Behind ICICI Lombard's recent surge: What the headlines won’t tell you

")

Recent developments in the insurance sector have sparked investor interest, particularly with the potential hike in third-party motor insurance premiums. ICICI Lombard, a key player in this market, has shown impressive performance despite recent challenges. Will this trend continue?

General insurance has caught investors’ attention over the last few days. Reports indicate that the ministry of road transport and highways is considering an 18-25% hike in third-party motor insurance premiums.

On cue, ICICI Lombard General Insurance, which claims 10.8% share of India’s motor insurance market, surged 7% in a single day on Friday.

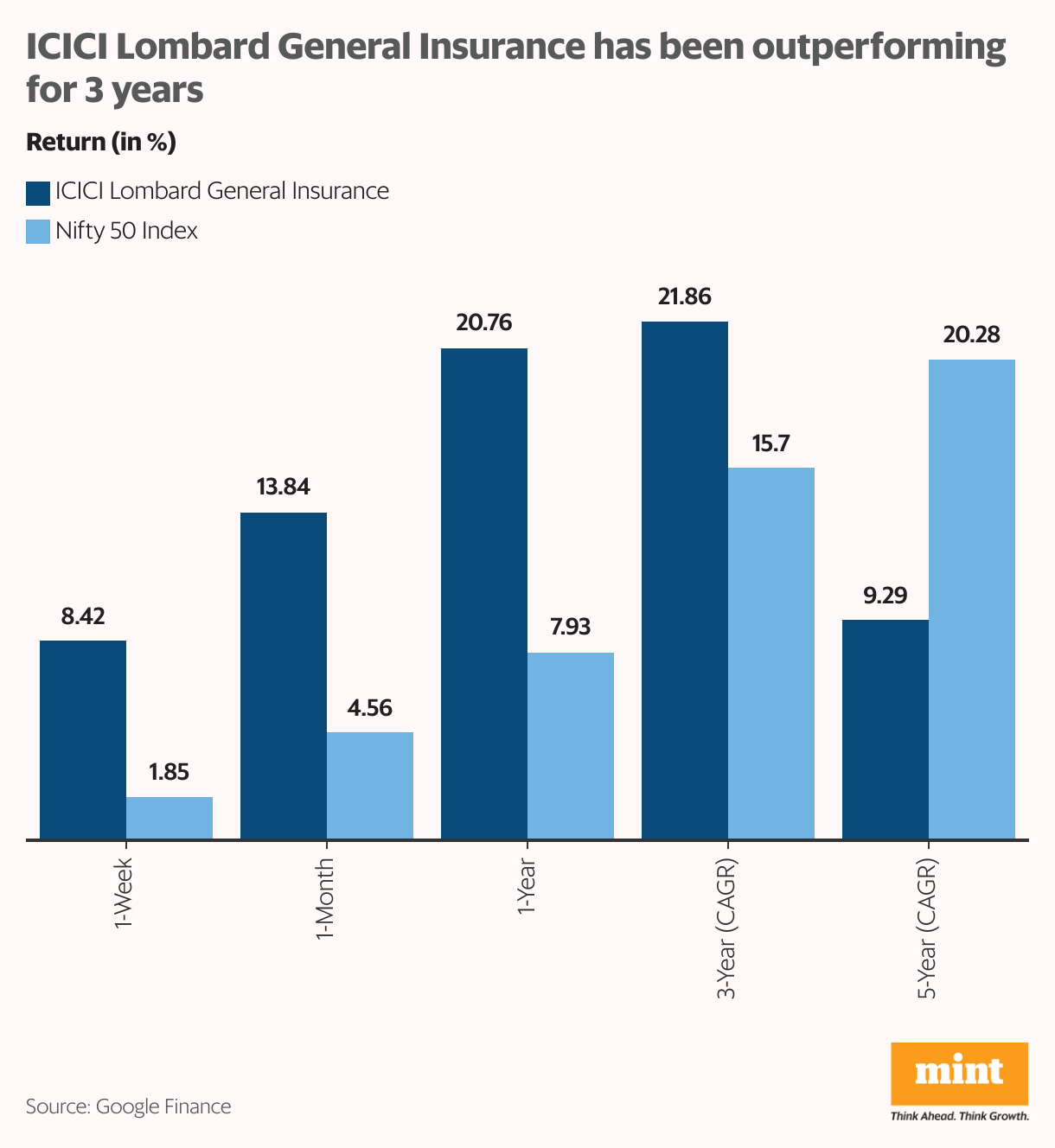

Investor enthusiasm around the stock is not new. The stock has been outperforming over the last three years.

While disappointing Q4 earnings had dampened sentiment in recent months, the latest development has breathed fresh life into the counter. Can this take the stock to new heights?

Motor insurance is the mainstay

For general insurers, automotive insurance constitutes a major chunk, around 30% of the business. About 60% of that is for insuring damages to third parties. Third-party insurance is compulsory according to the Motor Vehicles Act.

