360 One is pivoting from pure-play wealth to full-stack finance. Will it pay off?

")

Summary

360 One is evolving from a pure-play wealth manager to a full-stack financial platform, with global expansion, acquisitions, and a broader client focus driving its next growth phase.360 One Wealth Management, one of India's leading wealth management firm, has been expanding aggressively. After acquiring ET Money in 2024, the company bought B&K Securities in early 2025, strengthening its institutional broking and research capabilities. More recently, it partnered with global financial giant UBS to tap into offshore wealth and serve international clients more effectively.

These moves point to a clear ambition: 360 One wants to evolve from a pure-play wealth manager into a full-fledged capital markets player. By doing so, it aims to diversify its revenue streams, reduce dependence on wealth flows, and create a more integrated financial services platform.

So, how does 360 One aim to unlock the next growth opportunity through these strategic moves? And how do these bets fit into its long-term plan? Let's take a look.

360 One gains a global edge

The UBS transaction has three parts: a strategic collaboration, UBS acquiring a 4.95% stake in 360 One, and 360 One acquiring UBS's India business.

The partnership will allow clients from both institutions to access a wider suite of onshore and offshore wealth management services. Beyond wealth, both firms see potential synergies in other business lines, such as asset management and investment banking–where cross-border capabilities and client relationships can complement each other.

The second leg of the deal involves UBS subscribing to convertible warrants for a 4.95% stake in 360 One. These warrants are priced at ₹1,030 per share, translating to an investment of ₹2,112 crores for 2.05 crore warrants.

For UBS, this points to a broader India strategy, particularly as global wealth managers like Julius Baer and HSBC are stepping up their India presence. Many global firms have historically struggled to scale in India due to intense competition, high client expectations, regulatory complexities, and talent constraints. By partnering with a market leader like 360 One, UBS may be better positioned to navigate these challenges.

The deal strengthens 360 One's value proposition for domestic and international clients. Importantly, the scope of the partnership goes beyond capital. The wealth management opportunity coming through the partnership is significant. According to management, 360 One's non-resident Indian (NRI) book exceeds ₹17,000 crores ($2 billion)—even without a dedicated NRI sourcing office.

However, 360 One sees strong demand with the partnership, especially in the alternative segment. With growing awareness & use of GIFT City, the company sees strong potential for 3x AUM growth in the coming years.

The final piece of the transaction is 360 One's acquisition of UBS's India business for ₹307 crore. This includes business transfer agreements covering distribution and broking business, portfolio management (PMS), and the loan book. The deal involves a complete transfer of clients, with ₹26,000 crore AUM, generating annual revenue of about ₹75 crores.

While UBS's India wealth business is significantly smaller than 360 One's, the acquisition will add scale to AUM and contribute positively to revenue and net flows. Though not materially earnings-accretive in the near term, it opens up long-term growth opportunities, especially when the number of high-net-worth individuals is expected to explode in India.

To fulfil these ambitions, the company will strategically deploy the funds raised ( ₹2,112 crore) from the UBS stake sale. It has earmarked ₹300-350 crore for UBS collaboration, ₹200-250 crore for enhancing B&K Securities, ₹800-900 crore for the loan book, and the rest for strengthening the alternatives business.

Also Read: Motilal Oswal needs to find its next growth engine. Here’s what it’s betting on.

B&K Securities acquisition adds heft

In addition to the UBS deal, 360 One also signed an agreement to acquire Batliwala and Karani (B&K) Securities for ₹1,884 crore, including ₹200 crore in cash. B&K operates across institutional broking, equity capital markets (currently being built out), and corporate treasury.

Over the past few years, it has more than doubled its revenue, from ₹110 crores in FY22 to ₹281 crore in FY25. Net profit stands at ₹102 crore, making the deal earnings accretive by 6% (360 One FY25 PAT of ₹1,015 crores).

B&K is a leading full-service broker, with a strong institutional client base–both foreign and domestic. The acquisition is expected to strengthen 360 One's presence across capital markets and help it offer clients a complete range of services. The management believes capital markets will remain a key area of client activity for the next 10-15 years.

One of the key opportunities lies in broking. 360 One aims to increase equity broking's contribution in its transaction and brokerage revenue (TBR) mix, from around 12% in the first nine months of FY25 (9MFY25) to 40-50% over time.

It aims to expand research coverage from 400-450 stocks to 600, benefit from B&K's annualised brokerage revenue of ₹190 crore (9MFY25), and tap into equity clients like family offices and AIFs. The management expects the equity broking segment to grow at 15–25% CAGR over the next three–five years.

