Market constituents hope for change in Sebi's derivatives plans

")

Recommendations to tighten index derivatives include increasing initial margins, limiting product expiries per week, and increasing contract sizes, potentially impacting NSE volumes by 35-40%.

Market stakeholders suggested mandating a minimum cash requirement for retail investors keen on derivatives trade and permitting multiple product expiries on the same day, in response to the regulator's recent move to tighten the index derivatives framework.

Tuesday was the last day for submitting public comments on the discussion paper that Securities and Exchange Board of India (Sebi) floated last month.

“If you want to protect retail investors, one of the ways of doing it is to keep a minimum requirement of, say, ₹5 lakh cash or cash equivalent for either buying or selling options," said Rajesh Baheti, director, Crosseas Capital, one of India's largest arbitrage and jobbing firms. “Another suggestion is to have multiple index products expire on the same day in place of having just a single expiry per week per exchange."

Baheti said these were part of his comments to Sebi's 30 July consultation paper titled “Measures to strengthen index derivatives framework for increased investor protection and market stability".

Read more: Could Sebi’s curbs for investment advisers choke financial planning in India?

Three of the most important recommendations of Sebi’s Secondary Market Advisory Committee (SMAC) are to increase the initial margin to trade, have only a single product expiry per week per exchange, down from the current five indices which expire each day of week, and increase in contract size from ₹5-10 lakh currently to ₹25-30 lakh.

The initial margin comprises Span and extreme loss margin (ELM). Span is the minimum margin prescribed by the exchange and ELM is over and above that to mitigate any mark-to-market losses.

As per a discount broker, the initial margins for writing options on the expiry day could increase from the current 12-13% to as much as 20-21% if the measure is implemented.

A third broker, requesting anonymity, agreed with Baheti, saying that margins were meant for risk management and not to “control" volumes.

“Our current margin system is robust. We hope that Sebi instead implements a product suitability framework, stipulating a threshold for retail participation in options trading like ₹5 lakh to trade," he said.

Currently, options buyers can trade in options for as little as a few thousands.

Baheti said that allowing multiple option index products to expire on the same day would “square" with Sebi’s objective of not having daily expiries, and thus reduce volatility to a single day instead of every day of week.

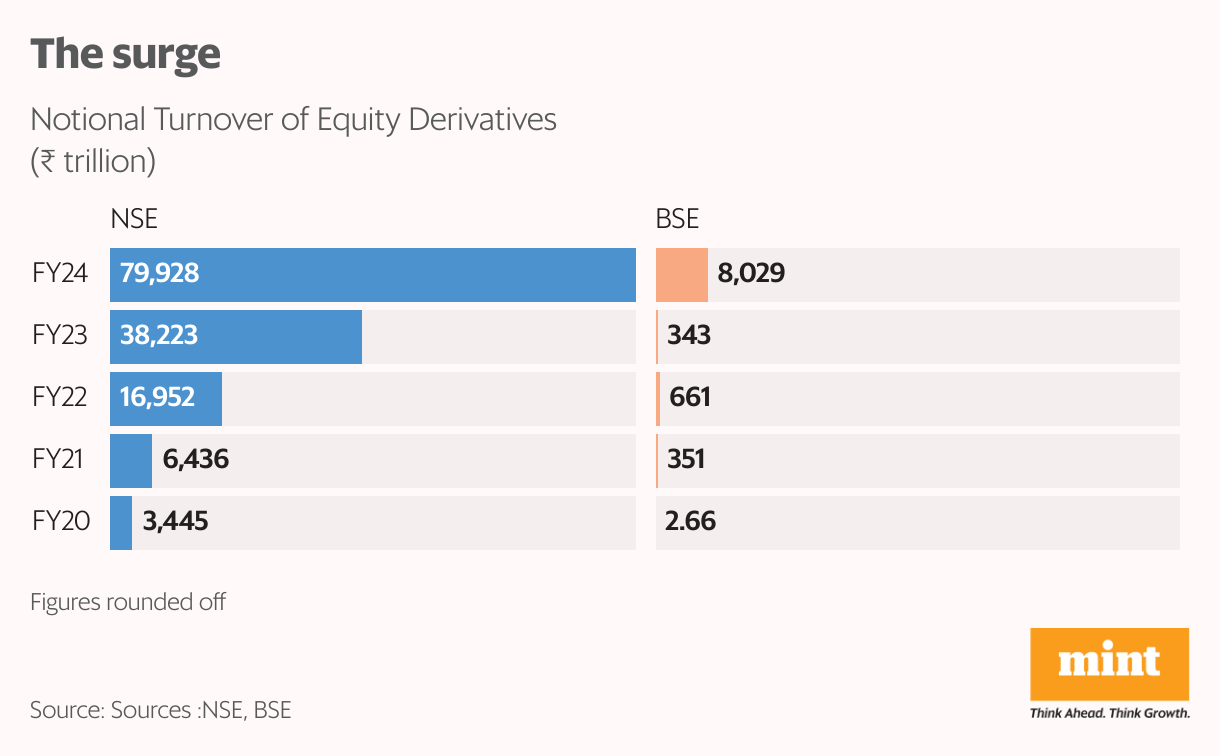

The three measures of increasing margins, having a single expiry per week and increasing contract size could shrink NSE's volumes by 35-40% and increase BSE's volumes by 10%, estimates the broker cited earlier.

This is because market share of NSE in June stood at 78.15% based on notional turnover of ₹7384.37 trillion, while that of BSE stood at 21.85% ( ₹2063.8 trillion). While NSE has four index option expiries per week, including Midcap Select on Monday, Finnifty on Tuesday, Bank Nifty on Wednesday and Nifty on Thursday, BSE’ s most liquid expiry is Sensex options expiring on Friday.

If the measure of having a single product expiry is implemented, NSE is likely to choose Nifty and BSE Sensex. This could have a more adverse impact on NSE, whose other index products will be effectively stopped, and a favourable impact on BSE, which could see a relative increase in volumes, said the broker.

Read more: Should PMS investors switch to focused funds after new tax changes?

Other measures include increasing contract size from ₹5-10 lakh ₹25-30 lakh, increasing strike intervals in options, removal of calendar spread benefit on expiry day of options, collecting upfront margin from option buyers and ensuring that position limits are adhered to by clients on an intra-day basis rather than only by the end of day to reduce extra leverage.

Another person, speaking on the condition of anonymity, said Sebi was likely to implement all seven measures with some tweaks in them. He said these could include reduction in the margin increment.

What raised regulatory concerns was that 925,000 unique individual and proprietary firms who traded index derivatives on NSE incurred a loss of ₹51,689 crore in FY24. Of these investors, 85% made a net trading loss and only 142,000 made a net profit.

The recommendations come on the back of a dramatic hike in securities transaction tax (STT) in the FY25 Union budget by 60% on sellers of futures and options contracts, which will be effective from October 2024.

On the contrary, Anand K. Rathi from MIRA Money said the Sebi measures are in the direction of curtailing retail traders from unnecessarily using it as a mode to get rich. "In my opinion, this may not really impact the market as such, primarily because, yes, in the interim, you may see some derivative trading coming down. But whosoever is left over to remain, whosoever is left over and are remaining because of the transaction size increasing will compensate for the volume loss due to the number of people trading", he said.