Adani Ports bets big on doubling revenue by FY29. But execution is everything.

")

India’s largest port operator is targeting ₹65,500 crore in revenue by FY29, backed by aggressive domestic expansion and a global logistics push. The plan is bold—its success will depend on staying the course.

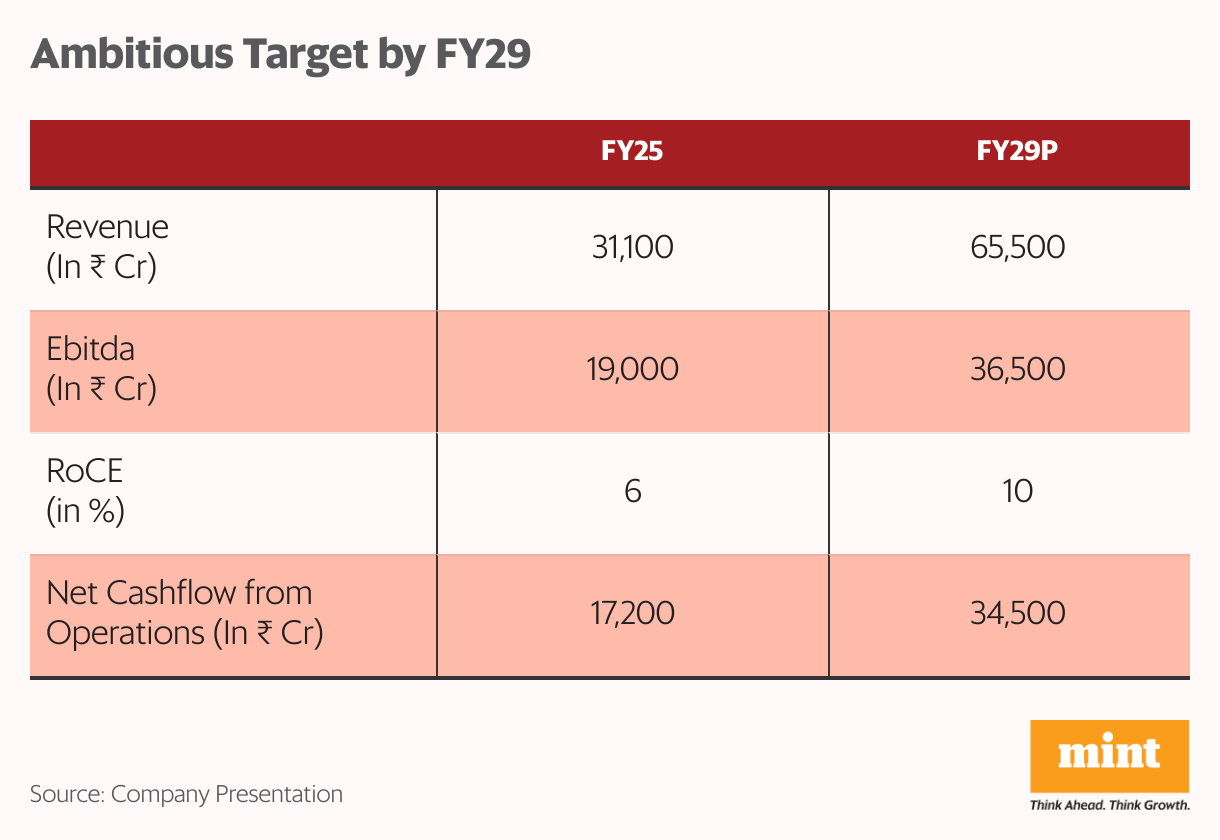

India’s largest port operator has set itself an ambitious target: double revenue, Ebitda, and operating cash flow by FY29. After a strong FY25 performance, Adani Ports and Special Economic Zone Ltd is betting on a mix of domestic capacity expansion, global acquisitions, and rising logistics volumes to deliver this multi-year growth.

The company ended FY25 with revenue of ₹31,100 crore, up 14% from the previous year, and net profit of ₹11,061 crore, up 37%. Now, it’s gunning for ₹65,500 crore in revenue, ₹36,500 crore in Ebitda (up from ₹19,000 crore), and ₹34,500 crore in operating cash flow (up from ₹17,200 crore) over the next four years. A ₹75,000 crore capex plan has been lined up to support this aggressive push.

Read this | We are generating more cash than we know how to use: Adani Ports MD Karan Adani

But while the building blocks are in place, execution will be key.

