Markets

Markets

Seven consistent midcap stocks that foreign institutional investors bought in Q1

Summary

- FII buying and selling can provide a gold mine of information, but comes with some caveats. Following their transactions can be instructive, but it’s important to make informed decisions that suit your goals and risk appetite.

Foreign investors or FIIs are financial titans known for their sophisticated and flexible investment strategies aimed at achieving sky-high returns. Several factors shape their strategies, including market conditions, company fundamentals, sectoral trends, risk management and investor sentiment.

While their dynamic strategies and potential for high returns are enticing for individual investors like you and me, understanding their methodologies and time horizon is crucial. And no matter how bullish or bearish they turn, it’s important to understand your own risk appetite and conduct your own research.

FIIs have rekindled their appetite for Indian equities in recent months, with net purchases surging to a four-month high in July.

Today we look at the top mid cap stocks that foreign investors recently added to their portfolios. These companies have also shown consistent improvement in their fundamentals.

#1 Cello World

A recently listed stock that had its IPO in October 2023, Cello World has garnered significant interest from the big boys of the equities market – domestic institutional investors (mutual funds, etc) and FIIs.

The company’s latest shareholding pattern shows that FIIs increased their total stake to 5.9% in the June quarter, from 4.4% in March and 3% in December 2023. Mutual funds also increased their holding to 2.3% in June from 2.2% in March.

Here’s how the shareholding pattern has changed over the past three quarters.

Cello World offers a diverse range of products in several categories, allowing it to serve as a one-stop-shop for consumers across income levels. It has the most diversified product portfolio among its peers, with products in glassware, opal ware, melamine, and porcelain. This has allowed Cello to maintain stable revenue growth over the years.

The company recently initiated a share sale to institutional investors through a qualified institutional placement (QIP) to raise ₹740 crore ($88 million). The issuance of additional shares for the QIP resulted in an equity dilution of 4.1%.

In Q1FY25, Cello World reported 6.1% year-on-year growth in revenue to ₹510 crore. Net profit grew to ₹83 crore, with margins improving to 16.5%.

Management indicated that urban demand was weak during the quarter, owing to the general elections and heat waves. It is optimistic that demand will recover in the second half of the year and expects high double-digit growth for the full financial year.

Cello World’s stock is up 11% so far this year.

#2 Kirloskar Brothers

Part of the Kirloskar Group, Kirloskar Brothers is making strong inroads in the investor community. FIIs have added the stock to their portfolios for more than eight consecutive quarters, increasing their stake from 1.5% in September 2022 to 5.03% in June 2024.

Even domestic mutual funds have turned bullish on the company, and fund managers have added the stock to their portfolios for the past four quarters.

Here’s how the shareholding has changed over the past eight quarters.

Kirloskar Brothers is an engineering company that manufactures systems for fluid management. Its primary operations cover large infrastructure projects such as water supply, power plants and irrigation, as well as the production of pumps, valves, motors, and hydro turbines.

With over 250 product categories and more than 100,000 stock-keeping units (SKUs), the company serves more than 12 industries and has over 2,500 customers.

Sales grew at a compound annual growth rate of 4% between FY20 and FY24, while the bottom line grew at a CAGR of 155%.

The company's revenue grew by 7.3% yoy in FY24 owing to sustained demand for customised products and an increase in standard product orders. Net profit surged by 48.3% yoy during the same period, primarily due to reduced interest expenses and increased other income for the year.

Management expects double-digit revenue growth in FY25. The consolidated pending order book for the international business stands at more than ₹3,000 crore.

The company aims for continuous innovation, with more than 100 product launches a year. It is also developing new products for green hydrogen and small modular reactors.

Management outlook on the international business is positive, owing to increased inquiries. The company is also making strategic investments in digital ventures to enhance its revenue streams.

It also plans to capitalise on its localised global presence by introducing new products in the US and UK while looking to increase revenue contribution from the service segment for its UK entity.

It’s no wonder then that shares of the company have rallied more than 90% so far this year.