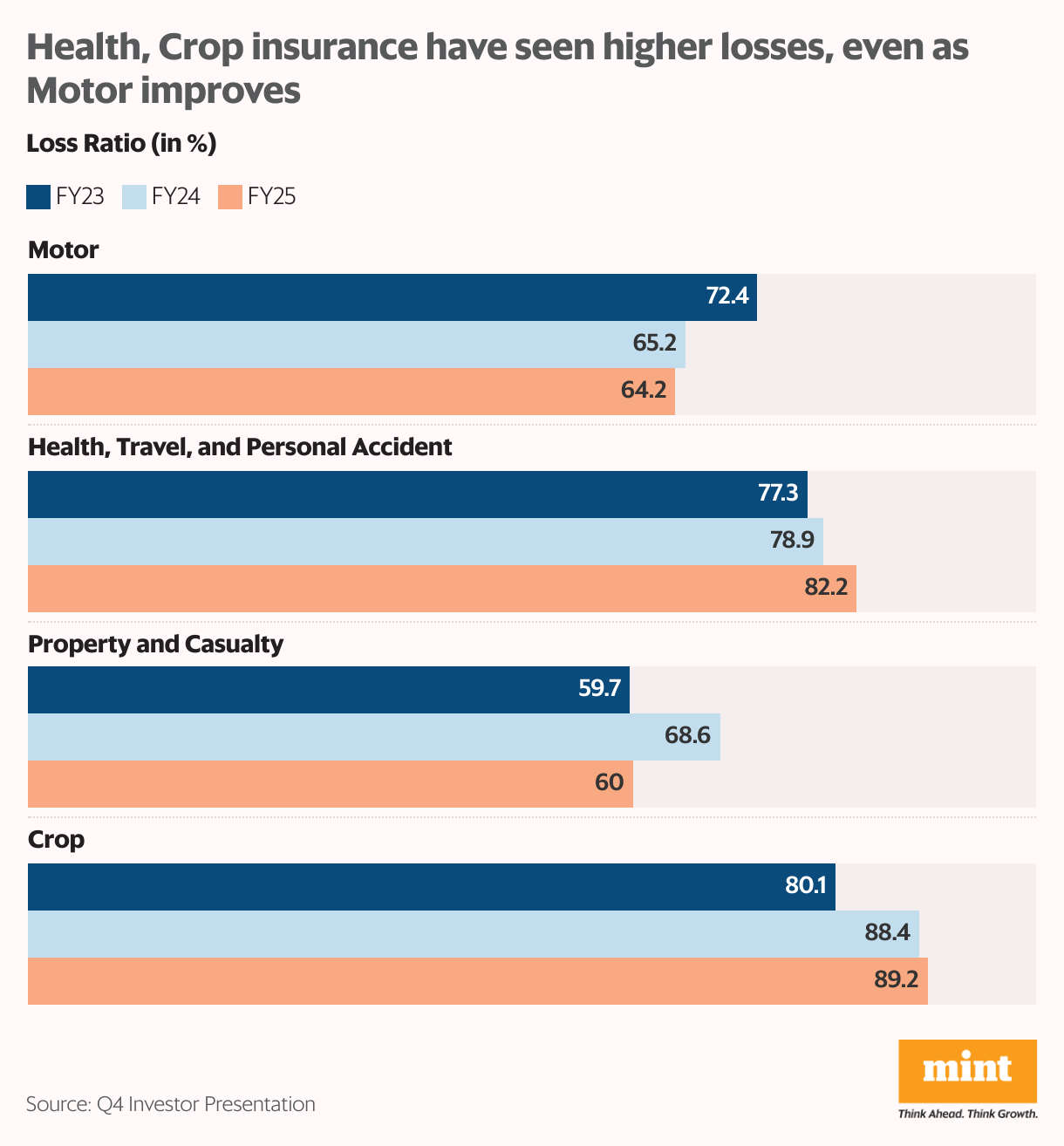

The regulator has held premiums steady in the segment for the last four years. But with more vehicles on the road, claims and loss ratios have been on the rise. In the first half of FY25, the loss ratio for motor insurance stood at 124.8%, while that for the broader general insurance sector was much lower, at 113.2%. So, higher premiums promise to bring some much-needed relief to insurers.

ICICI Lombard is a well-diversified multi-line insurer. But motor insurance constitutes 40% of its business, which is split equally between own damage and third-party damage. Health, travel, and personal accident insurance comprise the next largest segment at 29%, picking up pace over the last few years.

