Power play: Can Coal India defy the headwinds?

")

Coal India is ramping up investments and diversifying into power, even as operational bottlenecks, regulatory risks, and global price drops weigh on margins. With Q4 results around the corner, the spotlight shifts to fundamentals and execution plans

Coal India has been on a roll recently. This week, it made back-to-back announcements—a mining agreement worth ₹7,040 crore with TMC Mineral Resources and a joint venture with Damodar Valley Corporation (DVC) amounting to ₹16,500 crore for its power play.

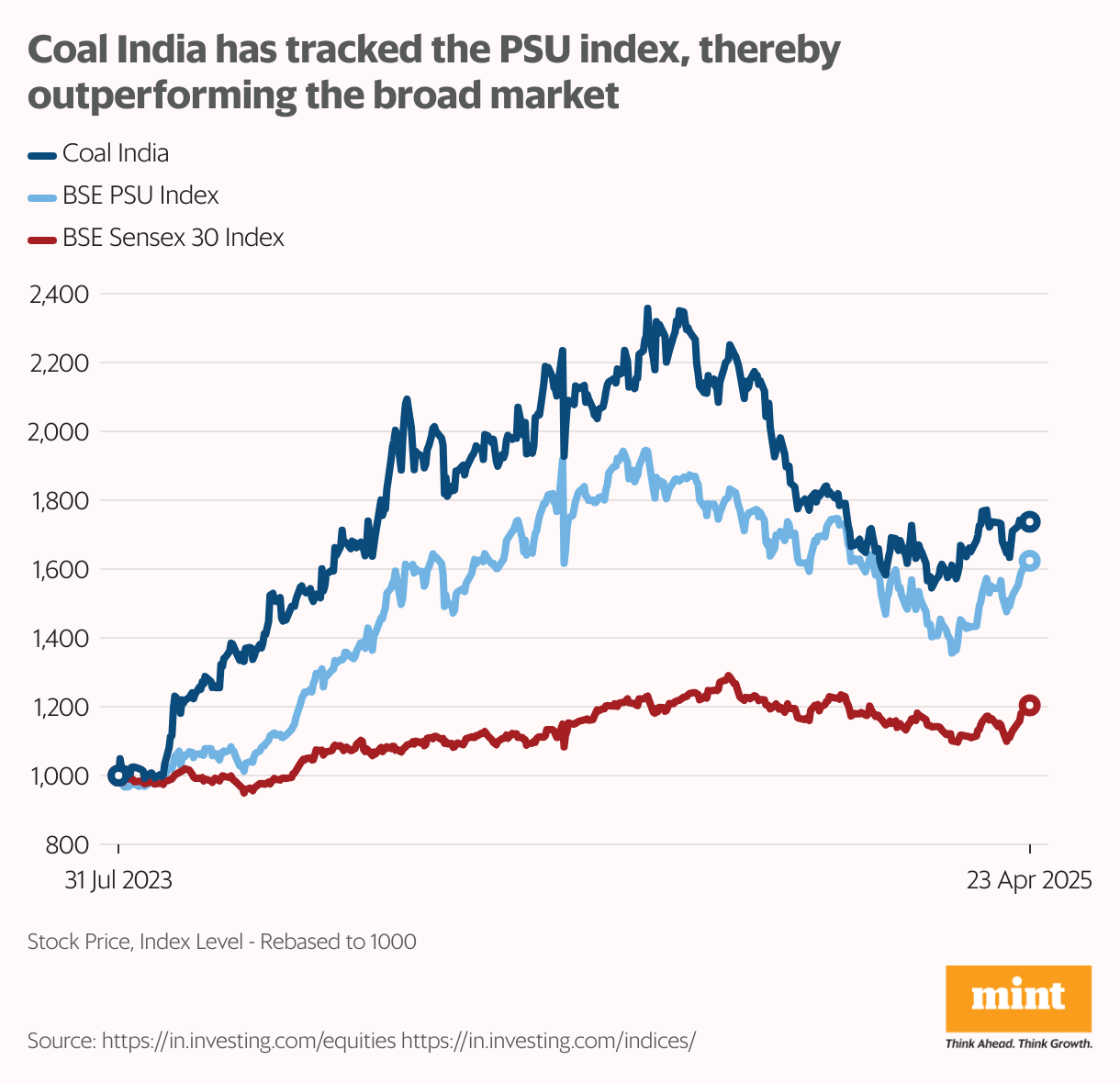

But investors were not enthused. The stock has remained flat as recent headwinds weigh on investor sentiment ahead of the Q4 results. That said, over the last couple of years, Coal India has significantly outperformed the broad market index. It has tracked the general enthusiasm around PSU stocks, and delivered almost 75% return during the period.

