Hindustan Aeronautics: Here’s all you need to know before investing

Here’s everything you need to know before investing in shares of India’s premier defence stock.

Few companies in India have garnered as significant an impact in the aerospace and defence sectors as Hindustan Aeronautics Ltd (HAL). The state-owned giant has been instrumental in shaping the future of India's aerospace and defence capabilities.

With decades of expertise, HAL has grown beyond being a mere supplier of military aircraft to becoming a strategic enabler of national defence, advancing the country’s aspirations of self-reliance under initiatives like Make in India.

From manufacturing state-of-the-art aircraft to developing cutting-edge drones, HAL’s journey is a testament to its resilience, innovation, and vision for the future.

The company’s financial trajectory, bolstered by a substantial order book and strong government backing, signals strong growth prospects, making it a worthy stock to watch.

Here’s everything you need to know before investing in HAL.

About the company

Hindustan Aeronautics (HAL) is one of the largest and most renowned aircraft manufacturing companies in India.

With a history spanning over seven decades, HAL has been instrumental in the design, development, and production of various aircraft, helicopters, and aero engines. The company's notable achievements include the production of indigenous aircraft like the Tejas Light Combat Aircraft (LCA) and the Advanced Light Helicopter (ALH).

HAL's expertise extends to aircraft upgrades, overhaul services, and the manufacture of aero structures, avionics, and other critical components.

It has 20 production and overhaul divisions and 9 R&D centres across India. The company inaugurated a new design and test facility at Aero Engine Research & Development Centre in Bangalore in December 2023, to accelerate R&D of aeroengines.

HAL has historically been one of the PSUs with largest allocation to R&D costs. The company spends around 8% of the total revenue on R&D. Also, it has created an R&D reserve. An annual contribution of 15% of the operating profit, is transferred into this reserve.

HAL’s Giant Leap

The company’s role in India's defence sector is evolving, thanks to strategic initiatives like the Make in India program.

This initiative has allowed HAL to step up its innovation game, resulting in enhanced revenue visibility and an increased appetite for taking on capital-intensive projects.

HAL’s massive order book continues to expand, with major inflows expected in the near future.

The company’s aggressive push into export markets has also contributed to its growth. With platforms like the LCA Tejas gaining international recognition, HAL is steadily enhancing its export portfolio, positioning itself as a key player on the global defence stage.

Notably, HAL has been awarded the largest proposal approval in its history—a project worth ₹70,500 crore for the construction of 60 marine utility helicopters, with an estimated cost of ₹32,000 crore.

What makes HAL particularly interesting for investors is its exposure to the growing drone market. The company is at the forefront of developing AI-driven, advanced drones for high-altitude strategic missions.

Its emphasis on reducing foreign dependency for such technology aligns with the government's self-reliance goals.

Order Book Strength

HAL’s order book is a key pillar of its growth story. The company’s net profit has grown at a CAGR of 26% in the last three years supported by its healthy growth of order book and timely execution.

At the end of FY25, its order book stood at a little over ₹1.2 trillion. This is up from ₹94,000 crore as of FY24 and ₹82,000 crore in FY22.

In recent times, HAL has received substantial contracts for repair and overhaul services. A landmark contract awarded to HAL by the ministry of defence was in September 2024, for the supply of 240 aero-engines for the Su-30 MKI aircraft, worth ₹26,000 crore.

This growing order book provides HAL with visibility for future revenue streams, making it a solid investment proposition.

Moreover, HAL is expected to secure additional major contracts over the next few years, with the total order inflows expected to range between ₹1.6 trillion to ₹1.7 trillion over the next 18 months to three years.

The management expects full workload until 2032 and expects to maintain double-digit growth in sales. It has also planned ₹14,500 crore capex over five years for capacity expansion and modernisation.

HAL is poised for significant order inflows, with ₹1.3 trillion worth of contracts for 97 LCA Tejas Mark 1A and 156 LCH Prachand at an advanced stage of clearance, expected to materialise within the next three to six months.

Nevertheless, investors should note that the company has received some criticism due to the delay in delivery of the fighter jets.

The typical execution period for the order book extends to a few years, which could further stretch due to time taken to build capabilities. As such, the risk of overruns cannot be ruled out, impacting margins.

Financial Performance

HAL’s financial performance has been robust. Its sales have been growing smoothly. During 2020-24, the sales and net profit have grown at a CAGR of 9.6% and 26%, respectively.

The returns have been admirable, reporting an average RoCE and RoE of 30% and 26%, respectively.

Due to its large scale and healthy operating profitability, the company’s debt coverage metrics remain strong. As a result, its liquidity position is strong, as evidenced by its cash balance of ₹26,400 crore.

Given the volatile geopolitical scenario, defence companies like HAL will remain instrumental in India's manufacturing ecosystem and will play a crucial role in helping India become part of global defence supply chain.