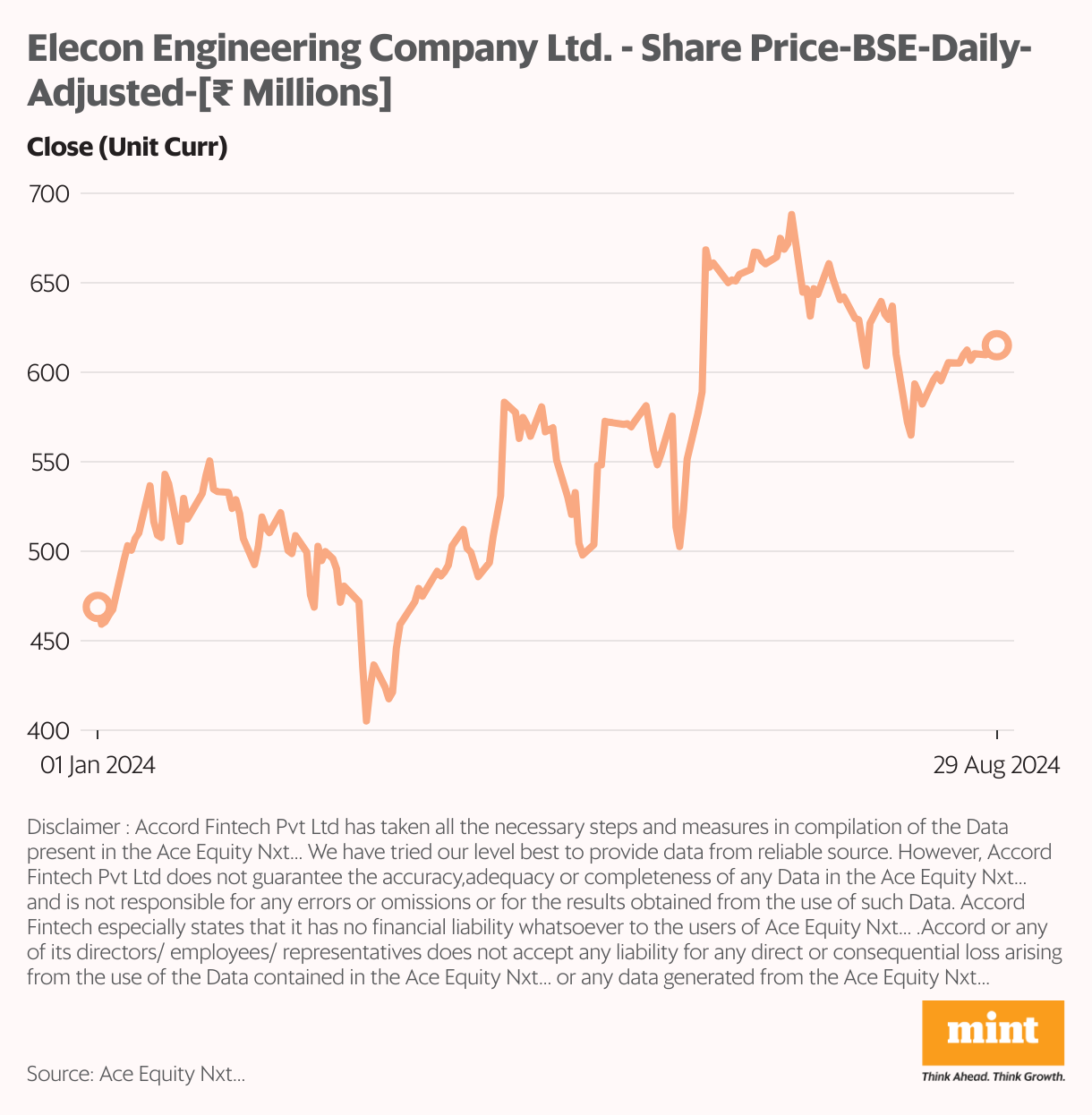

#3 Elecon Engineering

FIIs increased their holding in Elecon Engineering from 7.6% in March to 9.1% in June. They have been consistently buying shares of Elecon for the past six quarters. Even mutual funds increased their stake to 1.9% in June from 1.3% in March.

Here’s how the shareholding pattern has changed over the past eight quarters.

The company makes and sells power transmission and material handling equipment in India and abroad. It is also in the steel and non-ferrous foundry business.

It was one of the first to introduce mechanised bulk material handling equipment in India. Since then it has become the single largest company offering most types of bulk material handling equipment and products.

Elecon derives 13% of its revenue from the material handling equipment solutions. The remaining 87% is from power transmission services. The company is a market leader with 39% market share of the organised sector in India.

