BSE: From bear market bait to global investment darling. Will it hold?

")

- Derivative strength has kept BSE afloat amid market turmoil, but mid- and small-cap weakness poses near-term risks. As regulatory shifts reshape trading dynamics, the exchange is betting on higher-margin contracts to sustain growth.

The December quarter was brutal for investors, with the market slumping 7.3% and portfolios deep in the red. Yet, one investor found an unlikely lifeline: BSE. The market barometer helped ace investor Mukul Aggarwal weather the storm, providing a rare bright spot amid the downturn.

Trendlyne data shows that the BSE stock, comprising nearly 14% of Aggarwal’s portfolio, surged 22% in Q3FY25, driving his net worth higher.

In fact, this former lifeline is still holding fort as the broader mid- and small-cap segment languishes in bear territory.

The stock is up almost 7% year-to-date, driven by an 8.5% rally on Wednesday which extended into Thursday as well. Shares climbed 3% in intra-day trade for the second consecutive session, after global investment firm Goldman Sachs acquired a ₹401 crore stake in the exchange through an open market transaction.

Read this | Bullish or bearish? Mint survey gauges market mood amid volatility

Investors seem to have found comfort in the company’s record third-quarter performance and are betting on a further increase in the exchange's market share in both derivative and cash market trading segments in the medium-to-long term, experts said.

BSE's revenue hit an all-time high and profit doubled year-over-year, largely driven by the success of BSE Star MF—its web-based mutual fund distribution platform, which saw a 92% revenue jump.

Cracks beneath the surface

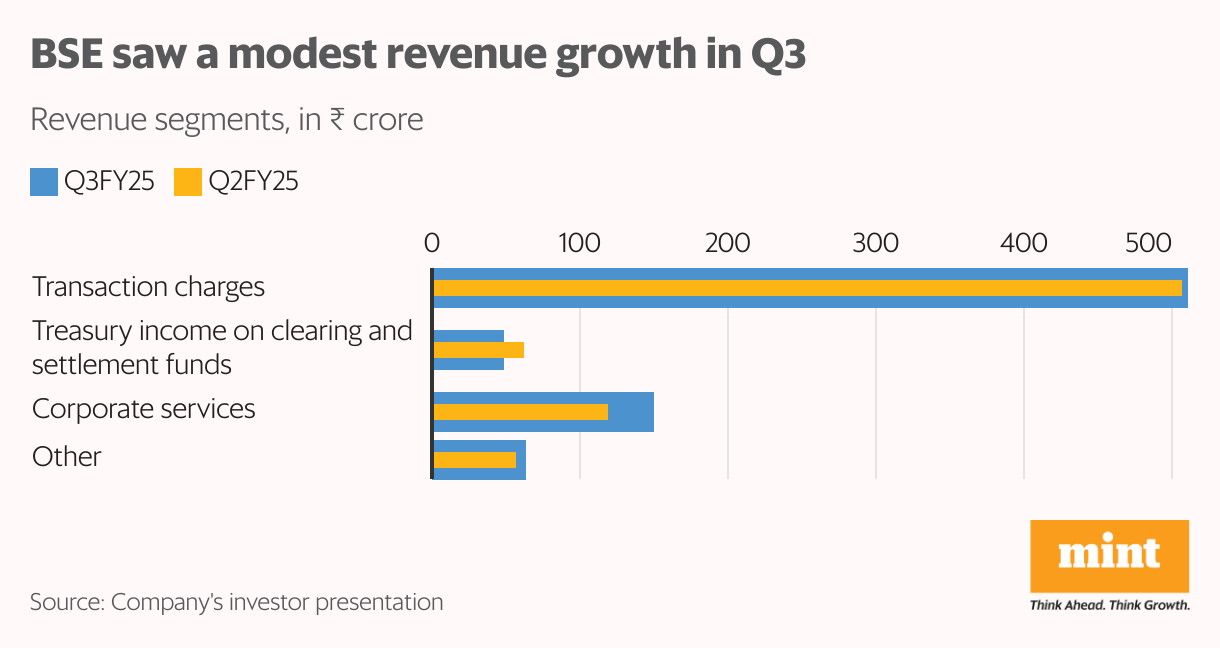

While BSE's yearly performance looks strong, sequential data reveals a different story. Revenue growth slowed to just 3.6% quarter-on-quarter—the weakest in six quarters—hurt by a 22% drop in cash volume and lower treasury income from clearing funds.

