Backed by giants, bleeding cash—is Ather Energy ready for IPO?

. File photo: Reuters")

With strong backers, cutting-edge tech and a growing charging network, Ather is one of India’s most ambitious EV bets. But with widening cash burn and rising competition, its IPO will test how far investor conviction can go.

India’s electric two-wheeler race is entering a new phase—and one of its earliest disruptors is now testing investor faith.

Ather Energy, known for its tech-led scooters and premium positioning, is headed for a public debut next week. As competition intensifies and capital becomes dearer, the initial public offering (IPO) marks a crucial inflection point for both the company and the broader EV ecosystem.

Backed by Hero MotoCorp and marquee investor Tiger Global, Ather is aiming to raise fresh funds and widen its shareholder base. But while it has made strides in technology, manufacturing and customer experience, persistent losses and cash burn raise questions on scalability and sustainability.

Read this | What an IPO signals about Ather's battle against Ola Electric

Let’s take a closer look.

IPO brass tacks

Ather’s public issue is expected to revive India’s primary markets, which have seen subdued activity in recent months.

The company had filed its draft red herring prospectus (DRHP) back in September 2024, but tepid market sentiment led to delays. Since then, Ather has trimmed its valuation expectations twice—from ₹17,000– ₹20,000 crore to around ₹12,000 crore.

The company plans to raise ₹3,000 crore, including a ₹2,626 crore fresh issue and a ₹355 crore offer for sale (OFS). Hero MotoCorp, which holds over 38% in Ather, is not selling any shares in the OFS—a potential vote of confidence for public investors.

Proceeds from the issue will go toward a new manufacturing plant in Maharashtra and R&D investments. Plans to partly prepay ₹534 crore of outstanding debt have been scaled back, thanks to a stronger recent performance.

The IPO, managed by Axis Capital, HSBC, JM Financial and Nomura, is priced in the ₹304– ₹321 range and will remain open from 28 April to 30 April.

Read this | Will Ather’s fate be similar to Ola’s? Analysts are more cautious than optimistic.

While Ather remains loss-making, industry tailwinds, its backers, operating track record, and strong focus on product innovation and after-sales service could help anchor valuations in the absence of traditional metrics.

India’s electric two-wheeler shift gains momentum

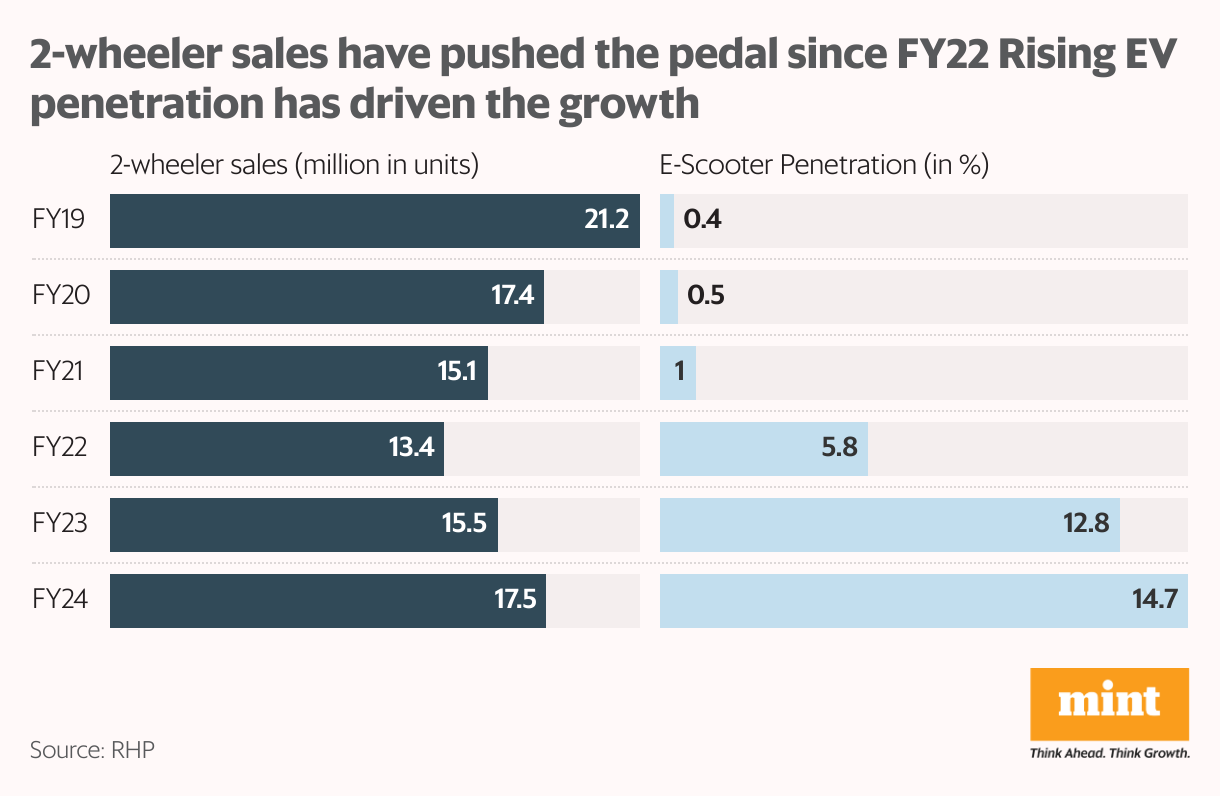

India’s two-wheeler (2W) market was already slowing when the pandemic hit. Post-lockdown pent-up demand, infrastructure-growth, and urbanisation trends have kept two-wheeler sales on the upswing, while delayed upgrades to four-wheelers amid slow rural growth have helped as well. From 106–108 vehicles per 1,000 people in FY19, two-wheeler penetration has risen to 116–118 in FY24.

