Chalet Hotels is gearing up for a major expansion. Should investors check in now?

")

Chalet Hotels ended FY25 with 22% revenue growth and strong expansion plans. With over 1,250 rooms in the pipeline, it is set to strengthen its presence and drive sustained earnings growth.

The hospitality sector has been on a strong run. As a result, hotel companies have delivered stellar financial performance in FY25, backed by a steady rise in average room revenue and continued expansion.

In line with this trend, Chalet Hotels ended FY25 with 22% revenue growth, while profit before tax rose 61%. The company delivered across segments.

To capitalize on the sectoral upcycle, Chalet has lined up a strong expansion plan. These expansions will keep adding room to its portfolio for the next three years and will likely keep its earnings trajectory strong.

But what exactly are these expansion plans, and how is Chalet expected to perform in FY26? We break that down in this story.

Second beachfront property in Goa

Chalet is doubling down on its premiumisation strategy, expanding its luxury portfolio through both organic development and acquisitions.

In May 2025, Chalet approved the acquisition of Lakeview Mercantile, a Goa-based luxury resort company, for an enterprise value of ₹140 crore. The company has a 15-acre beachfront plot in Bambolim, Goa, with potential to develop a 170-key luxury resort. This will be Chalet's second luxury beachfront resort in Goa, strengthening its presence in the high-demand tourist hub.

Rishikesh resort offers strong potential

In addition to the Goa property, Chalet completed the acquisition of The Westin Resort & Spa in Rishikesh from Mankind Pharma on 10 February 2025. Chalet acquired this 141-key wellness resort at an enterprise value of ₹530 crores. The property, with operations started in January 2023, resort has an average daily rate of ₹26,500, double that of Chalet’s ( ₹12,094).

However, the property's current occupancy lags at just 43%, significantly lower than Chalet’s average of 73%.

The Westin recorded a revenue of ₹93 crore, up 30% from last year, for the year ending FY25. The property Ebitda also rose 62% to ₹34.5 crore, with margin improving to 37%, up from 29% in FY24. Chalet sees scope for improvement, particularly as occupancy scales. Ebitda stands for earnings before interest, tax, depreciation, and amortization.

The company expects over 60% occupancy, which is reasonably possible with Chalet's expertise in the industry. Axis Securities estimates this property to generate annual revenue of ₹100 crore. Economies of scale will kick in at higher occupancy, further aiding the property margins.

Kotak Institutional Equities estimates Westin to generate an Ebitda of about ₹48 crore, at a 40% margin and 60-65% occupancy.

Marriott expansion lifts key count

Chalet has also continued to add rooms organically. It’s just 1.5 months into the FY26, and it has already commissioned 121 keys at The Marriott, Whitefield, Bengaluru. This pushes the hotel’s operational room count to 512, with eight more keys in the pipeline.

With this addition, Chalet's total operational key (including Westin) rose from 3,193 (in Q4FY25) to 3,314 as of May 2025.

