Banks have had a rough ride, but some bucked the trend

")

- As Indian banks grapple with competition and regulatory challenges, some have managed to turn the tide. These lenders have showcased remarkable resilience with robust growth in deposits and loans

Indian banks have been through some tough times lately. Retail lending skyrocketed after the pandemic, leading to intense competition and soon followed by stress in the segment. The regulator responded by tightening the guardrails, resulting in a slowdown in retail credit in an environment already marred by subdued corporate credit. Deposit growth has been hit, too, as domestic assets found their way from bank deposits towards stock markets.

Silver linings against a sombre cloud

In these troubled times, banks have posted low double-digit growths for FY25. Some banks like HDFC performed better on deposits with more than 15% growth, while their credit-growth was much slower at just about 7%. On the other end of the spectrum, we have the likes of UCO Bank which registered 20% growth in advances while their deposits grew by just 10%.

However, against this rather gloomy cloud, a couple of banks draw out a silver lining. Mid-sized banks which have been focused on fast-growing retail loans while appropriately controlling for stress in the segment, have managed to buck the trend.

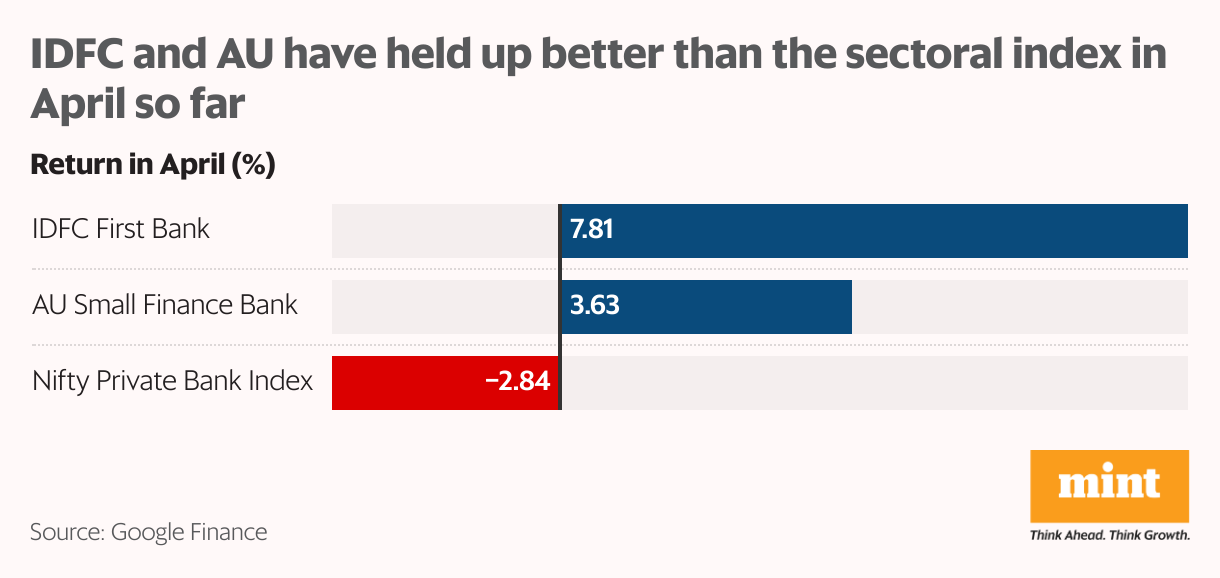

AU Small Finance Bank and IDFC First Bank have closed FY25 with more than 20% growth on both, deposits and advances. Their stocks reflect this optimism, having appreciated by 3.6% and 7.8% respectively this month, even as the broader private bank index has corrected by 3%.

The AU advantage

We have previously covered how AU Bank’s recent fortunes are closely linked to its merger with Fincare Small Finance Bank. The merger led to a higher share of microfinance on AU’s books, which has seen sharp growth recently. While the segment has also seen higher stress and the regulator’s wrath, the superior as well as diversified credit profile of AU’s borrowers has helped it sail through. Credit growth has mellowed from 46% in FY24 to 25.8% in FY25, but it is still the best in the industry.

