Zomato-Paytm ticketing deal appetizing for both

")

- Zomato’s acquisition of Paytm’s entertainment ticketing business is in line with its plans to strengthen its presence in the going-out segment.

MUMBAI : Zomato Ltd and One 97 Communications Ltd, the parent company of Paytm, have found common ground. The online food delivery company wanted to acquire a business focused on lifestyle, and Paytm wanted to exit businesses not related to digital payments and financial services.

After the Reserve Bank of India's (RBI’s) ban on Paytm Payments Bank, it is critical for the company to get its act together by sharpening focus on core businesses like loan distribution and exiting from smaller businesses like entertainment ticketing.

Zomato’s acquisition of Paytm’s entertainment ticketing business is in line with its plans to strengthen its presence in the going-out segment (which includes dining out and event ticketing). Even so, the muted reaction of Zomato’s shares—1% down on Thursday—after the deal announcement appears justified if one looks at the current numbers and future estimates for the business as indicated by the management.

Also Read: Zomato’s Paytm deal and its big bet on entertainment

Paytm’s ticketing business has been valued at ₹2,048 crore—7X FY24 revenue of ₹297 crore. The Ebitda margin is at about 10% of the revenue. Ebitda is earnings before interest, taxes, depreciation and amortization.

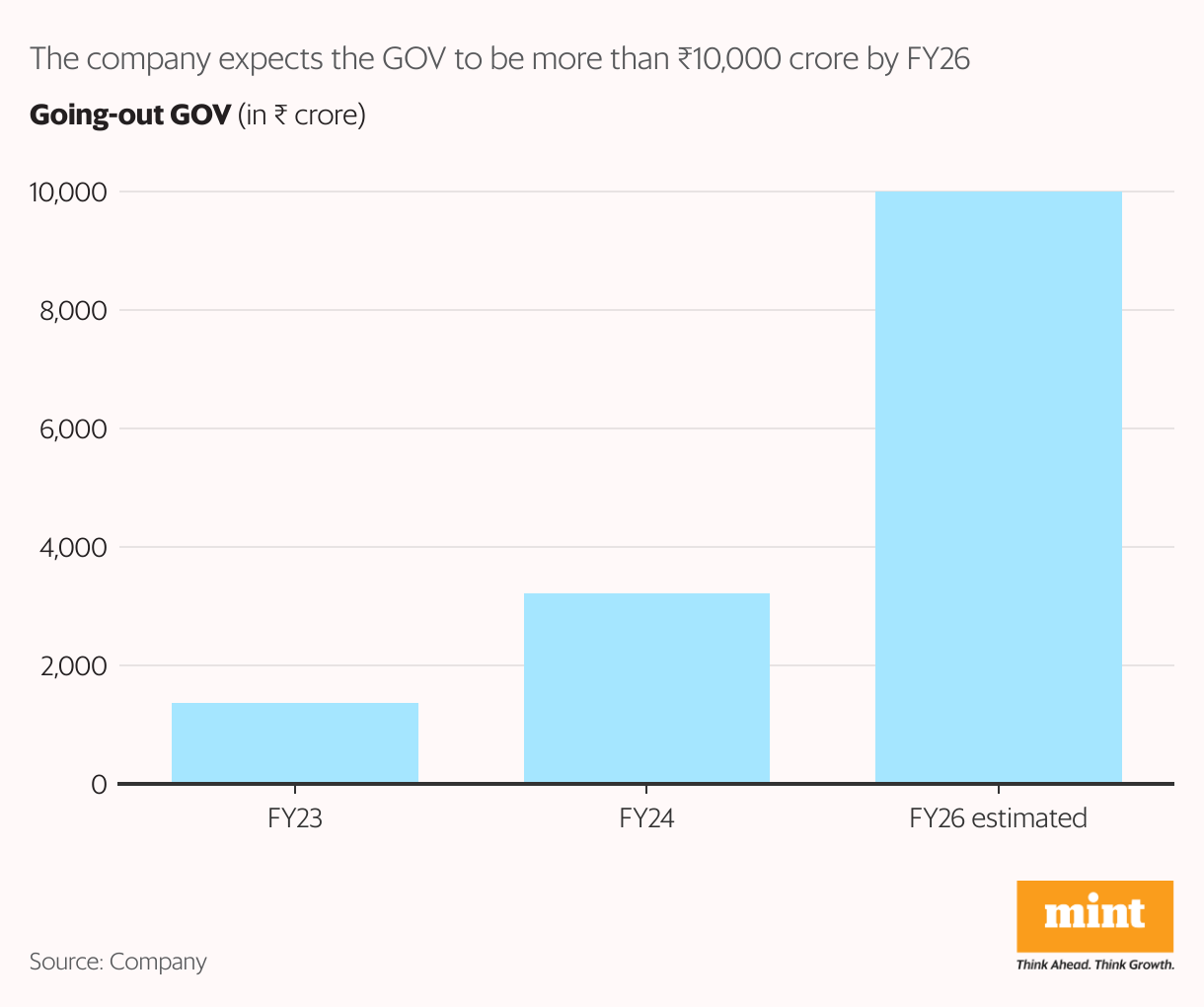

However, Zomato’s preferred parameters for evaluating its businesses are gross order value (GOV) and GOV margin. The acquired business will be housed in Zomato’s going-out vertical, which aims to clock a GOV of more than ₹10,000 crore for FY26.