Going forward, however, as global drivers take a backseat, company fundamentals are expected to come back into focus. Coal India is a Maharatna central public sector undertaking, which has been India’s leading coal producer since 1972. But recent headwinds have doused investor sentiment. While the near-term outlook is a mixed bag, the medium to long-term promise still holds.

Recent troubles for Coal India

In Q3FY25, Coal India reported 1% year-on-year decline in revenues to ₹35,780 crore while profits saw a much steeper fall of 17.5% during the period. The mining industry faces seasonality, with production taking a dip during monsoons and extreme summers. So, while sequential numbers looked better, they do not reflect the true picture.

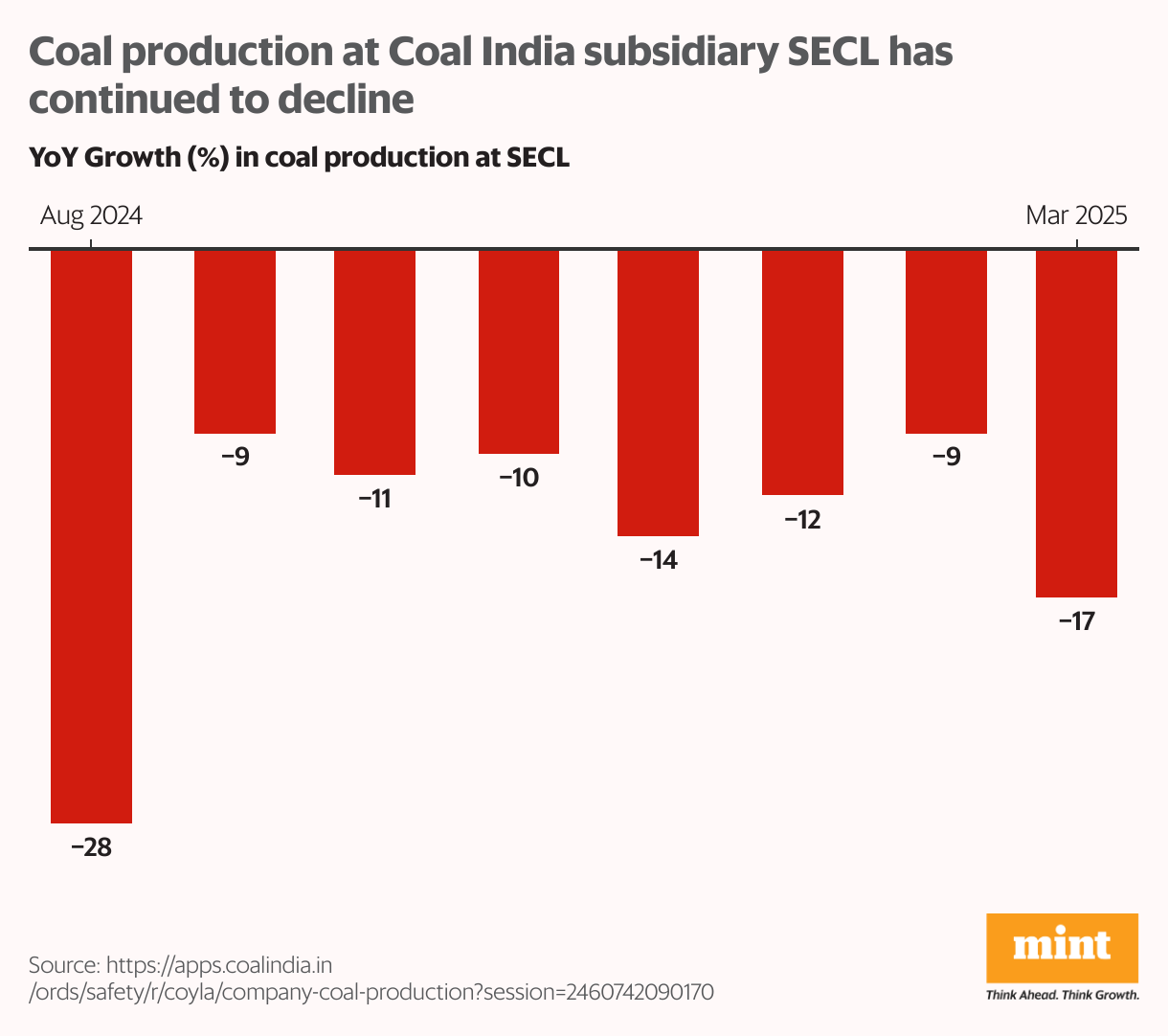

Apart from seasonality, Coal India has also struggled with slower evacuation and high pithead inventory levels. To make matters worse, its subsidiary, SECL has continued to struggle in FY25 as land-acquisition and regulatory clearances were delayed, and projects were deemed unviable.