Domestic cargo volumes underpin growth

Cargo volumes hit a record 450 million metric tonnes (MMT) in FY25, rising 7% year-on-year. Domestic cargo, which makes up the bulk of this, grew 5% to 431 MMT. International volumes, still a small share, surged 72% to 19 MMT.

That helped Adani Ports expand its all-India market share slightly, from 26.5% to 27%. The company now aims to nearly double overall cargo volumes to 1,000 MMT by 2030.

India buildout is the foundation

Of the ₹75,000 crore capex plan, ₹45,000–50,000 crore is earmarked for domestic port infrastructure. Adani expects domestic cargo to rise from 633 MMT to 850 MMT by 2030, largely via organic capacity additions.

The company already holds environmental clearances for 1,560 MMT across its ports, allowing fast expansion without new regulatory hurdles. Key upcoming projects include container terminals at Mundra and Vizhinjam, a multi-commodity berth at Dhamra, multipurpose berths at Hazira, and expanded Ro-Ro capacity.

Investments will also go into port connectivity and evacuation infrastructure, prioritising terminals linked to customer demand and upcoming industrial corridors.

East-West corridor powers global push

Adani Ports expects its international business to contribute 150 MMT toward its 1,000 MMT volume goal. Its overseas expansion strategy targets majority control, strong profitability, and alignment with the East-West corridor—a vital trade route linking East Asia with Europe, the Middle East, and Africa, and accounting for ~60% of global trade.

Ports like Mundra (West coast) and Dhamra (East coast) are well-positioned to capture this traffic. The company has also established operations in Haifa (Israel), Dar es Salaam (Tanzania), and Colombo (Sri Lanka), with the latter two having gone live in FY25.