Industry slowdown weighed on business

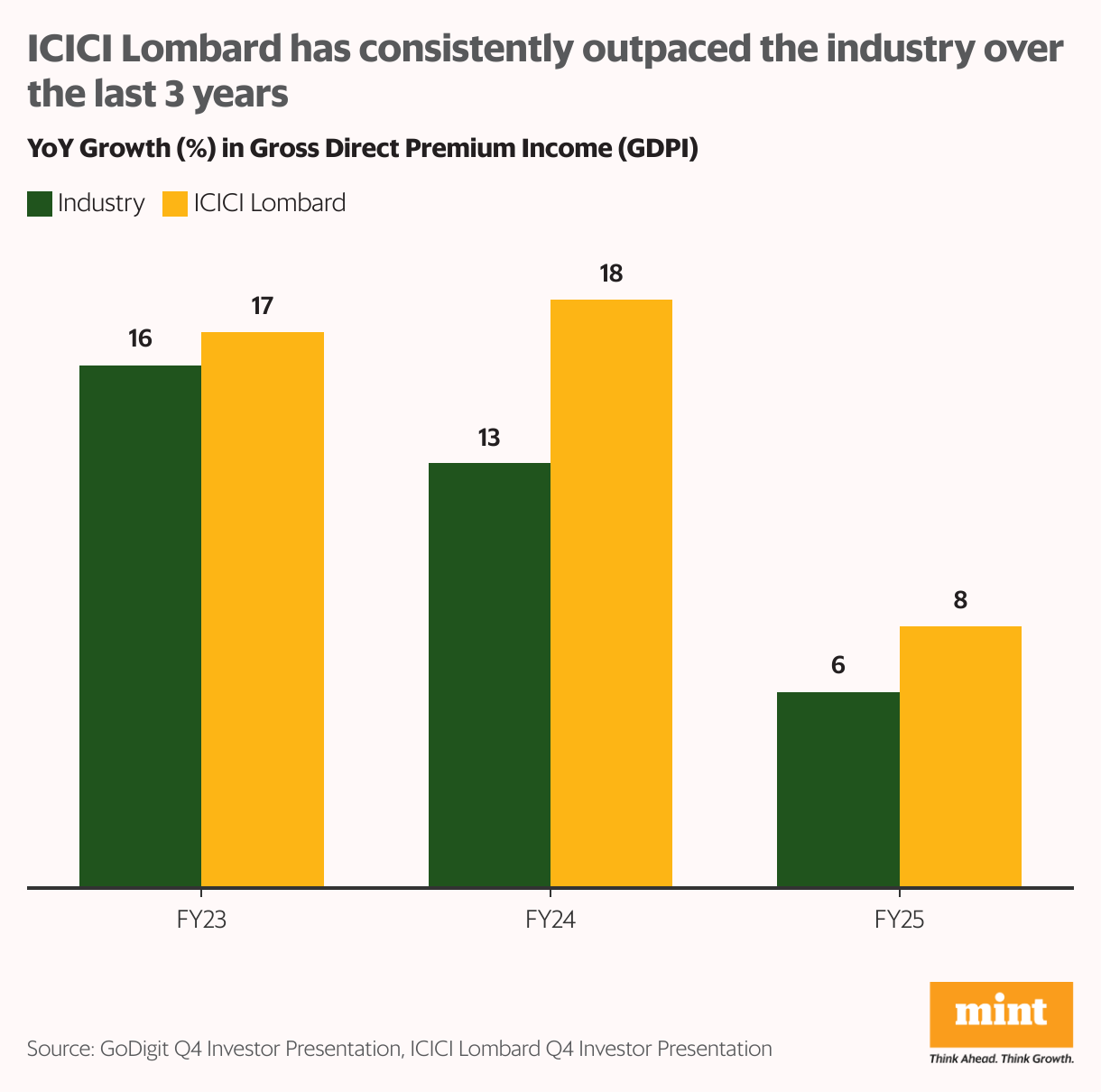

The company has seen a robust 13.1% CAGR growth in its GDPI (gross direct premium income) over the last 17 years. In fact, FY23 and FY24 reported even faster expansion at 17-18%. But growth slowed down sharply to 8.3% in FY25. Q4 numbers were even worse, with weak investment income contributing to a 1.9% year-on-year decline in profit for the quarter.