In FY24, Elecon reported 26.7% yoy revenue growth and 44.5% Ebitda growth.The stock has been in the limelight since a month ago, when its board approved a stock split in the ratio of 1:2.

Management aims to expand in overseas markets by strengthening relationships with current OEM partners and forging new alliances. However, the company has offered conservative growth guidance for FY25 due to geopolitical tensions.

Shares of Elecon Engineering have rallied 32% so far this year.

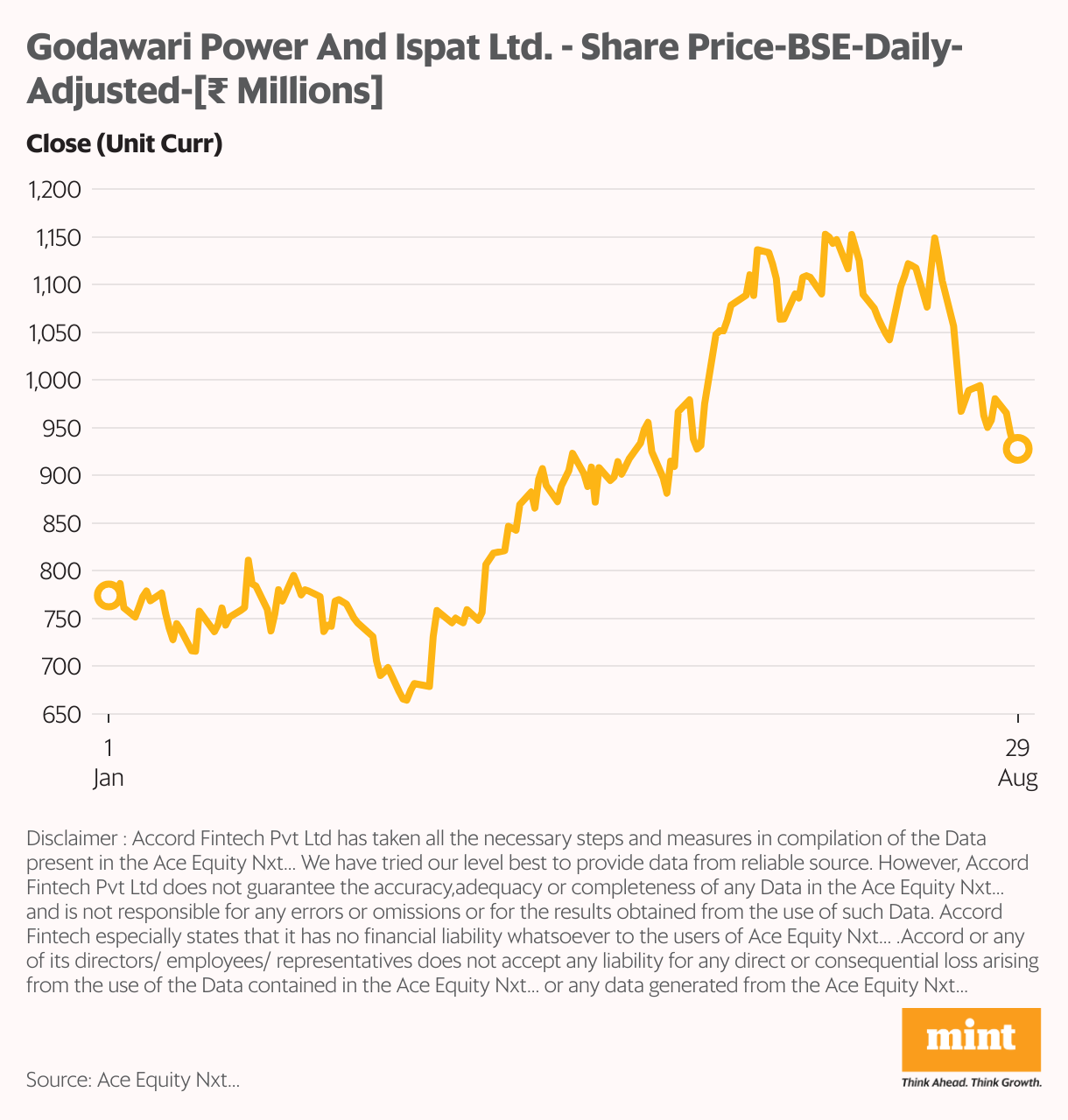

#4 Godawari Power

The latest shareholding pattern of the steel company shows that FIIs increased their stake from 5.5% in March to 7.5% in June. They held a mere 2% of the company in September 2022.