Chandan Taparia, head of equity derivatives and technicals at Motilal Oswal Financial Services, attributes this to profit booking in mid- and small-cap stocks and a shift in trading interest to outperforming assets like gold.

Adding to the pressure, BSE’s adjusted net profit fell 37% sequentially in Q3, as a ₹200 crore contribution to the Settlement Guarantee Fund (SGF) eroded earnings.

While HDFC Securities notes that management doesn’t expect similar SGF contributions in the near term, the brokerage warns of a gradual rise as BSE expands market share and shifts to longer-duration contracts.

Read this | As BSE navigates regulatory shifts, does its valuation leave room for an upside?

Even though experts remain divided on whether such contributions will rise in the future, they agreed that current bearish sentiments in the market will keep business subdued for the exchange in the near term. Market participants anticipate a further downside, projecting a 15-25% sequential drop in BSE’s earnings for the March quarter.

“I think this scenario will continue over the next couple of months. Only if the market sentiment changes then overall trading activity will increase," Taparia noted.

Mid- & small-cap woes

The turmoil in the mid- and small-cap space, coupled with still-rich valuations despite recent corrections, could weigh on BSE’s stock.

“BSE has a larger share of mid- and small-cap companies compared to NSE and in a bear market there is less inclination from retail investors to trade in these segments," highlighted Puneet Sharma, CEO and fund manager at Whitespace Alpha, a category III alternate investment fund.

“Given that these segments remain overvalued relative to their historical averages, even after the ongoing correction, there could be more fall and lesser trading in the market in the short term," he added.

Read this | The retail investor bloodbath in smids might just be the beginning

However, the volatility could also present an opportunity. Increased market uncertainty might drive more foreign institutional investors (FIIs) toward derivative trading, supporting BSE’s revenue growth in Q4, Sharma added.