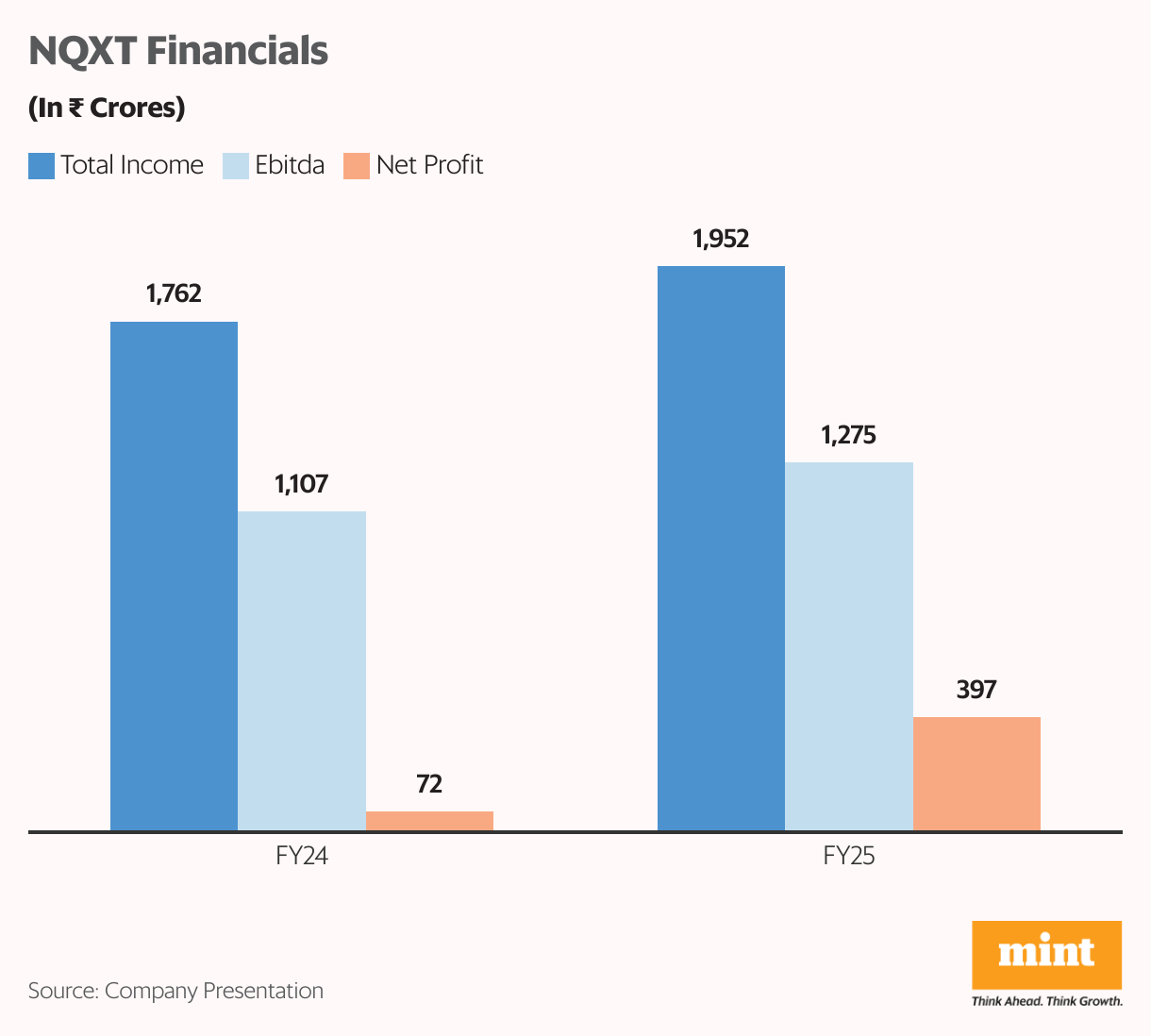

A major piece of the global puzzle fell into place in April with Adani Ports’ acquisition of the North Queensland Export Terminal (NQXT). The asset supports the company’s 1,000 MMT vision and is expected to add 15% to total volumes.

NQXT operates under long-term take-or-pay contracts and currently runs at 85% utilisation. Most cargo is Asia-bound. In FY25E, the terminal posted ₹1,952 crore in revenue (up 10.7%) and ₹1,275 crore in Ebitda (up 15%). Adani projects Ebitda to rise to ₹2,237 crore in four years as capacity scales up to 120 MMT.

The terminal may also evolve into a green hydrogen export hub, given its location in resource-rich Queensland. The deal is earnings-accretive from the outset—adding 6% to consolidated revenue and 7% to Ebitda. (Figures converted at ₹55.94/AUD.)

Read this | Adani Ports’ international expansion gets a leg up with Abbot Point deal

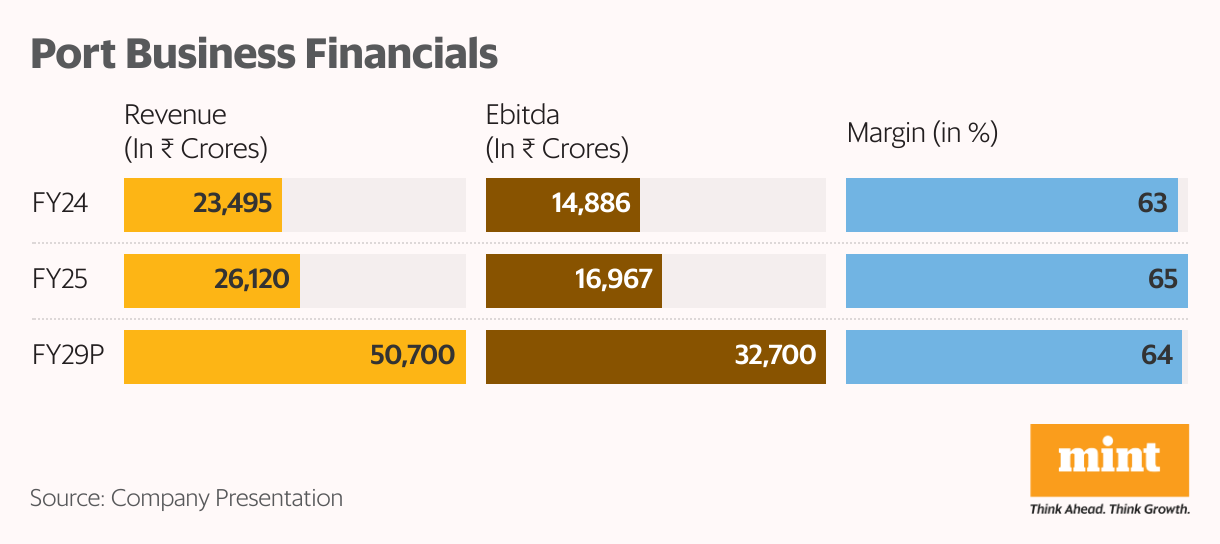

By FY29, Adani Ports expects its port revenue to nearly double to ₹50,700 crore, compared to ₹26,120 crore, with Ebitda rising to ₹32,700 crore, from ₹16,967 crore. Margins are likely to stay stable at around 64%.