Furthermore, a fifth of its microfinance book is eligible under the government’s credit guarantee scheme. AU has also invested in improving its collection efficiency, while remaining stringent with its provisioning norms. This has helped control the stress on its books, and command higher investor confidence.

It has also been one of the primary beneficiaries of regulatory tailwinds. The RBI’s reversal of higher risk weights on microfinance has helped credit growth. Moreover, since two-thirds of its book comprises fixed-rate loans, it stands to benefit more from the monetary easing cycle, which was formalized this week with another 25-bps cut and an official change in the RBI’s stance.

IDFC has doubled down on deposits

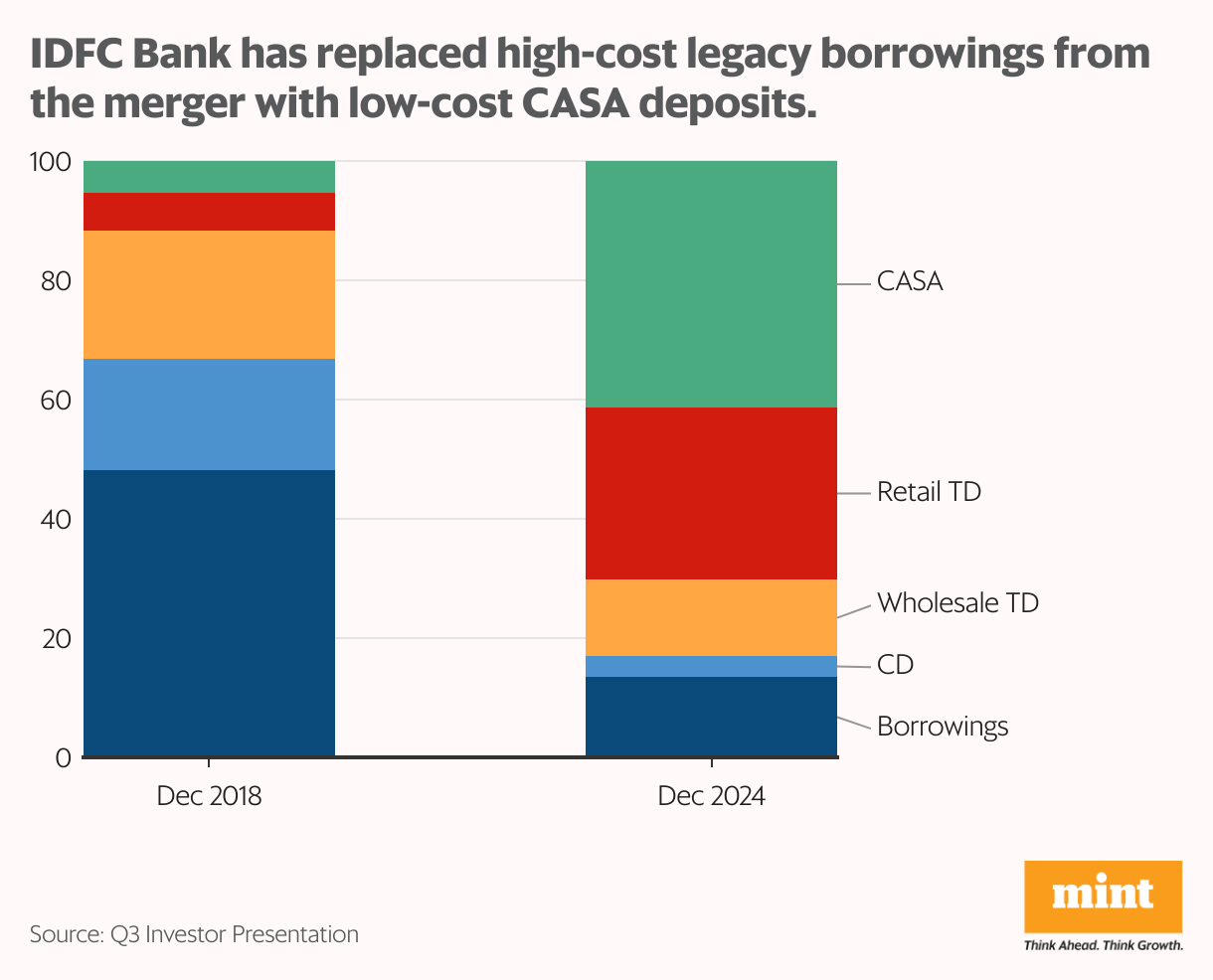

Since the merger with Capital First in 2018, the IDFC management has had a hawk-eye focus on growing its deposit base. High-cost legacy borrowings have been retired and replaced with low-cost retail customer deposits. Branch footprint has been expanded from 206 branches to almost 1,000 branches. Deposit mobilisation per branch has seen an even starker improvement. In FY24, the bank mobilized 2 times more deposits per branch compared to its peers.

How? Not only has the bank pulled in customers with attractive interest rates going as high as 7.25% and schemes such as the extensively advertised monthly interest payouts, but it has also retained customers by upping its tech and customer support game. Its digitization initiatives have helped improve customer satisfaction, and its mobile banking app has been ranked the best in the industry by Forrester.