Coming to margins, given that prices are fixed under FSA (fuel supply agreements), margin expansion at Coal India is contingent on higher e-auction premiums and realizations. This, in turn, depends on global coal prices. While coal had remained stable at about $150 per tonne up till September 2024, geopolitical and economic uncertainty thereafter has led to a sharp correction down to $94 per tonne. This has increased the risk of import substitution, consequently affecting e-auction premiums and margins.

Moreover, import substitution during down-trending global prices also leads to lower offtake volumes. Since costs in mining are primarily fixed, margins are significantly correlated with production volumes. Lower volumes lead to lower operating leverage and compressed margins.

Also Read: Coal India banks on upcoming power plants to accelerate growth

Capitalizing on industry tailwinds

India’s peak electricity demand in 2024 touched 250 GW, and is expected to keep growing with rapid urbanization and climate-change. To meet these rising energy needs, the government has pushed for higher renewable as well as conventional power capacity. Still, as much as 75% of India’s power requirement is fueled by coal, and 80% of that is produced by Coal India.

Estimates pencil in about 80 GW of additional thermal power capacity required by 2030, of which only about 35 GW is currently under construction. The government’s call for higher thermal power production, supported by its consistent commitment towards expanding the railway network, puts Coal India in a beneficial position, given its near monopolistic status in the industry.

Recent troubles should not be extrapolated

While Coal India has faced troubles recently at some of its mines, its diversification across eight states has helped negate localized issues. For instance, continued underperformance of SECL (Chhattisgarh) has been countered to an extent by MCL in Odisha.