Electrification is progressing in tandem.

Driven by growing climate awareness, lower running costs and the government’s FAME II and PM E-Drive subsidies, electric scooter sales have jumped from 0.4% penetration to 14.7% in just a few years. Between FY19 and FY24, conventional 2W sales fell at 3.7% CAGR, while E2Ws surged at 101.7% CAGR.

Read this | Can two-wheelers stay on the pedal in 2025?

Looking ahead, premiumization, new launches and higher financing penetration amid continued rural demand recovery is expected to support 2-wheeler sales. While the cost of ownership for electric two-wheeler (E2W) is 37% lower than their conventional counterparts (55%, incorporating subsidies), the acquisition cost is about 40% higher.

The acquisition-cost gap is expected to shrink to just 7% by FY31. Falling prices of batteries which constitute about 30% of an E2W cost, other technological advancements, and improving economies of scale are expected to drive down the costs of acquisition as well as ownership.

E2W sales would continue to grow at full throttle as government initiatives encourage legacy players to enter the market and incumbents to expand capacity. Moreover, expansion of charging infrastructure is likely to assuage range anxiety. Driven by 41% CAGR growth between FY24 and FY31, E2W penetration is penciled in at 35% by FY31.

The cash-burn paradox

Cash-burn in the early years, particularly in a disruptive industry such as EV, is par for the course. But as the investments made towards scaling up manufacturing, distribution, and servicing, as well as product and brand development start paying off, the company turns profitable. For instance, Tesla piled up losses for six years before turning Ebitda positive in 2013.

Ather has been a technological disruptor in E2W right from the beginning. Apart from its pioneer 450 model that matched conventional power, its long-list of industry-firsts include cloud integration, touchscreen dashboard with navigation, smart helmets, and guide-me-home lights.

More importantly, its innovations have been guided by customer intelligence received from its integrated information systems aka Atherstack. It invested 15% of its revenues towards R&D in 9MFY25, against only 7% towards marketing. It sports 45 registered and 303 pending patent applications.

Read this | Banks have had a rough ride, but some bucked the trend

Ather’s R&D focus and premium offerings have helped it gain ground despite aggressive expansion by the likes of Ola and Bajaj. But these innovations have come at a cost. Notwithstanding premium pricing, the company has been accumulating losses and bleeding cash since inception.

While the losses have shrunk in the first nine months of FY25, operating cash outflows accelerated during the period. It reported operating cash outflow of ₹717 crore in 9MFY25, significantly higher than the outflow of ₹268 crore seen during the full year FY24.

Capex and new launches to fuel growth

Ather is betting on fresh capex and new models—like the recently launched Rizta—to scale its operations.

Its current annual capacity of 420,000 electric two-wheelers and 379,800 battery packs will be expanded with the help of IPO proceeds. The planned manufacturing facility in Maharashtra offers strategic advantages: high EV adoption in the region and proximity to component suppliers.

But as EV adoption scales up, concerns over charging infrastructure and service quality are mounting across the industry. Ather appears better positioned to weather this challenge. Its fast-charging network, Ather Grid, is India’s largest for two-wheelers and is complemented by portable home chargers. Its asset-light network of service and experience centers supports rapid expansion while helping maintain customer trust and brand perception.

Margins gain from scale and tech integration

Ather’s focus on in-house design and growing scale has helped cut production costs and improve margins—despite the sharp rollback in government subsidies. FAME incentives for electric two-wheelers have dropped 77% between FY22 and 9MFY25, but Ather’s gross margin rose from 7% to 19% in the same period.

Another contributor to its improving margin profile is its high-margin ecosystem offerings. In 9MFY25, non-vehicle revenue—comprising accessories and Atherstack services—accounted for 12% of the sale value per unit. Atherstack, in particular, clocked a 53% Ebitda margin, helping narrow overall losses.

But risks loom

A rollback of government incentives could slow EV adoption, and legacy players with deeper pockets are better equipped to ride out such policy shocks. Ather, though a pure-play EV firm, benefits from the deep-pocketed support of Hero MotoCorp—its largest shareholder.

However, Hero is also facing legal headwinds. A ₹10,144 crore litigation, if it results in material liability, could have spillover effects on Ather’s financial flexibility and perception.

There are operational risks too. Ather outsources manufacturing of all components except batteries, making it vulnerable to supplier-side disruptions. This dependence is further amplified by its reliance on Chinese imports for lithium-ion cells. Any shifts in localization norms or geopolitical tensions could disrupt supply chains and inflate costs.

Finally, thanks to a changing dealership landscape for E2W, the company has had to start operating a handful of its experience and service centers under the company-owned, company-operated (COCO) model. While this model allows tighter control over customer experience, it entails higher upfront capex and operating expenses. At current scale, it has been margin-dilutive.

Correction: An earlier version of this piece suggested the electric-two-wheeler market operates solely under the company-owned-company-operated dealership model. The error is regretted.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.