Indian mutual funds are also bullish on Godawari Power, having bought the stock for the past four quarters.

Here’s how the total shareholding has changed over the past eight quarters.

Part of the Hira Group of Industries in Raipur, Godawari Power was formerly known as Ispat Godawari Ltd.

It has a unique presence across the steel value chain. It manufactures all kinds of intermediate steel products such as sponge iron, ferroalloys, HB wires and finished long steel products including billets, wire rods and mild steel wires. It is also in the power business and generates electricity for captive use.

In the first quarter of FY25, Godawari Power reported 12% yoy revenue growth, driven by higher production volumes and realisation of pellets. Net profit increased by 24% yoy to ₹290 crore over the same period.

The company has undertaken large capital expenditure (capex) and has big growth plans for the next few years. It plans to nearly double iron ore mining and pellet capacity and establish an integrated steel plant with four times its existing capacity. The company also aims to supply galvanised products to agencies such as Indian Railways.

So far this year, shares of Godawari Power are up 24%.

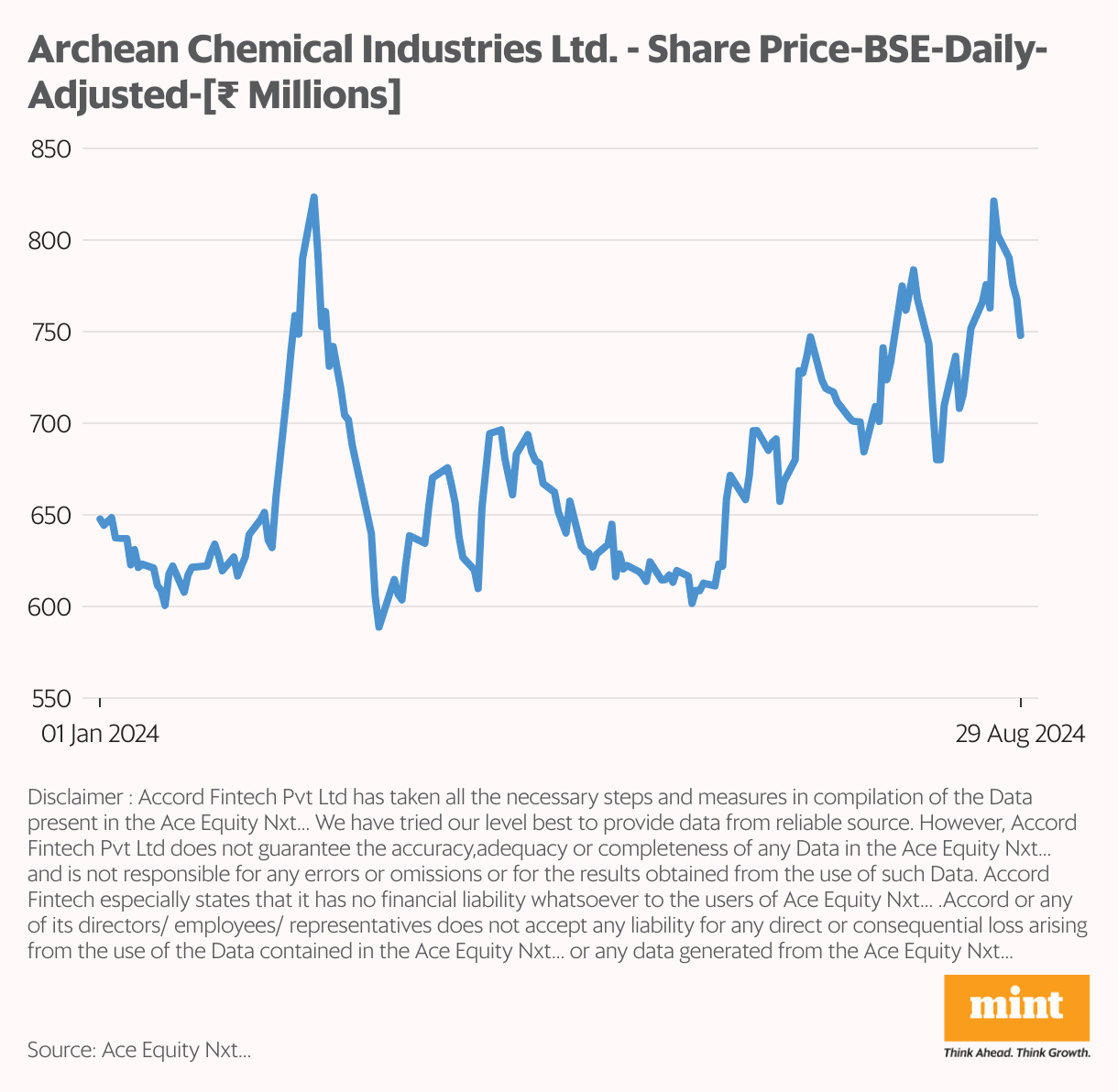

#5 Archean Chemicals

Previously overlooked by FIIs, Archean Chemicals saw heavy buying from them in the June quarter. Their stake rose to 9.5% from 5.9% in the previous quarter. Even mutual funds have turned bullish on the company.

Archean Chemical is one of the largest exporters of bromine and industrial salts. It’s the leading specialty marine chemical manufacturer in India, producing and exporting bromine, industrial salt, and sulphate of potash to customers around the world. It raised ₹1,430 crore in its IPO in November 2022.