360 One sees material synergies in the corporate distribution business. B&K is a key player in this space, which could create great synergy when paired with 360 One's product portfolio. However, given that investment banking is still nascent, growth is expected to be slower. Nonetheless, in the long run, strong relationships with corporations will drive growth in the investment banking business.

Solid finish to FY25

360 One's total assets under management grew a strong 25% from last year to ₹5.8 trillion in FY25, supported by strong net inflows of ₹25,974 crore, despite market volatility. Of the total AUM, 85% came from the wealth management (including ₹33,055 crore from ET Money), while the remaining 15% came from the asset management segment.

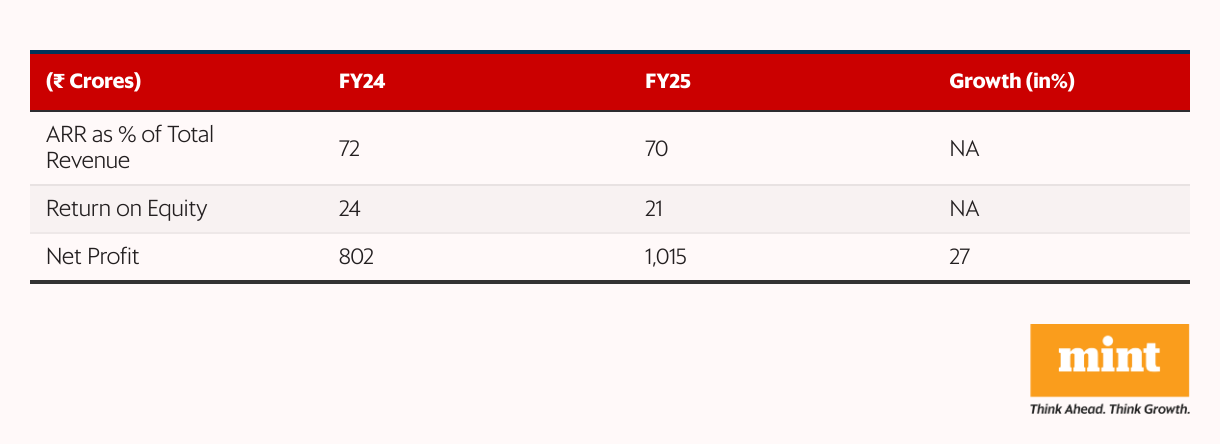

Average annual recurring revenue (ARR) AUM also increased 26% and now accounts for 40% of the total AUM, up from 37% last year. With a steady ARR retention of 0.73% (revenue earned as a percentage of average assets), ARR-linked income grew by 28% and now contributes 70% of revenue.

This shift improves earnings visibility and reduces dependence on volatile brokerage and transaction fees, which make up the remaining 30% of revenue. On the profitability side, the cost-to-income ratio declined 2.8 percentage points to 45.9%, aided by scale benefits. As a result, net profit rose 27% to ₹1,015 crore. The management anticipates a gradual decline in this ratio as new business becomes more productive.

Also Read: Samhi's GIC deal may accelerate growth. Could a valuation rerating follow?

What's next?

360 One primarily serves ultra-high-net-worth individuals with investable surpluses of over ₹25 crore. However, it recently expanded into the mid-market HNI segments ( ₹5-25 crore) to broaden its client base.

The company has also entered global markets and expanded into cities beyond Tier-1. While both are early-stage efforts, they align with industry trends and demographic shifts as more HNIs and affluent Indians emerge outside metros.

With these growth drivers, the management targets annual ARR inflow growth of 12-15% and mark-to-market growth of 8-10%. This is expected to translate to AUM growth of 20-25%, revenue growth of 15-20%, and PAT growth of 20-25% annually.

That said, equity dilution from recent transactions–including the UBS stake issuance and the B&K acquisition–could weigh on return on equity in the near term.

Long runway, but execution critical

360 One continues to hold a strong position in the wealth management industry. Its focus on diversifying across client segments (including mass affluent) and geographies (beyond Tier-1 cities) is gaining traction. While the global business is still in early stages, the UBS partnership is expected to fast-track the scale-up.

In parallel, acquiring B&K Securities will enhance 360 One's capital markets offerings and is expected to be EPS-accretive from the beginning. With multiple integrations underway–including mid-segment HNI expansion, global foray, ET Money, B&K, and UBS- execution will be critical.

The company currently trades in line with the 10-year median price-to-earnings multiple of 34x. While the long-term opportunity in wealth management remains intact, declining return ratios due to dilution and market volatility may have kept the share price range-bound in the near term.

For more such analyses, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The author holds the stocks discussed in this article. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.