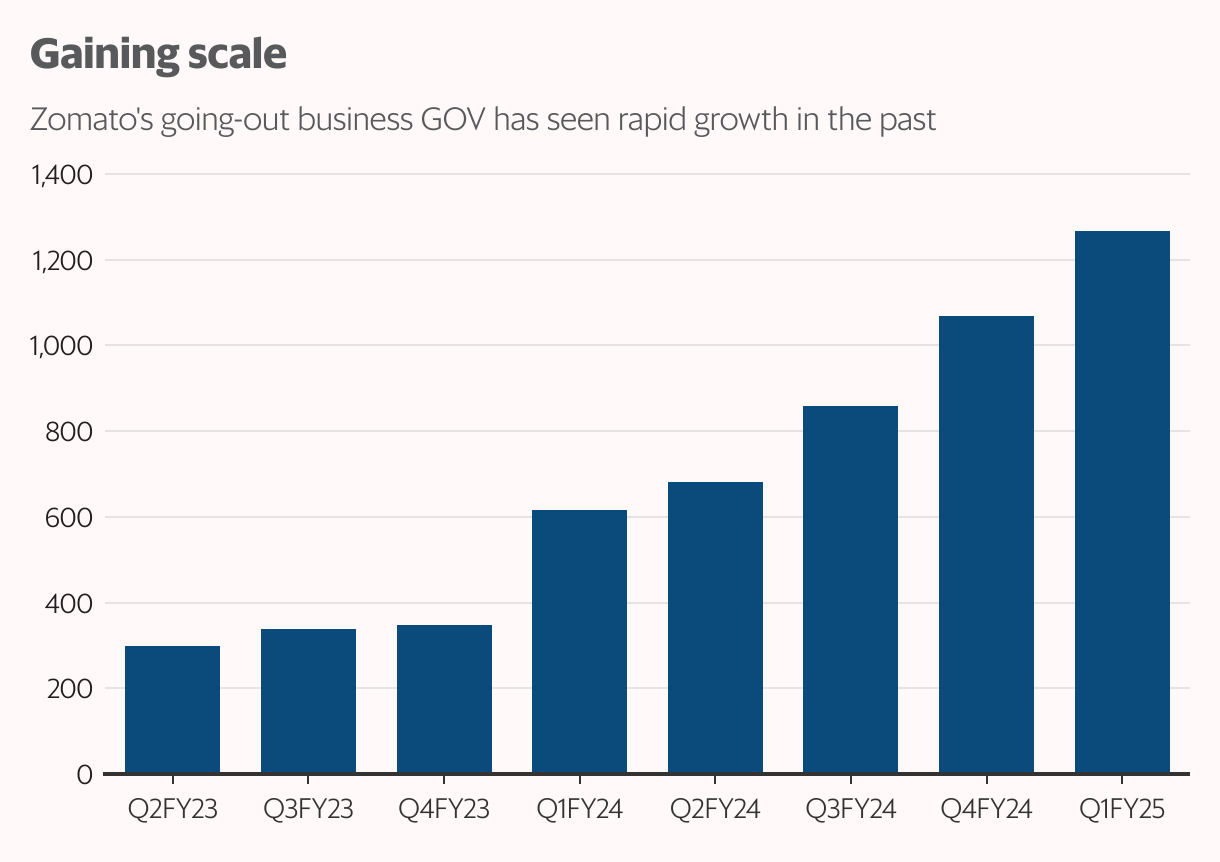

In FY24, the GOV of Zomato’s going-out business was ₹3,225 crore. The GOV of Paytm’s ticketing business was ₹2,000 crore in FY24 with a GOV margin of 1.5%. Thus, The combined GOV of ₹5,225 crore needs to grow at about ₹2,400 crore per year for FY25 and FY26 each. The target is achievable given that the absolute GOV growth for Zomato’s standalone going-out business was nearly ₹2,000 crore in FY24.

Nonetheless, even after FY26, the going-out business will account for just about 10% of the total target price, as per a Jefferies India report that values Zomato stock at ₹335 apiece. The brokerage has valued the business at ₹33,600 crore or 2.5x of GOV based on September 2026 financials.

Also Read: IndiGo: The past, present, and potentially exciting future

Pricey valuations

On an EV-to-Ebitda multiple, however, valuations seem pricey. Zomato’s long-term GOV margin goal for the ‘going-out’ business is 4-5%, which at ₹10,000 crore GOV should mean an Ebitda of ₹400-500 crore. Assuming it is Ebitda positive in FY26, then the EV-to-Ebitda multiple would come to a staggering 65x based on the potential FY26 Ebitda of ₹500 crore as calculated above. However, Jefferies expects an Ebitda loss till FY28. Interestingly, the brokerage had applied a lower EV-to-Ebitda multiple of 55x for the profitable food delivery business based on September 2026 financials.

To be sure, Nomura’s analysts have flagged off integration challenges arising from the acquisition. “Unlike Blinkit acquisition, where the founder and his team were well-known to Zomato management (as they were ex-employees of Zomato), here the acquired team of 280 people is completely unknown," they said in a 21 August report.

Also Read: New launches, Dubai entry elevate Sunteck Realty’s pre-sales outlook

On the other hand, Paytm has got a good deal, having sold the business at a reasonably high valuation of 70x FY24 Ebitda. The transaction increases Paytm’s cash pile to ₹10,000 crore. This could come in handy as Paytm may have to get aggressive for its online payment aggregator business, where it may have to offer incentives to onboard customers from rival platforms like billdesk.com, PayU, etc. More importantly, it will free up the management bandwidth to focus on core areas of payment services and distribution of financial products.

The deal provides strategic gains for both companies even though the impact on share prices is unlikely to be material for the time being.