Its unique location advantage and high barriers to entry have supported its growth over the years. A steep increase in bromine prices and the company’s favourable product mix has also improved operational performance.

The company’s revenue slumped almost 35% yoy to ₹2.2 bn in the June quarter amid logistics challenges. Net profit was also hampered and came in at ₹48.5 crore.

Management is cautiously optimistic about the second half of FY25 and anticipates improvements in performance as the agricultural sector recovers.

To diversify its operations, it plans to broaden its product portfolio in the hydrocarbon space.

Shares of the company have gained 17% so far this year.

#6 Shriram Pistons & Rings

For years, FIIs owned no shares of the company. But that has changed in the past five quarters. In June, FIIs increased their holding to 2% from 1.35% in March.

Here’s how the shareholding pattern has changed over the past eight quarters.

Shriram Pistons & Rings is primarily engaged in the end-to-end development and manufacturing of pistons, piston pins, piston rings and engine valves for various automotive companies in the domestic and export markets.

Its products are marketed to renowned OEMs and through aftermarket brands such as SPR and USHA, catering to domestic and international markets. It has a wholly owned subsidiary, SPR Engenious, which has stakes in other entities.

The auto industry is undergoing big shifts with the rise of electric and hybrid vehicles. Shriram Pistons has been strategically diversifying to cater to the potential demand from this.

All of this has helped the company post above-average numbers. Its revenue CAGR from FY19 to FY24 stands at 9.4%, Ebidta CAGR at 16.9% and net profit CAGR at 25.9%.

With strong prospects for subsidiaries and additional capacities kicking in, the company is expected to fare well in the coming quarters.

So far this year, shares of the company are up around 53%.