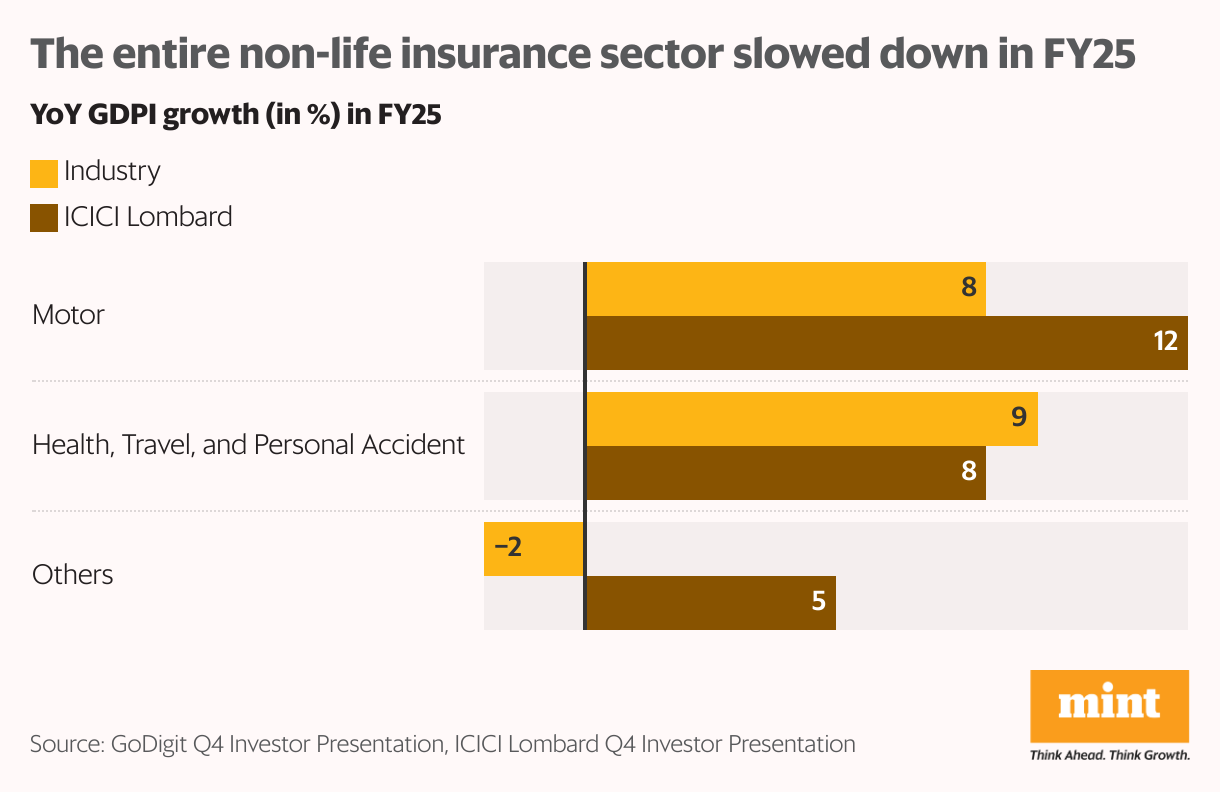

It is important to note, however, that this was an industry-wide phenomenon driven primarily by a slowdown in the sales of new vehicles during the year. With a muted 8% growth in the mainstay segment of motor insurance, the non-life insurance sector reported just 6.2% growth during the year.

The new rules by the Insurance Regulatory and Development Authority (Irdai) mandating deferred accounting of long-term policies instead of billing them upfront also played a role. Adjusted for the new accounting norms, the industry reported 8.6% growth.

Even as competition weighed on ICICI Lombard’s group health insurance segment, it surpassed industry growth in other segments. The company’s focused