IDFC’s deposit-centric strategy has paid off

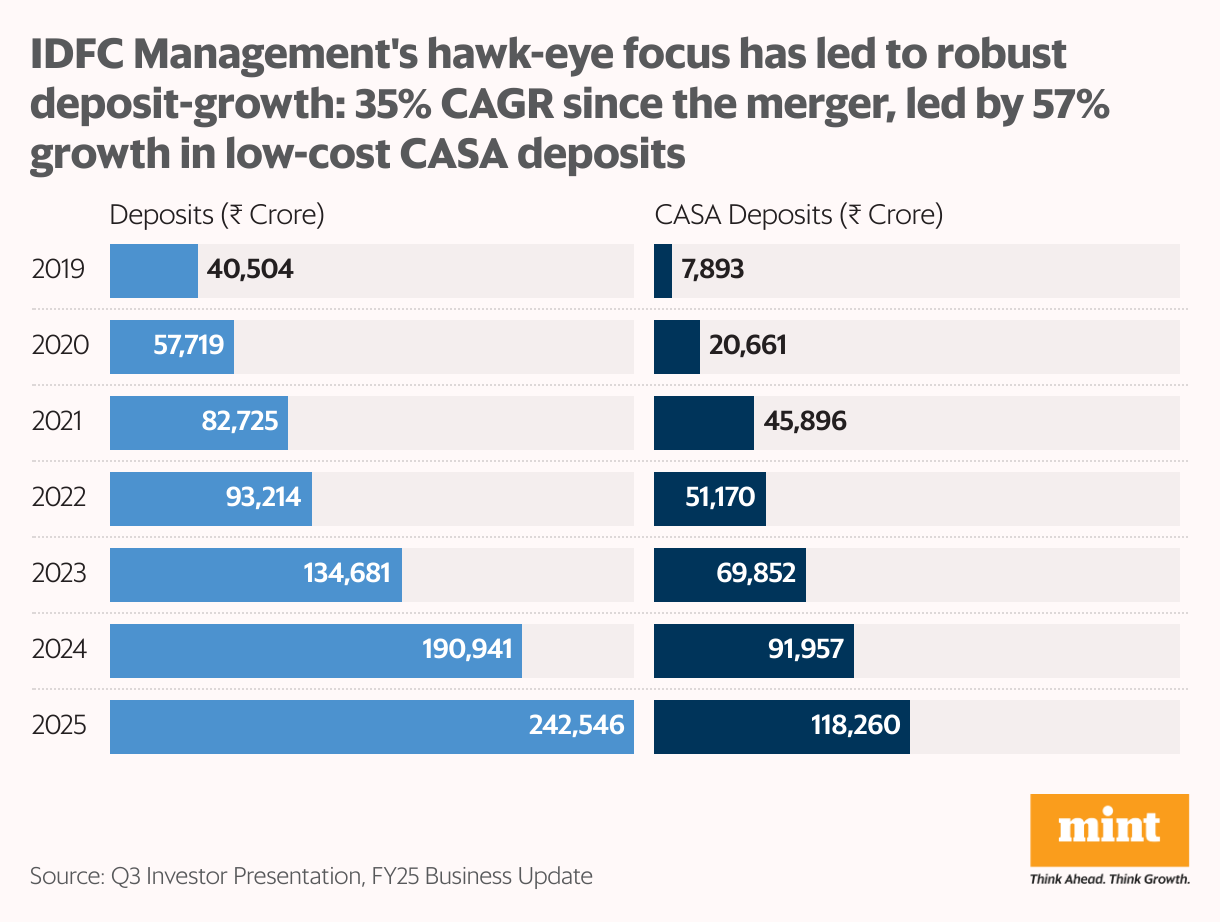

The proof is in the pudding. Since 2018, the bank’s loan book has more than doubled, while its deposits have expanded by a whopping six times—from ₹40,000 crore to more than ₹2,40,000 crore. More importantly, deposit growth has been driven by 57% CAGR growth in low-cost CASA deposits. This has helped substantially improve its CASA ratio from 8.7% to 46.9%, thereby moderating the bank’s cost-of-funds to 6.38%—among the lowest for mid-sized banks.

After expanding the deposit base by 42% in FY24, the management has guided for 25% CAGR growth between FY25 and FY27. So far so good, as FY25 saw customer deposits growing by 25.2%. Considering that 80% of the bank’s deposits come from retail customers which tend to be stickier, the bank is expected to deliver on its deposit-growth guidance.

