Markets

Markets

Wipro, Infosys March quarter results paint gloomy outlook for FY25

")

Summary

- The glaring gap between deal wins and actual revenue growth highlights a persistent issue with slow deal conversions

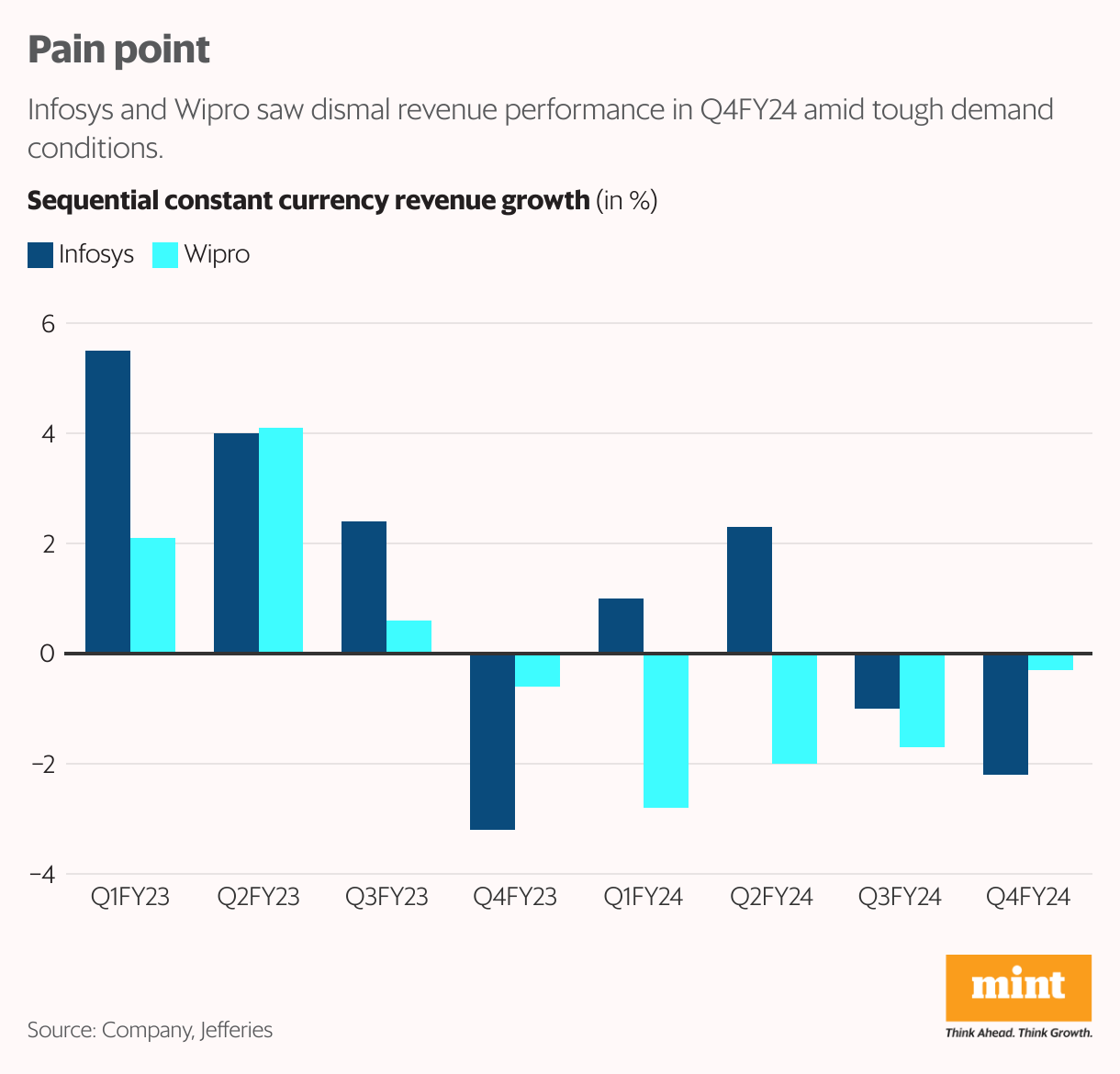

Infosys Ltd and Wipro Ltd have joined their tier-1 peer Tata Consultancy Services Ltd (TCS) in dampening the spirits of IT investors, as their results for the March quarter (Q4FY24) offer little reassurance about the sector’s near-term prospects.

Like TCS, Infosys, too, reported strong deal wins, marking a record high large deal total contract value (TCV) of $17.7 billion for FY24. However, the glaring gap between these deal wins and actual revenue growth highlights a persistent issue with slow deal conversions. This complicates forecasting revenue growth for the industry.

In Q4, Infosys constant currency (CC) revenue fell by 2.2% sequentially, a steeper decline than anticipated. The villain— muted discretionary IT spending by clients. This downturn was exacerbated by a one-time event involving contract re-scoping and renegotiation with a major BFSI (banking, financial services, and insurance) client. Despite ongoing signings of new and long-term deals, primarily cost optimization, smaller deal volumes continue to struggle.

Moreover, Infosys’ FY25 CC revenue growth guidance of 1-3% is conservative, falling below market expectations and not accounting for the In-tech acquisition. The management anticipates a stronger first half for FY25, driven by the ramp-up of previously secured deals. Among verticals, the company expects financial services revenues in FY25 to be better year-on-year. On the other hand, it expects manufacturing growth to slow down.

Infosys’ Q4 Ebit (earnings before interest and tax) margin stood at 20.1%, a sequential decline of 40 basis points (bps). The Ebit margin guidance for FY25 is in the range of 20-22%. Wage increases pose challenges, while reductions in subcontracting costs and improvements in utilization offer potential benefits.

“This is the lowest annual guidance by the company since Q2FY21," said ICICI Securities Ltd. In effect, earnings estimates have been lowered. The brokerage house has cut its FY25/26 earnings per share estimates by 1-8% after factoring in Q4 print, the impact of In-tech acquisition, and a bleak outlook.

Also Read: US banks remain a worry for Indian IT firms

Nonetheless, Infosys’ investors may be relatively better placed than Wipro where the pain is likely to be accelerated by its internal issues, making the road to meaningful revenue recovery arduous.

In Q4FY24, Wipro's IT Services CC revenue fell 0.3% sequentially. A positive surprise was the 130-bps sequential expansion in Ebit margin to 16%, although the Q1FY25 guidance disappointed. Wipro's Q1FY25 CC sequential revenue guidance of -1.5% to +0.5% indicates a weak outlook and fell short of already muted expectations. That, along with declining headcount, signals limited demand visibility.

According to the Wipro management, the demand environment remains uncertain, and geographies like the UK and Germany continue to be under pressure. Despite some green shoots being visible in its consulting business, which has been a pain point lately, expectations remain tempered. Amid global demand uncertainty, delayed turnaround benefits could keep the revenue growth gap between Wipro and other tier-1 peers wide.

Against this backdrop, growth strategies laid out by Wipro's new CEO are crucial. Acceleration of large deal flow, simplifying the organization and operating model, are among the five strategic areas that the new CEO will focus on; execution in a tough demand scenario will be key. In any case, the results of these measures will reflect in the long run.

Analysts at Nuvama Research caution that the CEO transition may further delay Wipro’s recovery. “We continue to anticipate Wipro to underperform peers while its inexpensive valuation and high dividend yield limit the downside potential," said the Nuvama report.

According to Bloomberg data, Wipro's stock is currently trading at a price-to-earnings multiple of 19 times for FY25, compared to 22 times and 27 times for Infosys and TCS, respectively.