efforts on older vehicles and commercial vehicles, as well as its improved portfolio segmentation, have worked in its favour. Removing the impact of the new accounting norms, the company’s GDPI outpaced the industry with 11% year-on-year growth.

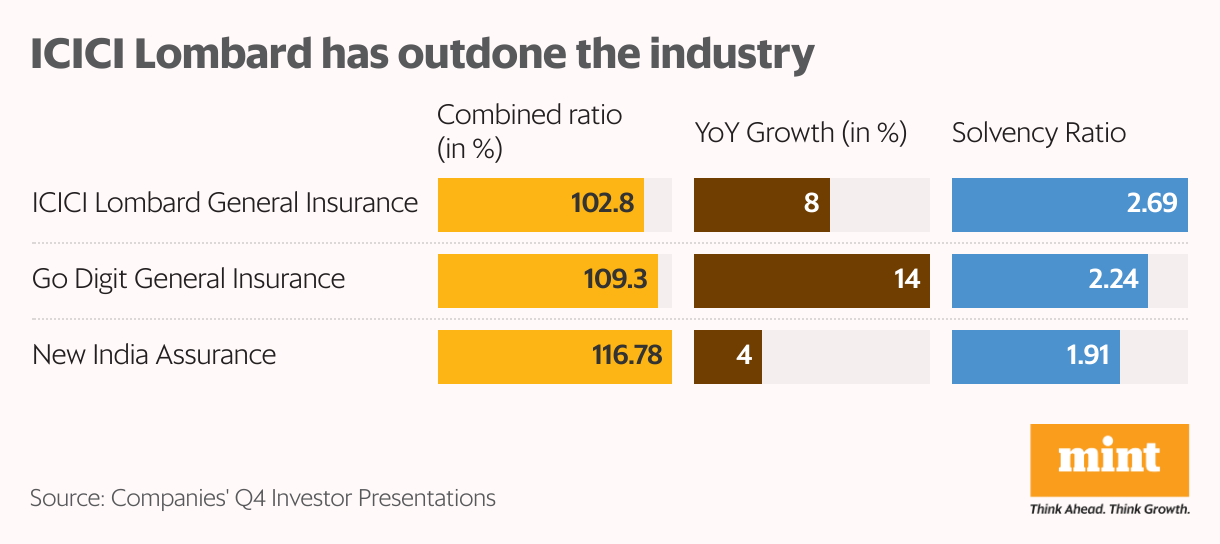

The lower loss ratio in motor insurance negated the rising losses in health and crop insurance. Overall loss ratio remained largely stable at 70.6% in FY25 versus 70.8% in FY24. Lower expense ratio continued the business’ moderation in combined ratio (loss ratio + expense ratio) to 102.8%. Excluding the impact of catastrophic (CAT) losses, the ratio stood even lower at 102.4%. Its bottom line expanded by 30.7% to ₹2,508 crore during the year.