Derivatives strength

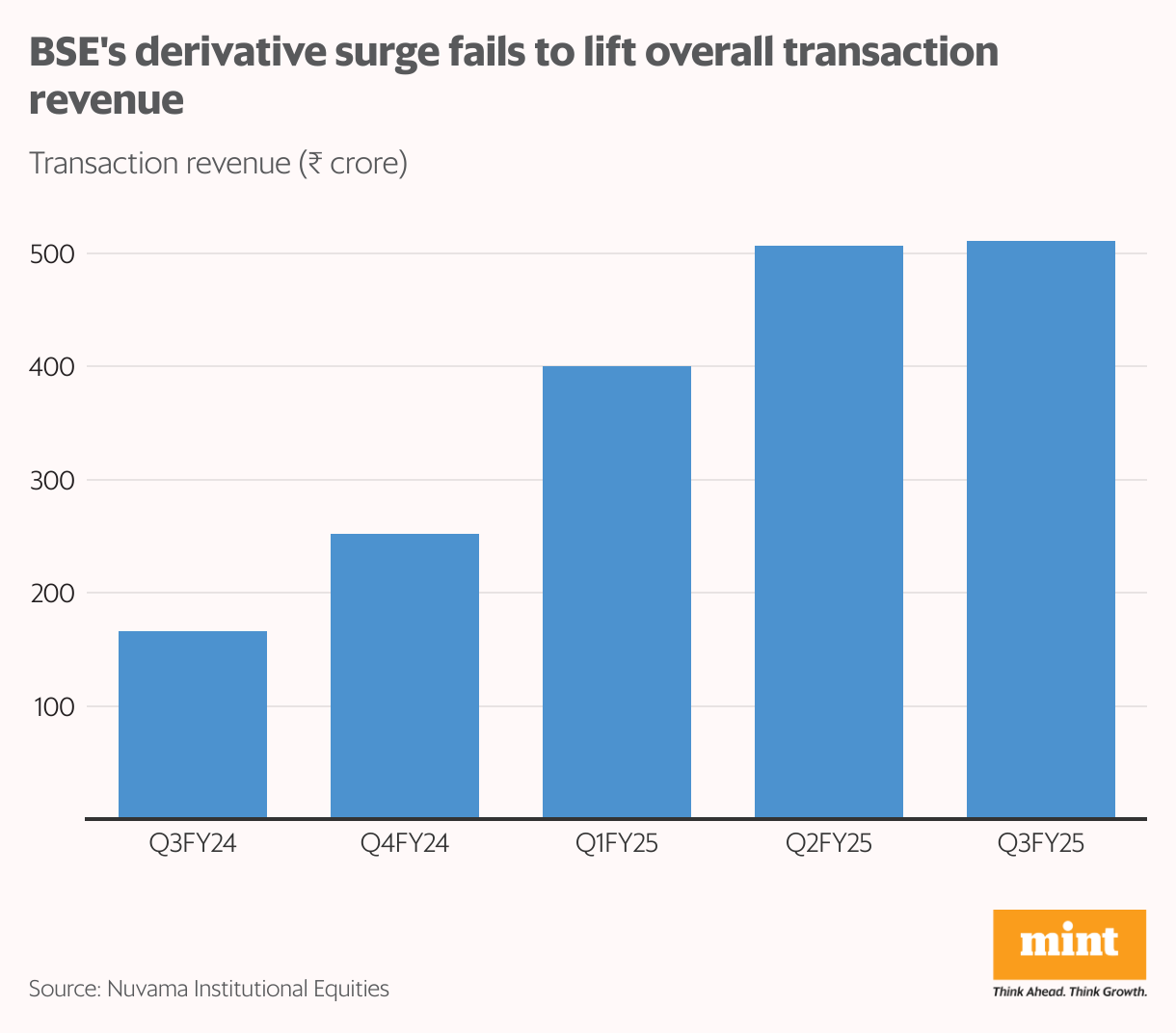

Last year’s surge in retail derivative trading kept sentiment around BSE strong. A steady rise in transaction charges from futures and options trades reassured investors of the exchange’s earnings growth trajectory. Even when the Securities and Exchange Board of India (Sebi) introduced a set of measures on 1 October 2024 to curb excessive derivative speculation, market participants remained unfazed—a bet that appears to have paid off, at least for now.

Despite Sebi’s phased rollout of these regulations, BSE posted a record-high average daily premium turnover of ₹8,800 crore in Q3. It even gained market share, with options trading rising to 12.5% from the previous quarter, signaling that interest in derivatives remains robust.

