Sebi’s seven measures to tame the “tail that's grown bigger than the dog”

")

- Sebi chief Madhabi Puri Buch said “the tail had grown bigger than the dog”, referring to the exponential rise in derivatives volumes on the sidelines of an event organized by the National Stock Exchange.

The chief of India's capital markets watchdog remarked that “the tail had grown bigger than the dog", referring to the exponential rise in derivatives volumes, in response to a Mint query on the sidelines of an event organised by the National Stock Exchange (NSE) on Tuesday.

Minutes later, the Securities and Exchange Board of India (Sebi) released a consultative paper on its website that aims to curb unbridled retail speculation in derivatives (futures and options) by raising upfront margins and doing away with multiple expiries each week.

“Yes, it does look, as somebody said, that the tail is wagging the dog because, ultimately, the F&O was meant to be a way of risk management, hedging, etc.," Sebi chairperson Madhabi Puri Buch said. “Now it has grown much bigger than the dog itself. So, the tail is wagging the dog, (and that) is something that we need to think about."

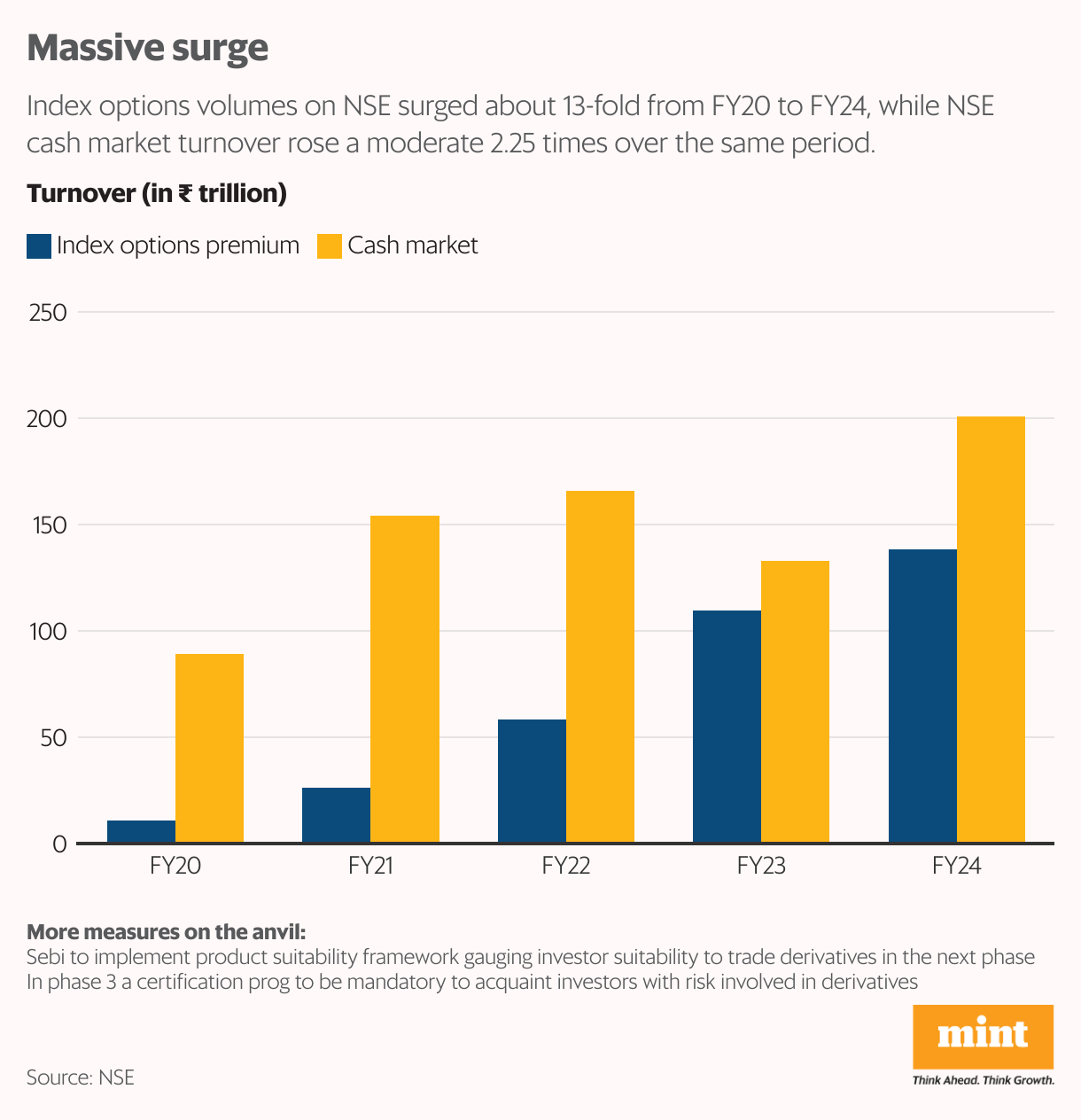

The derivatives rise has been nothing short of spectacular. Index options volumes on NSE, which enjoys over 90% market share, surged almost 13-fold from ₹10.8 trillion in FY20 to ₹138 trillion in FY24. Over the same period, NSE cash market turnover has risen a more moderate 2.25 times, from ₹89 trillion to ₹201 trillion.