Still, bogged down by the topline slowdown and brokerage downgrades, the counter corrected by as much as 4% following the earnings announcement.

Also Read: United Spirits is on a high after RCB's IPL win, JP Morgan upgrade and UK FTA. Can it keep buzzing?

Long-term industry prospects remain promising

India is the fourth-largest non-life insurance market in Asia. But the premiums constitute only 1% of GDP, against a global average of 4%. Even compared to emerging economies, India’s general insurance is underpenetrated. The total addressable market stands at $36 billion, and it has ample room for growth.

Premiumization in automobiles and increasing EV adoption should support growth in motor insurance. Meanwhile, improving penetration in health, property and casualty insurance is expected to drive growth in these segments.

Increasing penetration of digital insurance is also expected to push growth. Over the last three years, online motor insurance has seen much faster adoption in lower-tier cities. Against a 35% growth in online motor insurance in tier-1 cities, tier-2 and tier-3 cities have seen significantly higher growths at 70% and 110%, respectively.

Also Read: These three large-cap stocks are trouncing the Sensex in 2025—so far

Robust fundamentals

ICICI Lombard is one of India’s leading non-life insurers with 8.7% share of industry GDPI. While it commands barely 3% share of the health insurance segment, its expansive distribution through its promoter bank, 1.4 lakh individual agents and almost 1,000 virtual offices have helped it outpace the industry in other segments.

It leads the property and casualty insurance segment with 13% share in fire insurance and 20% in marine insurance. It also has high double-digit shares of India’s engineering and liability insurance segments. Since FY23, ICICI Lombard has outrun the industry with consistently superior fundamentals. The stock’s outperformance over the last 3 years reflects this optimism.

With a data analytics-driven approach, the company has been able to balance growth and risk management. Its focus on profitable growth through conservative underwriting has been bearing fruit. The combined ratio has improved over the years and is significantly ahead of the competition.

Its reserves are also robust. Incurred but not reported (IBNR) utilization continued to improve during the year, indicating the robustness of reserves. The solvency ratio of 2.69x is comfortably ahead of the regulatory minimum of 1.5x and its peers.

Also Read: Analysts and investors have soured on Asian Paints. Can it prove them wrong?

Strong outlook despite risks

Anticipating a sustained slowdown in auto sales, the non-life insurance industry is likely to continue in the slow lane over the next couple of years. ICICI Lombard faces an additional risk from its health insurance segment, which has lagged the industry amid intense competition. Any further pickup in competition, spike in claims, or drop in investment income can weigh on the business.

But the stiff pricing competition faced lately from public insurers in retail-focused segments should abate over the next few years, as players gradually conform to the regulatory cap of 30% on expenses of management (EOM), including commissions and promotional expenses. The company also stands to benefit from investments made in recent years towards the expansion of products and distribution in its health insurance segment. Any relief on GST in health insurance can also benefit the company. It is targeting a double-digit growth in the segment.

Over the longer term, industry tailwinds should help support growth, while increasing digital penetration can improve profitability. ICICI Lombard’s focus on enhancing penetration in tier-3 and tier-4 cities can be expected to drive growth for the company. Meanwhile, its conservative underwriting should support margins. Management has guided for its combined ratio to continue down the glide path to around 101.5% by FY27.

Its target price has been pegged at ₹2,200 apiece, valuing the business at 32 times its FY27 earnings. This reflects an upside of 8% over current levels.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder ofCredibull Capital, a SEBI-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.