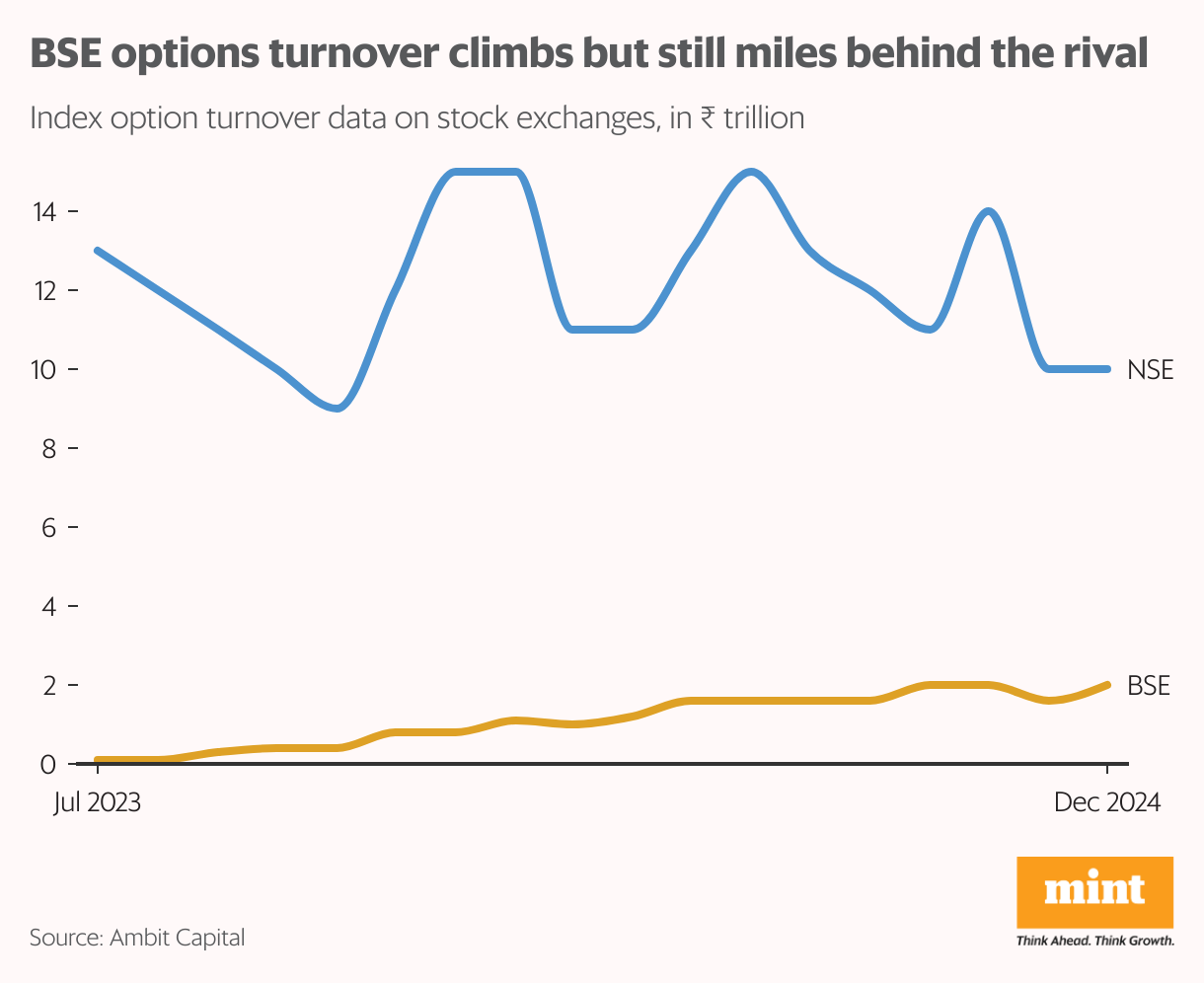

As competition in the derivatives segment intensifies, BSE has outpaced the National Stock Exchange (NSE) in month-on-month growth. This momentum has further supported BSE’s stock performance.

Thirteen days into February, BSE’s average daily turnover had risen nearly 20% over January, albeit from a lower base, while NSE saw a nearly 5% decline.

Analysts note that while abolishing weekly expiries for certain contracts will reduce overall trading volumes, it will also cut clearing and regulatory costs for exchanges. In fact, BSE’s Ebitda margin improved by 420 basis points sequentially to 56.3%, aided by an 18% and 13% quarter-on-quarter decline in clearing and regulatory expenses, respectively.

Additionally, a shift toward longer-duration derivative contracts, prompted by regulatory changes, could further boost BSE’s revenue. Longer-term contracts carry higher premiums due to their riskier nature, leading to increased transaction charges for exchanges.

“Lower number of orders and higher premium turnover due to new F&O regulation is expected to lower clearing and settlement costs (for BSE), resulting in (its) margin improvement in the medium term," said Rahul Malani, equity research analyst at Mirae Asset Sharekhan.

Malani estimates BSE’s revenue and EPS to grow at compounded annual growth 26% and 33% CAGR respectively over FY25-27.