Deposit growth has enabled credit growth

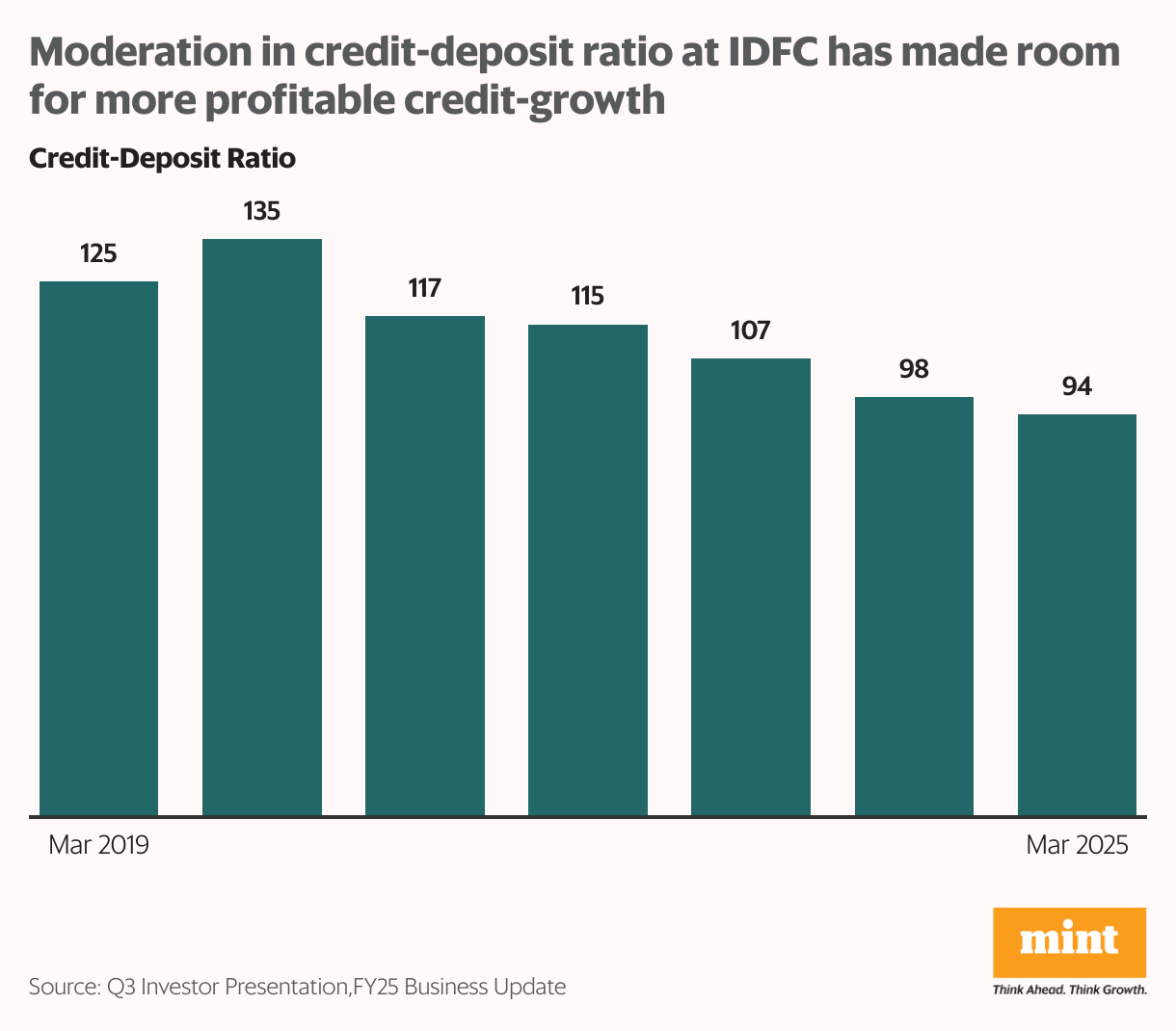

Immediately after the merger, IDFC had a credit-deposit (CD) ratio of 137%, which meant that it had to rely on high-cost borrowings to further credit growth. High CD could also potentially lead to systemic risks arising from capital inadequacy and asset-liability mismatch.

But over the years, as deposits expanded, the CD ratio has moderated to 93.8% as of March 2025. The incremental CD ratio for the latest quarter was even lower, at 75.7%. The resulting low cost of funds has enabled more profitable credit growth.