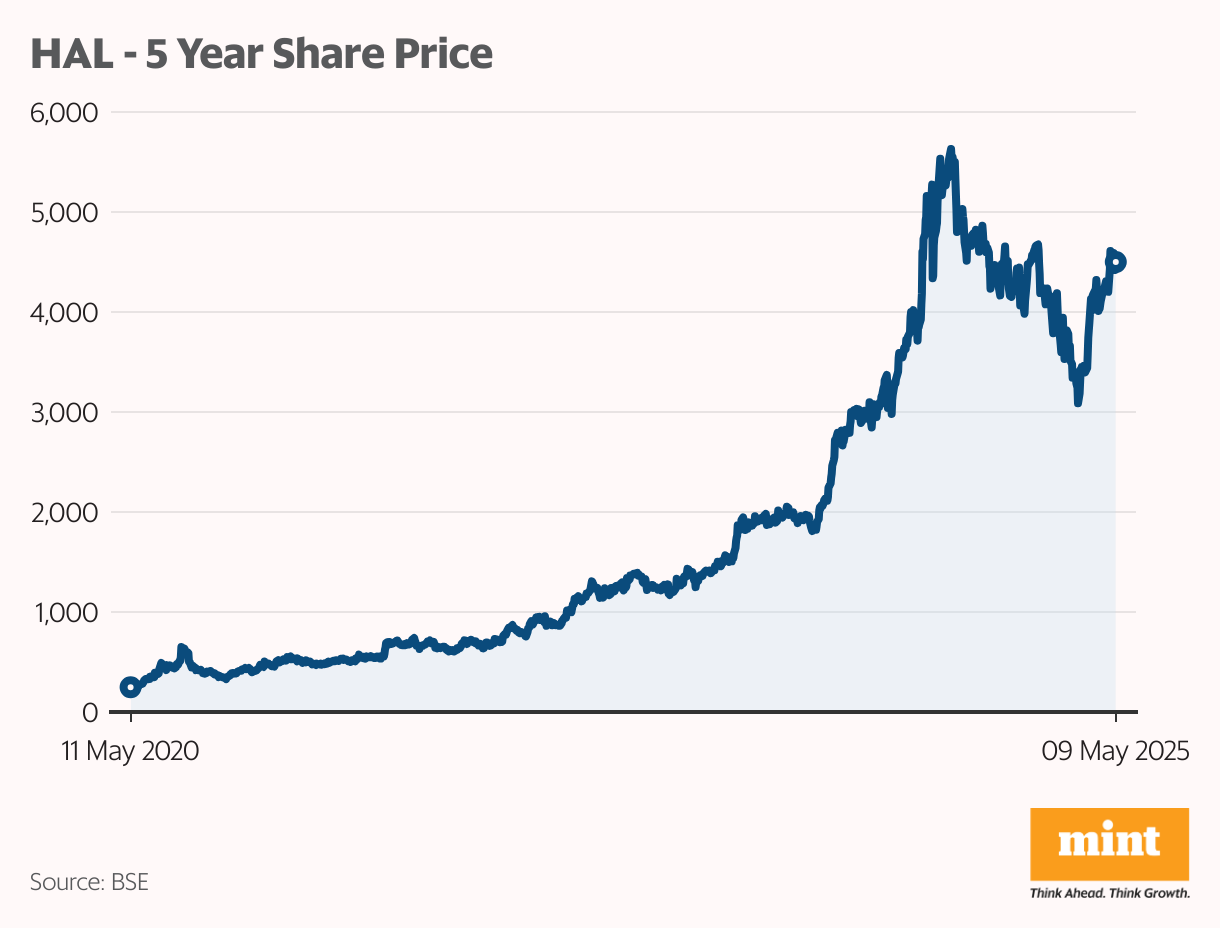

Stock Performance Over 5 Years

HAL has seen its stock price surge significantly in recent years, delivering impressive returns to investors. Over the past one year, HAL’s stock has moved up 16% while in the past 5 years it has surged 1,700%, fuelled by increasing investor confidence in the company’s growth prospects.

What next?

The future of HAL is intrinsically tied to India’s defence spending, which continues to grow as the government focuses on modernizing the armed forces and strengthening self-reliance in defence technology.

HAL is well-positioned to capture a significant share of this increasing budget, particularly as the country looks to reduce reliance on foreign defence suppliers.

HAL’s drone initiatives are a key area of growth. The company is developing the CATS Warrior, an AI-driven unmanned combat aerial vehicle (UCAV) that will work alongside manned fighter jets.

It’s also developing the CATS Hunter, a companion system for unmanned and manned aircraft. The company has set its sights on the launch of the CATS Warrior II, an advanced drone with 10+ hours of endurance and a payload of 400–500 kg, set for production by 2027.

In addition to drones, HAL’s focus on advanced avionics, AI-driven systems, and the production of strategic aircraft and helicopters further strengthens its growth potential.

With an expected capex investment of ₹3,000 crore per year until FY30, HAL’s roadmap for the coming years is clear—continued growth, innovation, and deeper integration with India’s defence ecosystem.

Conclusion

HAL’s story is one of steady evolution, transforming from a traditional defence manufacturer into a modern aerospace and defence giant.

As the company continues to innovate and execute, it could remain an attractive option for long-term investors looking to capitalize on India’s defence and aerospace growth.

However, HAL could face some surprise challenges along the way. Dealing with the government, its primary client, can be arduous due to high receivable days and orders that are heavily reliant on defence budget allocations.

Investors should evaluate the company's fundamentals, corporate governance, and valuations of the stock as key factors when conducting due diligence before making investment decisions.

Happy Investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com