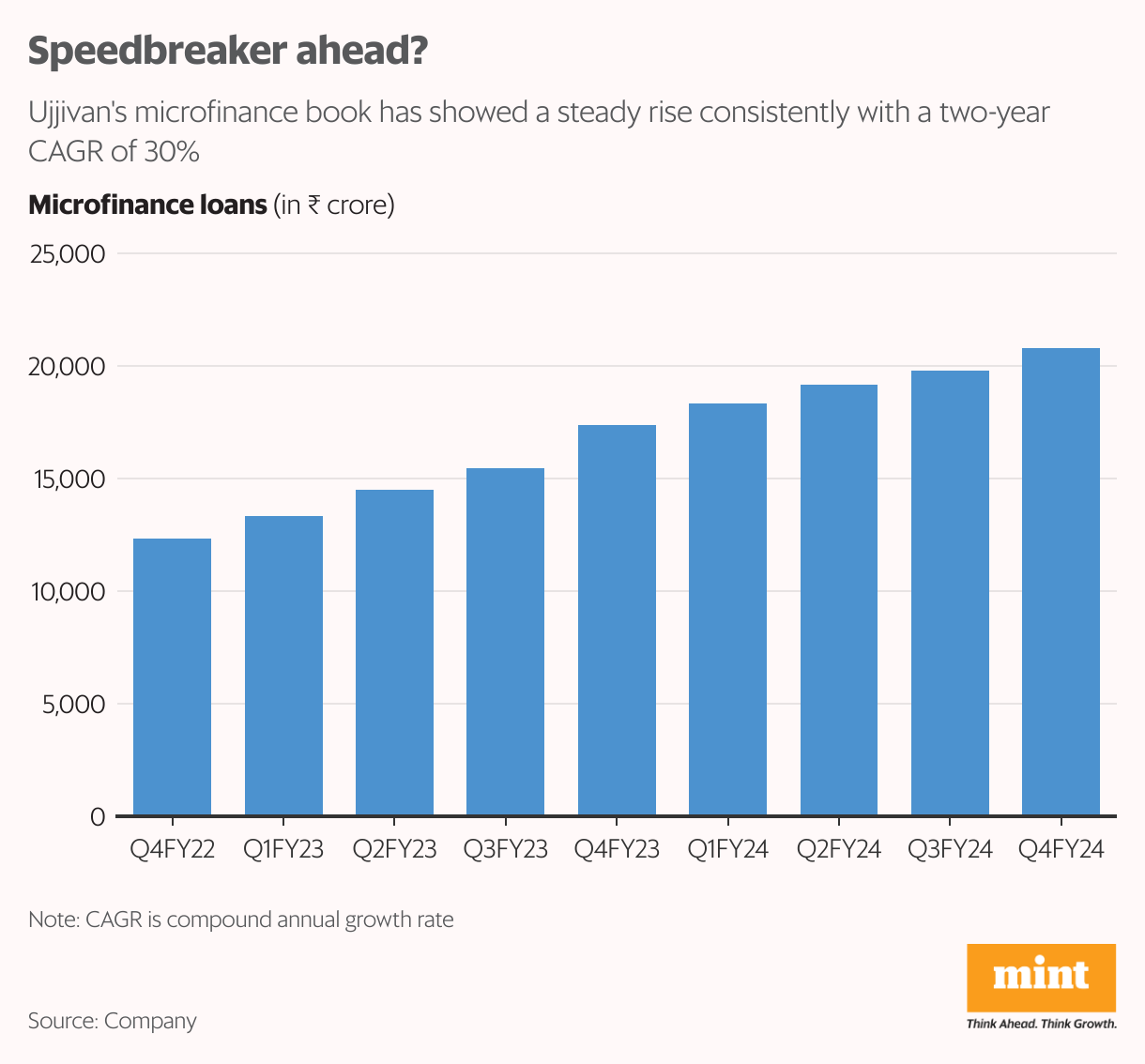

The management attributed it to a detailed review of the portfolio and a report from RBI-licensed credit bureau, CRIF, that indicated stress at the ground level in the microfinance lending segment.

The segment accounts for nearly 75% of Ujjivan SFB’s loan book, largely owing to the requirement of meeting the priority sector lending norms. Additionally, regulatory conditions require SFBs to maintain 50% of their portfolio in small-ticket loans, defined as loans under ₹25 lakh.

Also Read: ‘Small’ isn’t beautiful for small finance banks

As Ujjivan plans to apply for universal banking license, it will get a breather in terms of lower priority sector lending norms and also a relief from the obligation of small ticket loans. But most importantly, the SFB’s minimum capital adequacy requirement (CAR) will come down from 15% to 9% (11.5% if it wants to declare a dividend). This will significantly free up its capital. Though it is believed that the trust of depositors is higher in universal banks vis-à-vis small finance banks, it remains to be seen how far it will help in terms of mobilizing additional deposits.

Ujjivan vs Equitas

The negative reaction of the Ujjivan stock has widened its valuation gap with Equitas SFB, its closest peer in terms of both the balance sheet size and market capitalization. Whether based on historical numbers for FY24 or as per Centrum Broking’s projections for FY25, Ujjivan’s valuation continues to lag Equitas, despite having a higher RoA and RoE. Ujjivan’s RoA is at 3.5% for FY24 and estimated at 2.7% for FY25 as against Equitas' 2% and 2.1%, respectively. Ujjivan’s earnings per share is expected to drop in FY25 compared to Equitas'.

Against this backdrop, Ujjivan’s stock price correction due to the adverse change in guidance could be a case of investors focusing on near-term earnings drop.

Also Read: A tale of two loans: Banks queue up for BPCL, put Vodafone Idea on hold