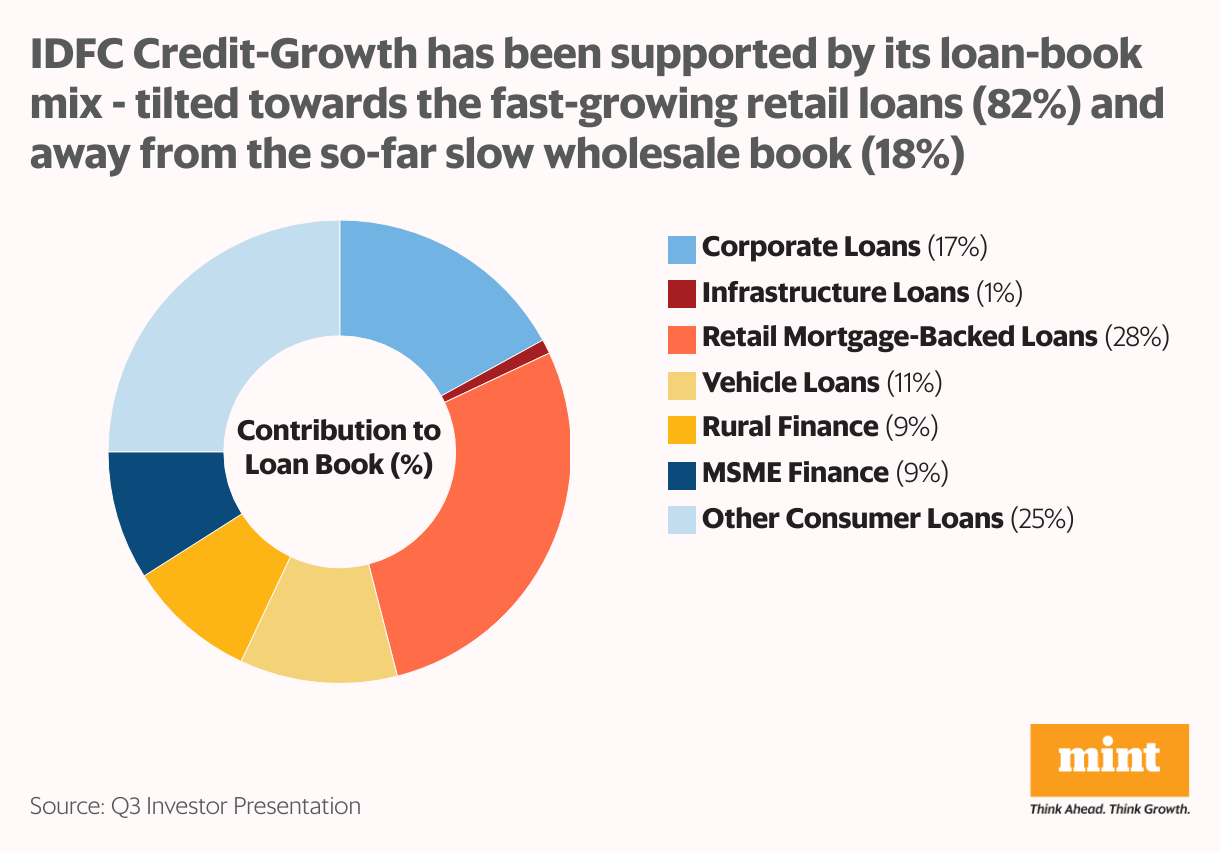

Retail focus has helped credit growth

In recent years, retail lending has accelerated, while crowded-out private capex kept corporate credit sluggish.

Against this context, IDFC’s loan mix has worked in its favour. 82% of its advances were concentrated in the fast-growing retail lending and MSME segments, while sluggish wholesale loans comprised only 18%. Consequently, IDFC posted healthy credit growth of 20.3% in FY25.

Also Read: Loan growth slows for banks in Q4 as liquidity stays tight, deposits lag