- This rapid growth in derivatives trading has raised concerns among regulators about potential market instability and investor protection.

- SEBI has proposed measures, including increasing contract values, raising upfront margins, and reducing the number of weekly expiries.

- The proposed changes could reduce derivatives trading volumes by 25-30%, predict market participants.

- The proposed measures aim to reduce speculation and increase financial prudence among traders.

- SEBI is also considering a product suitability framework and a mandatory certification program for derivatives traders

What raised regulatory concerns was that 9.25 million unique individual and proprietary firms who traded index derivatives on NSE incurred a loss of ₹51,689 crore in FY24. Of these 9.25 million investors, 85% made a net trading loss and only 1.42 million made a net profit.

Measures proposed

In the consultative paper, Sebi has proposed seven specific measures to strengthen the index derivatives framework for increased investor protection and market stability. Comments are invited till 20 August.

The recommendations come on the back of a dramatic hike in securities transaction tax (STT) in the FY25 Union budget by 60% on sellers of futures and options contracts, which will be effective from October 2024.

Of the seven measures suggested to temper retail exuberance, market veterans said the three that could have the highest impact on derivatives volumes, exchanges and brokers are the increase in Nifty lot size and by token in index contract value; increase in the upfront margin to trade; and allowing only one weekly expiry per exchange.

The three key measures

The first recommendation is to increase the contract value from ₹5-10 lakh to ₹15-20 lakh initially, and to ₹20-30 lakh after six months. The margin to trade a Nifty futures contract and to sell a Nifty options contract could increase from around ₹1 lakh to ₹3 lakh if this measure is implemented.

The second measure involves raising the upfront margin on sellers. The margin is a mix of SPAN (minimum amount to pay the broker for taking position) and extreme loss margin (ELM). The ELM is proposed to be increased by 3% a day before expiry of the weekly contract and by 5% on the day of expiry. This could increase total margin (SPAN, which is around 10% of contract value, plus ELM) from 12% to 13% on day before expiry and to 15% on expiry.

The third important measure involves cutting the number of weekly expiries to just one from the current five per exchange. For instance, currently NSE and BSE offer Nifty Midcap Select and Bankex options, respectively, which expire every Monday, Finnifty expires on Tuesday, Bank Nifty on Wednesday, Nifty on Thursday and Sensex options on Friday.

“If the suggestions are implemented, NSE and BSE will be allowed to offer only one expiry per week," said Chandan Taparia, senior vice-president and head – technical and derivatives research, at Motilal Oswal Financial Services. “In all likelihood, this will be Sensex and Nifty options."

Also read | Sebi's unusual decision to return the draft documents of 4 IPOs last week

Rajesh Baheti, managing director at proprietary trading firm Crosseas Capital, said the potential impact of the measures to cut the weekly expiry on NSE could be severe if implemented. “NSE is the much bigger exchange of the two (NSE and BSE) and should have been allowed to offer at least two expiries and BSE just one," said Baheti.

While Taparia expects the volume hit as a consequence of the three measures to be 25-30%, Dhiraj Relli, managing director and CEO of HDFC Securities said it could be hard to “quantify" as having a single expiry per exchange could “consolidate" volumes in a single product (Nifty) that is currently being spread over four products.

Nithin Kamath, founder & CEO of Zerodha, agreed with Relli in a post on social platform X shortly after the release of the paper.

“Whether it is an STT increase in budget or contract size going up to 20 lakhs, these changes will incentivize futures traders to move to options. If the intent is to reduce speculation, then the solution is maybe to make it harder for non-serious people to trade by having a product suitability framework," Kamath said in the tweet.

The other four measures

Three other measures include widening price intervals at out of the money option strikes to make it harder for retail to buy these because of unfavourable risk-reward; removal of calendar spread margin benefit on day of weekly expiry to obviate a speculator selling Nifty on day of expiry and simultaneously buying a Nifty options expiring the next week at half or less the cost of normal margin; intraday monitoring of position limits to ensure participants don’t exceed the set limit by the exchange during a trading session.

The seventh measure involves collecting margin from options buyers upfront by brokers instead of end of day to ensure that additional leverage is not given intraday.

Also read | SEBI cracks down on F&O trading: Here are 7 key measures for retail investors

This will ensure end of extra leverage given by some brokers to clients who pay, say, ₹10,000 per contract to take exposure up to ₹30,000-40,000 intraday , said a broker requesting anonymity.

Going forward, in the next phase, Sebi is likely to implement a product suitability framework gauging investor suitability to trade derivatives, Relli from HDFC Securities said. Following that, in phase three, the regulator is likely to propose a mandatory certification programme to acquaint investors with the risk involved in derivatives.