Logistics business expansion

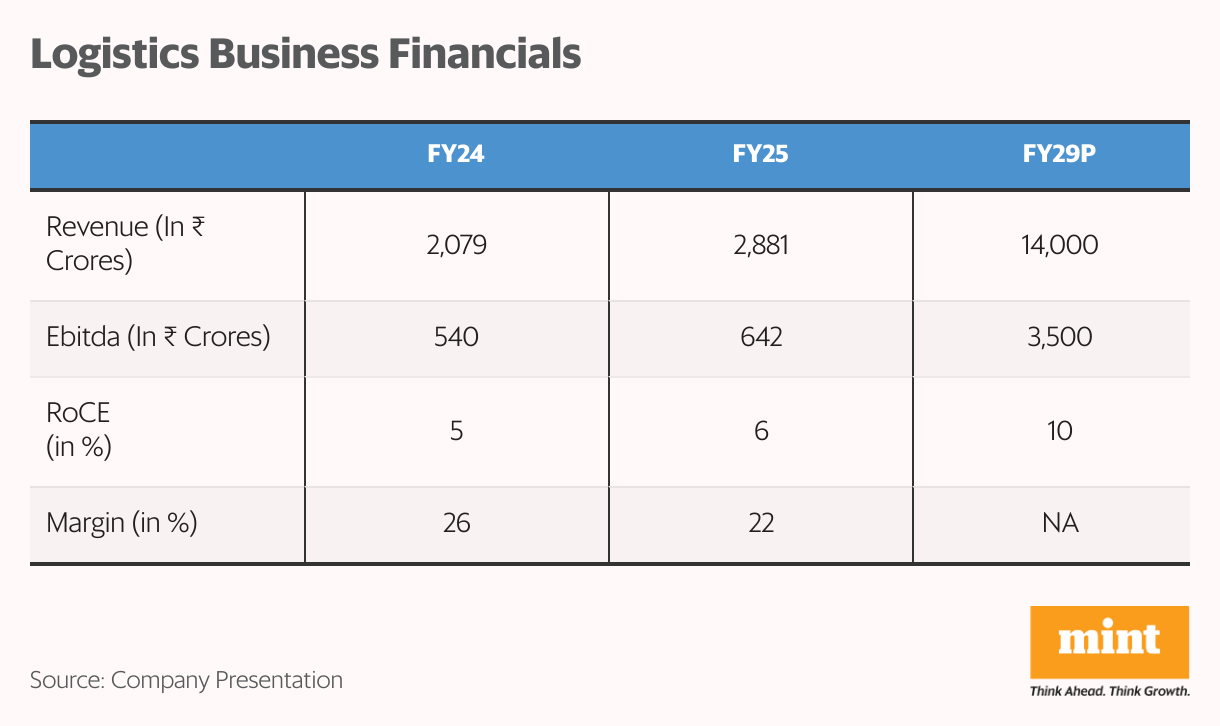

Adani’s logistics arm posted 39% revenue growth in FY25 to ₹2,881 crore, with Ebitda up 19% to ₹642 crore. Margins fell 400 basis points to 22%, but the company is confident of improving operational efficiency and return on capital.

The logistics roadmap targets ₹14,000 crore in revenue and ₹3,500 crore in Ebitda by FY29. A ₹15,000–20,000 crore investment will scale up rakes (from 132 to 300), logistics parks (12 to 20), trucks (937 to 5,000), warehousing (3.1 to 20 million sq. ft.), and agri silos (1.2 to 10 MMT).

Strong capital discipline underwrites growth

Despite the scale of its ambition, Adani Ports has maintained a conservative financial stance. Net debt-to-Ebitda stood at 1.9x in FY25, well within its 2.5x ceiling. Operating cash flow is expected to exceed planned capex, reducing reliance on debt.

Free cash flow as a share of gross debt rose from 28% to 34% over the past year, and interest coverage improved from 5.6x to 7.1x.

Premium valuation signals investor confidence

The stock currently trades at 30x earnings, above its 10-year median of 23x but below JSW Infrastructure’s 44x. The valuation premium reflects investor belief in its long-term visibility and integrated model.

India’s high logistics costs—14% of GDP versus 8-10% in developed economies—also present a structural opportunity. As infrastructure upgrades kick in, Adani Ports stands to benefit more than most.

Also read | This pharma stock surged 10X, crashed 60%, and rose to an all-time high again. Can it sustain the momentum?

Can Adani Ports pull it off?

The targets are steep. But Adani Ports has a few key advantages: a dominant domestic position, regulatory clearances already in hand, and a growing international footprint. The logistics business, though less mature, is being scaled aggressively.

For more such analysis, read Profit Pulse.

If it executes on schedule, doubling revenue, Ebitda, and cash flows by FY29 is within reach. But the real test lies in delivering consistently—across geographies, asset classes, and economic cycles.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.