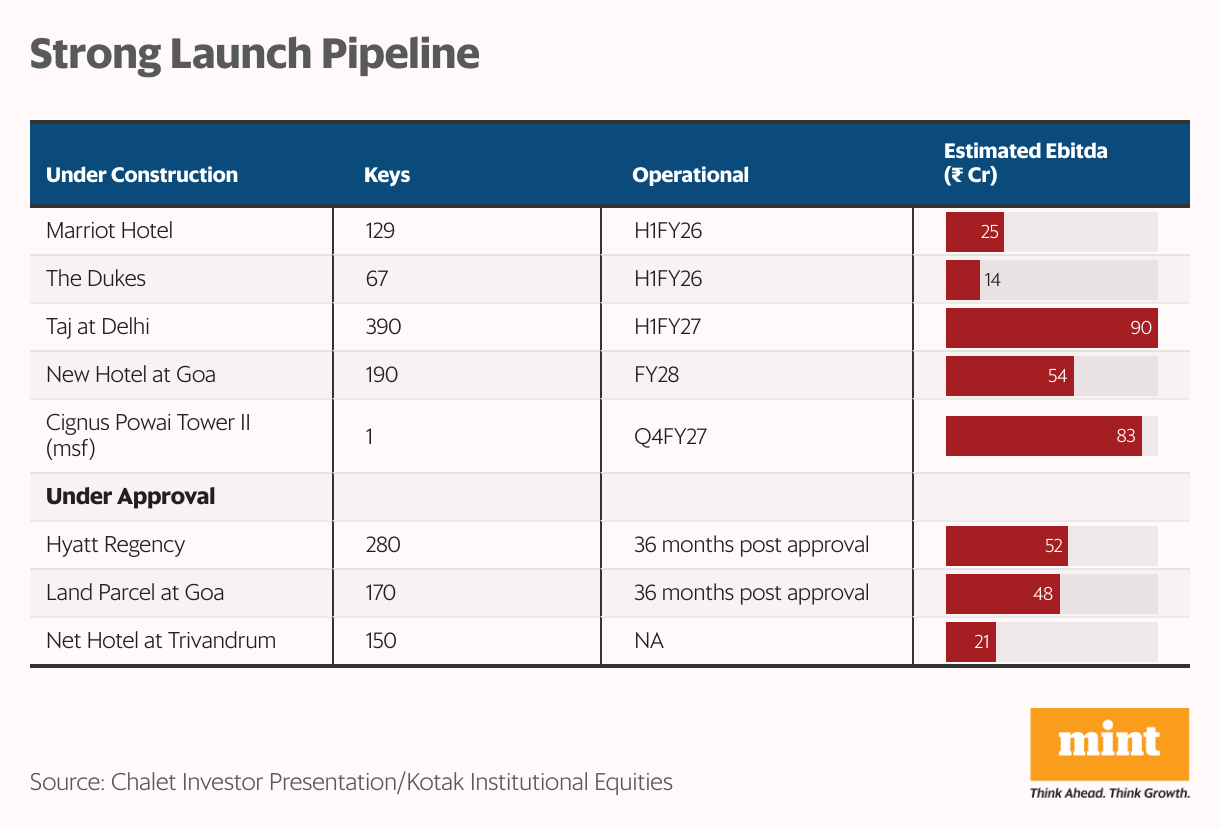

More rooms by FY28

In addition to Marriott, the company has a strong development pipeline. Over the next three years, 640 rooms are under construction, expected to be delivered in phases through FY28. This includes 67 keys at The Dukes Retreat (in Khandala), likely to go live in H1FY26, raising Chalet’s inventory to 3,389 keys. This property will likely start contributing to revenue from FY26.

Next in line is a 390-key property at Taj New Delhi, which is expected to be operational in H1FY27. With this addition, the total room count will touch 3,774 keys by the end of FY27. This will be followed by a 190-room resort at Varca (Goa), expected to be completed in FY28.

Once completed, Chalet's total operational inventory will reach about 3,964 keys by FY28.

Capacity in the approval stage

Besides the under-construction property, Chalet has three more projects in the approval stage, which could add another 600 rooms to its pipeline. These include a 280-key Hyatt Regency (Mumbai), a 170-key Lakeview Resort (Goa), and a 150-key project in Trivandrum. These projects are pending clearance from the National Green Tribunal.

Post approval, they are expected to be completed within 36 months. So far, the total pipeline (under construction + under approval) stands at 1,250 keys, increasing the total inventory by 39% to 4,564 by FY28. In addition, Chalet is also working on a commercial project, with 0.9 million sq. ft. of office space in Powai. This is expected to be completed by Q4FY27.

Kotak Institutional Equities estimates that once operational, the pipeline could add ₹387 crore (about 50%) of incremental Ebitda to Chalet's consolidated ₹772 crore in FY25.

Expansion push may stretch capital

However, this expansion will require significant investment. Chalet has planned a capital expenditure of ₹2,300 crores to fund the expansion over the next three years, primarily financed through internal accruals. Chalet's cash flow from operations increased 38% to ₹950 crores in FY25. The cash and cash equivalents stood at ₹186 crores, up from ₹82 crores in FY24.

As of Q4FY25, Chalet's net debt stood at ₹1,991 crore. Debt increased from ₹1,580 crore (in Q3FY25) due to the acquisition of The Westin Resort. The company's net debt to Ebitda multiple stood at 2.9x (as of FY25), and it expects to maintain it below 3.5x.