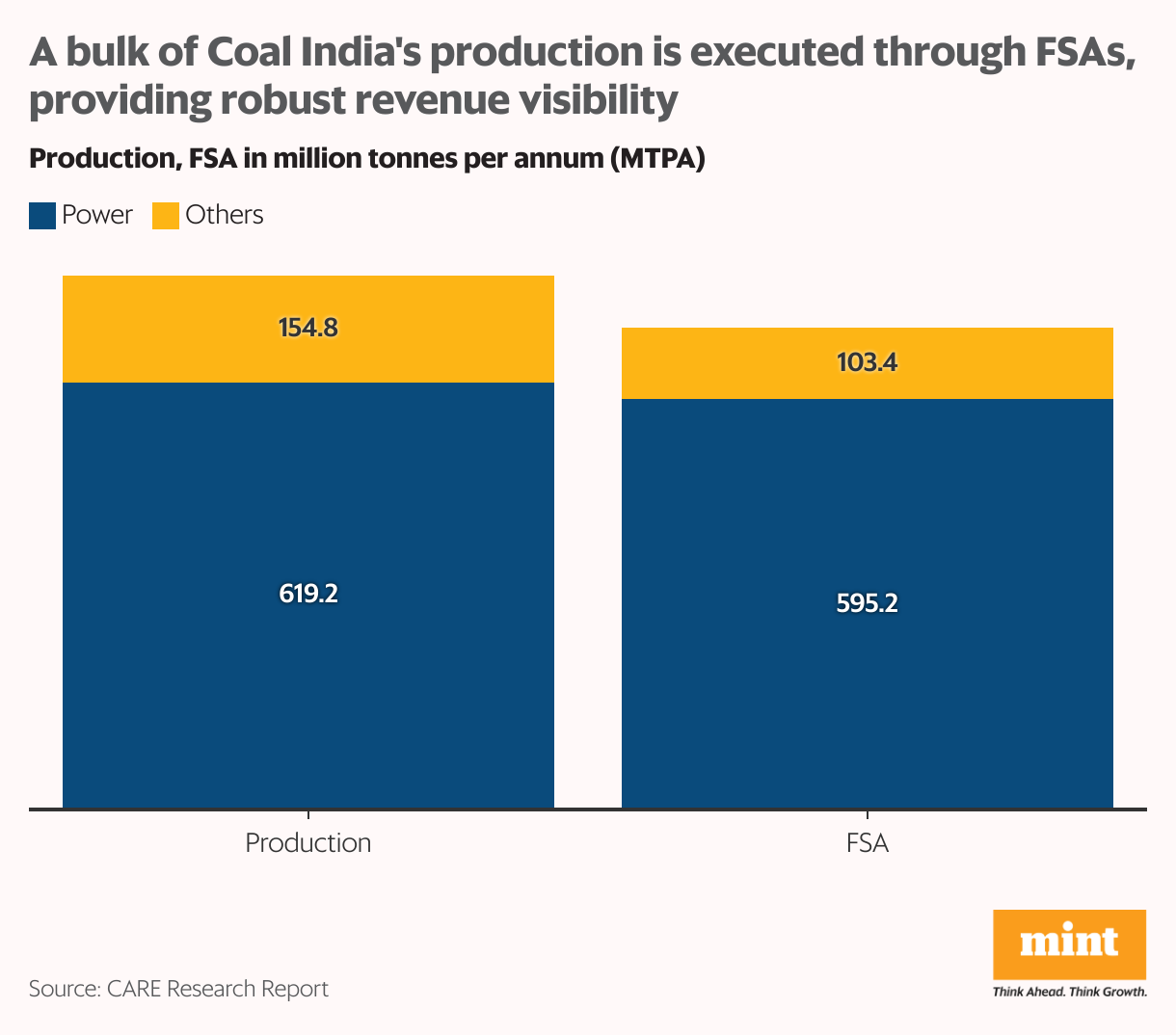

Furthermore, a bulk of Coal India’s sales are executed through FSAs. This ensures robust revenue-visibility. At the same time, growing energy needs of the country are expected to support long-term e-auction premiums and margins.

Additionally, its agreements with clients ensure advance payment, contributing to a strong liquidity position and a healthy cash conversion cycle. Finally, despite the capex-intensive nature of the business, Coal India has managed to maintain a healthy balance sheet with debt-to-equity controlled at less than 0.2x for five consecutive years now. Of course, contingent liabilities worth more than ₹54,000 crore as of March 2024 pose a risk.

Outlook is a mixed bag

The company is expected to announce its earnings for the final quarter of FY25 on 7 May. It is expected to close the year with a dividend yield of 7%, ranking the highest among PSUs in FY25. However, its dividend yield has been trending lower in recent years.

Moreover, performance in Q4 is expected to remain subdued as cheap imported coal continues to affect offtakes and margins. The pace of land acquisition and regulatory clearances has not picked up either, while evacuation infrastructure continues to remain a bottleneck.

Looking ahead into Q1 FY26, extreme summer is impacting production. But early in March, the Indonesian government had announced HBA regulations for coal export prices that replace other benchmarks. Consequent firmer import prices could help support Coal India’s margins.

Innovation and expansion to drive growth

This week, the company announced a mining agreement worth ₹7,040 crore between SECL and TMC Mineral Resources. Under the agreement, TMC will help employ a modern paste-fill technology wherein mined-out voids are backfilled with a chemical paste. The resulting improved surface land stability would prevent land subsidence, be environmentally friendlier, enable higher coal production. and also help save on costs associated with surface-level infrastructure and safety measures.

The company aims for 1 billion tonnes of coal production by FY26. To achieve this, it plans to invest about ₹16,000 crore annually in the expansion of mines, evacuation infrastructure, and coal washeries. Higher washing capacity is expected to reduce ash content, thereby bridging the gap between the quality of domestic and imported coal while also improving combustion efficiency and reducing operating costs.

Power play can hedge risk

The government had opened up coal mining to private players in 2020. Coal India has managed to retain near monopoly so far. But over the longer term, the risk from renewable energy is real. Against this context, the company’s forward integration towards power production makes perfect strategic sense.

Early in 2024, Coal India received regulatory approvals for setting up power plants. It started with two power plants with capacities of 660 MW and 1600 MW in Madhya Pradesh and Odisha. This week, the company announced a JV with DVC for brownfield expansion of its Jharkhand power plant. The 50:50 venture will entail an investment of ₹16,500 crore to add 1600 MW capacity. While the power plants will benefit from proximity to the company’s own coalfields, it will be several years before the projects can commence operations and reach financial fruition.

The company has also been considering renewable energy, coal bed methane, and coal gasification projects.

Risks remain

The business is faced with risks arising from renewable energy, bottlenecks in evacuation infrastructure, potential materialization of contingent liabilities, and falling prices of global coal. It also faced regulatory overhang from the Supreme Court’s judgement in August 2024, that allowed states to retrospectively levy or renew tax demand on mineral rights and mineral-bearing lands.

While the company has been investing towards expansion and diversification for managing some of these risks, the pace of execution and debt on its books will remain key monitorables.

For more such analyses, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.