Stress managed

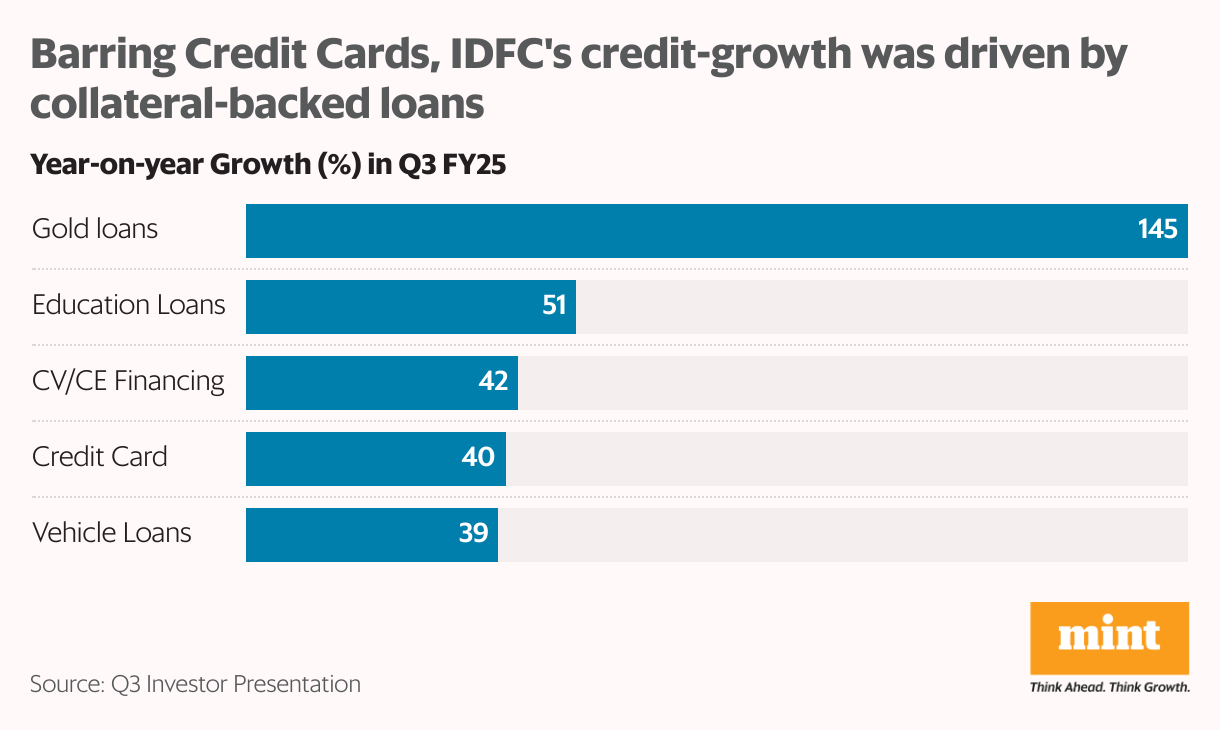

Despite the focus on retail lending, only 14% of IDFC’s book is exposed to unsecured retail lending. Remaining 68% of retail loans are backed by collateral, and have been spared the recent stress.

Moreover, IDFC’s recent credit growth has also been primarily driven by collateral-backed loans such as gold loans, education loans, and CV/CE financing. This is to say that the growth has not come at the cost of additional stress. IDFC also follows stringent underwriting and collection processes, which have led to overall stable collection efficiency and improving asset quality. Gross NPA declined from 2.8% to 2.2% over FY25.