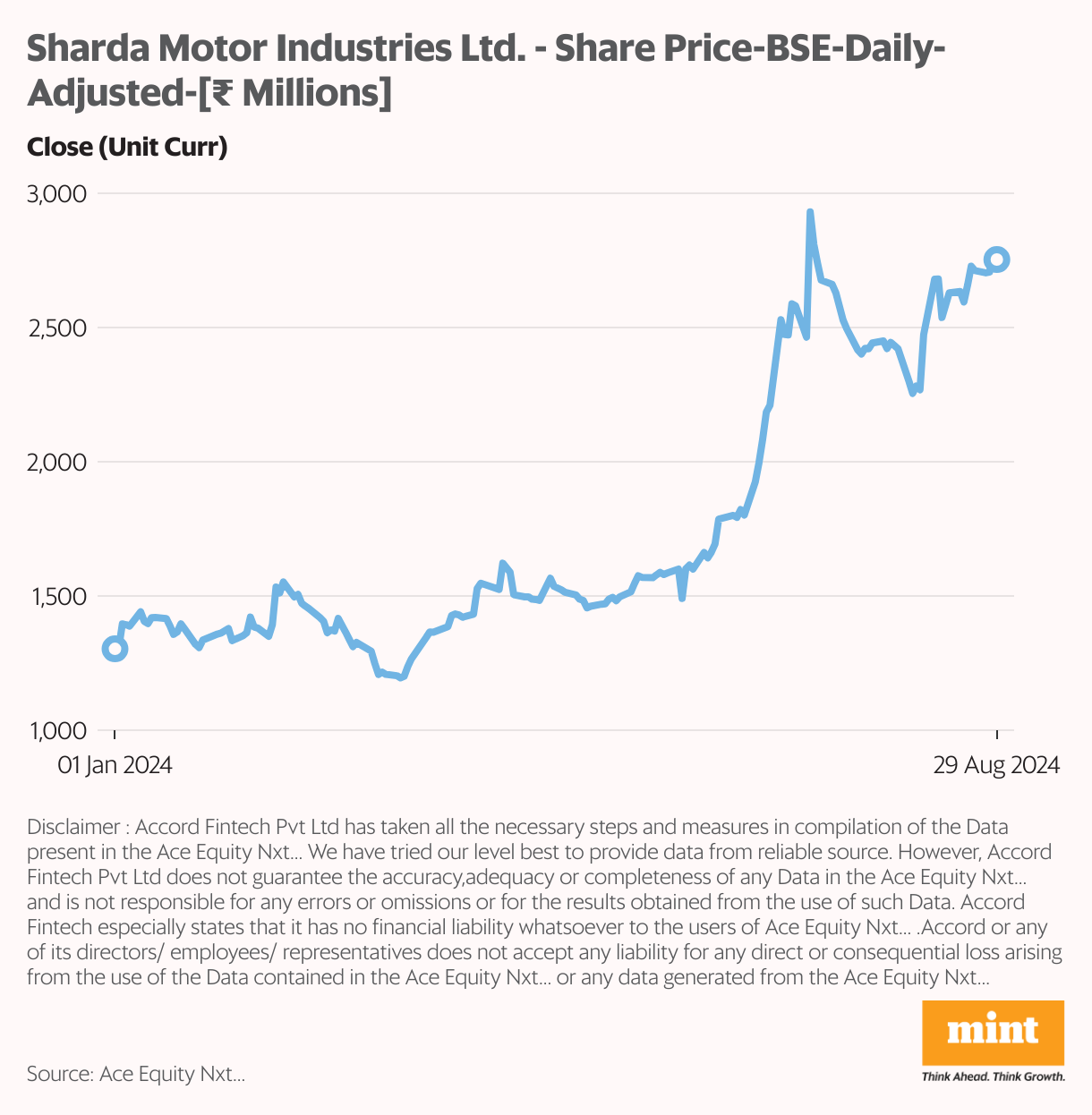

#7 Sharda Motor

After a hiatus in the March quarter, FIIs were back to buying the stock in the June quarter, increasing their stake from 1.5% to 2.4%. Before January-March, FIIs had increased their stake for six consecutive quarters.

But the biggest buys came from Indian mutual funds. Their holding went up from almost zero in March to 7.9% in June.

Here’s showing the shareholding pattern has changed over the past eight quarters.

Sharda Motor primarily manufactures and assembles components for automobiles and white goods.

Its portfolio includes catalytic converters, exhaust systems, suspension systems, sheet metal components and plastic parts for the automotive and white-goods industries. It has a market share of 30% in exhaust systems and 10% in suspension systems.

Its large market share has driven the company's volumes over the years, which is why its revenue has grown at a CAGR of 15.3% over the past five years. Net profit has grown at a CAGR of 15.7% on the back of low costs due to backward integration.

Sharda Motor, having been debt-free over the years, has had sufficient cash flows to fund its capex. In May the company announced it would buy back 102.7 million equity shares for ₹1,800 each.

Since the government announced new emission norms for off-road vehicles, demand for the company's products has increased, giving it an opportunity to grow its market share.

Sharda Motor is now focussed on multiple verticals to drive growth. These include:

- Lower-cost battery prototypes for EVs

- Niche product development of canopies for specific models

- Another opportunity in the three- to four-litre engine segment

- Export focus on Western Europe for opportunities in off-highway segments

Sharda Motor’s stock has rallied 111% so far this year.

Conclusion

FII buying and selling can provide a gold mine of information, but comes with some caveats.

Following their transactions can be instructive, but your investment journey is personal. So it’s important to make informed decisions that suit your goals and risk appetite.

While most of us don’t have the vast resources of foreign investors, we do possess the ability to invest with patience and a long-term vision.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com