Hotel operations see steady climb

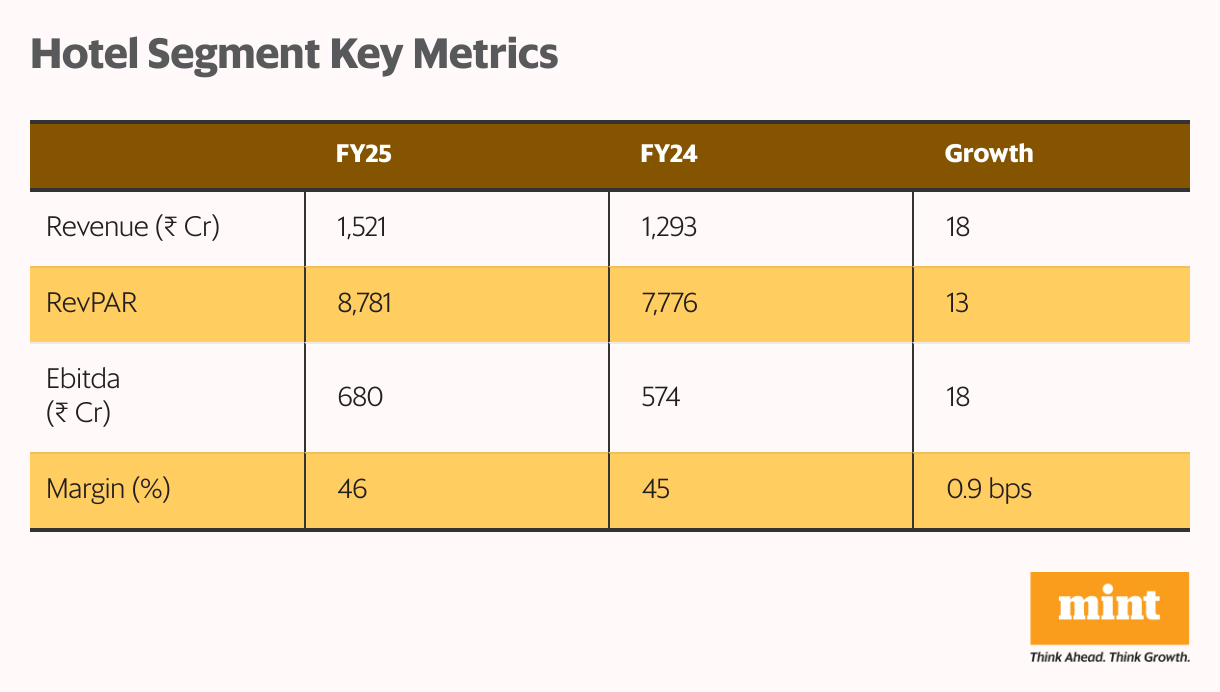

Chalet hospitality segment revenue rose 18% from last year to ₹1,521 crore in FY25. This was driven by a 13% increase in revenue per available room, led by a similar rise in average daily rate. Hotel occupancy remained steady at 73%.

With strong occupancy and revenue growth, the hotel segment Ebitda rose 18% to ₹680 crore, with like-for-like margin improving 90 basis points to 46.1%.

Resorts contributed just 6% of hotel revenue, with the rest coming from business hotels.

With the addition of Westin and Lakeview, the resort share is likely to increase. Higher resort shares are expected to support revenue growth as resorts command daily rates above 23% of hotel rates.

The company continues to diversify geographically beyond its core Mumbai Metropolitan Region (MMR). The region now accounts for 55% of hotel revenue, followed by Hyderabad (21%), Bengaluru (13%), Pune and NCR (5% each). Revenue diversification will continue, with incremental capacity planned in markets beyond MMR.

Leasing income benefits from scale-up

Chalet's annuity (leasing) revenue rose 59% from last year to ₹197 crore in FY25, supported by an 89% increase in leased area. Segment Ebitda increased 56% to ₹154 crores, with a margin of 78.2%.

This segment is expected to benefit from the real estate upcycle. Nine residential towers (10 floors each) are nearing completion, with revenue recognition scheduled to begin in H1FY26. Two new residential towers (11 floors each) and one commercial tower are under construction.

Also Read: 360 One is pivoting from pure-play wealth to full-stack finance. Will it pay off?

Chalet's performance

Chalet’s consolidated (hotel+annuity) revenue increased 22% from last year to an all-time high of ₹1,754 crore in FY25. Margins also expanded by 1.9 percentage points to 44%. However, net profit fell 49% to ₹142.5 crore, impacted by one-time deferred tax asset reversal of ₹202 crore in Q2FY25. Adjusting for this, profit before tax rose 61% to ₹434 crore.

Chalet stock is trading at an EV/Ebitda (enterprise value/earnings before interest, taxes, depreciation, and amortisation) multiple of 29x, in line with its 10-year median. This leaves little room for upside, meaning its share price will likely follow the earnings trajectory.

Industry outlook favourable

According to Horwath, hotel demand is expected to grow at 10% annually over the next 3-4 years, with supply remaining constrained. This imbalance is likely to support a prolonged upcycle for the hotel sector. Events like the World Cup Hockey and Kabaddi Championships may also aid occupancies in the coming quarters.

While Q1FY26 could see some softness due to cancellations and reduced inbound travel amid cross-border tensions, demand is expected to recover from Q2 onwards.

Chalet’s strong room addition pipeline through FY28 should keep the growth momentum intact.

For more such analyses, read Profit Pulse.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.