Near-term headwinds persist

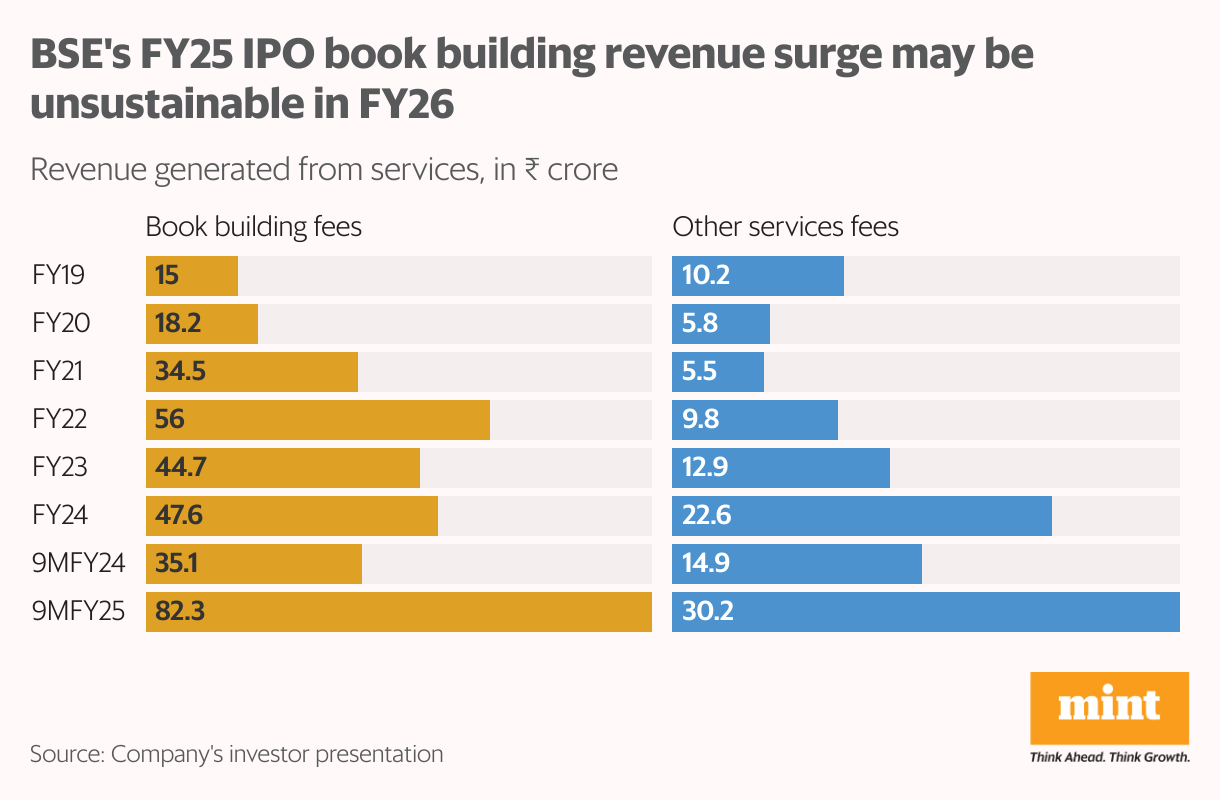

Despite strong derivatives growth, BSE faces short-term hurdles. Weak market sentiment is expected to hurt retail appetite for initial public offerings (IPOs), adding further pressure.

Also read | These two metal stocks may withstand Donald Trump's steel, aluminium tariffs

“Market sentiment is shaken. So, retail appetite for IPOs will also take a hit this (calendar) year. The number of IPOs which have gone through this quarter will be ultimately lower than the last quarter," Manish Bhandari, CEO and portfolio manager at Vallum Capital Advisors said.

As a result, HDFC Securities reduced BSE’s book building and cash market revenue estimates for FY26 in its recent report. The brokerage noted that the exchange’s current valuation fails to justify its near-term earnings growth prospects in the ongoing lacklustre market scenario.

However, most analysts agree that the stock exchange’s strong fundamentals should limit the extent of its downside compared to mid-cap peers.