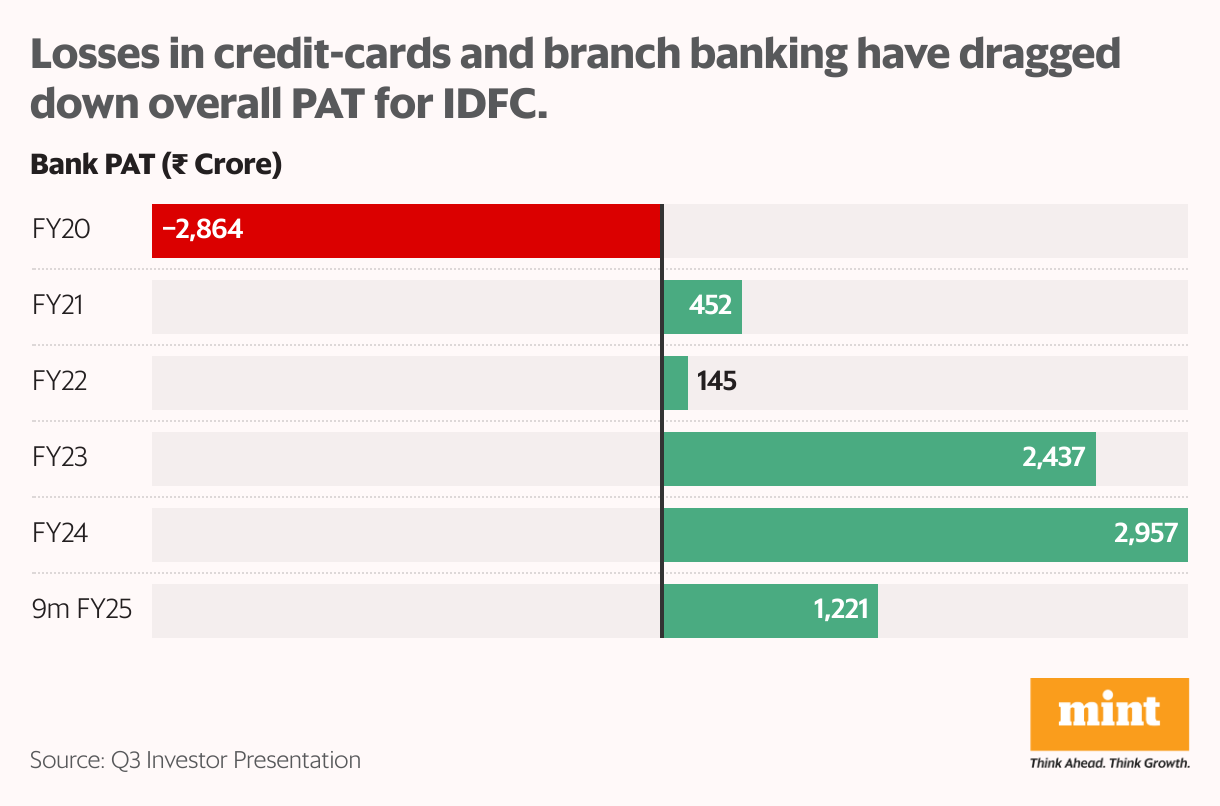

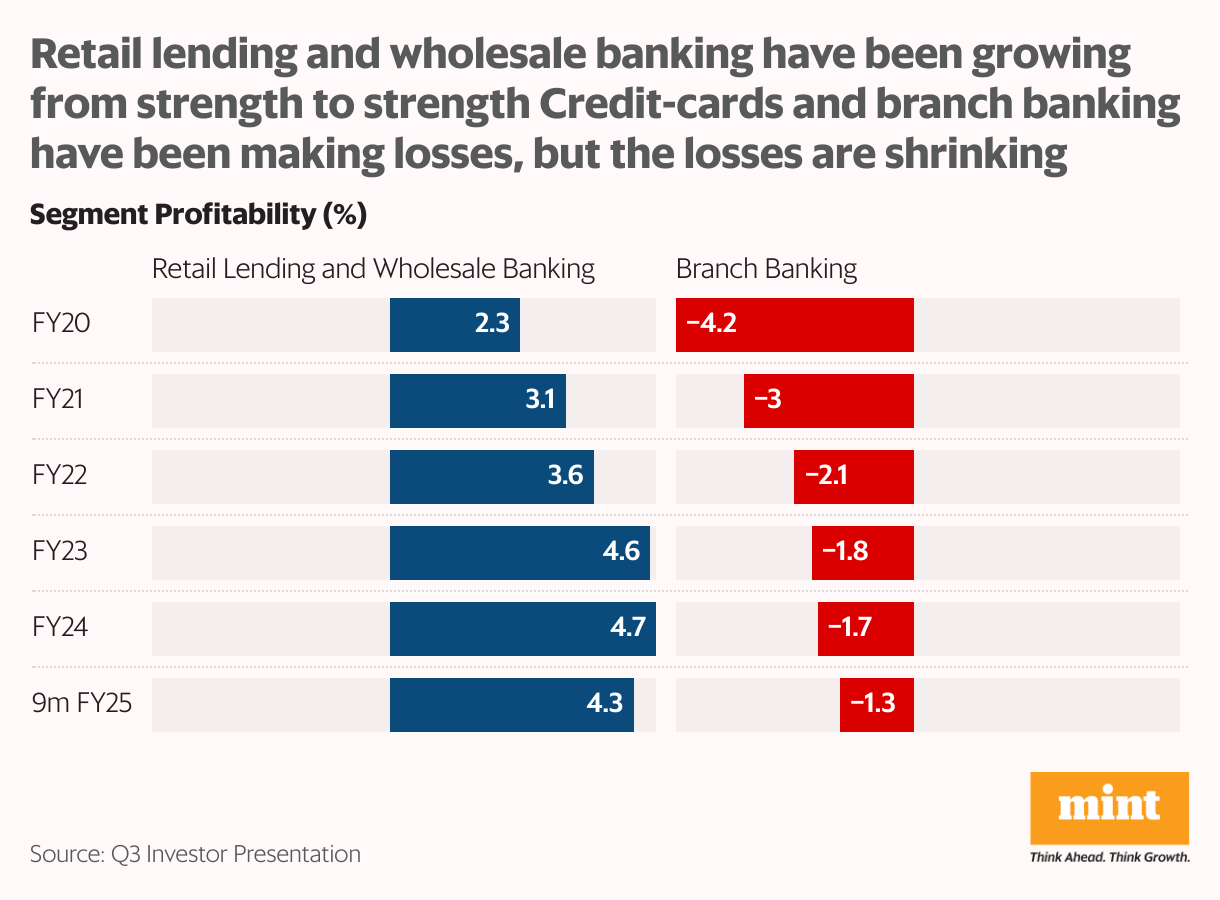

Loss-making segments to breakeven soon

While IDFC’s lending business has remained robust, the bank’s overall profitability has been dragged down by losses in branch banking and credit cards.

That said, scale is picking up in credit cards. And the management has been prioritizing deposit mobilization per branch, rather than blindly expanding the branch footprint. So, the losses have been shrinking and these businesses can be expected to breakeven soon.

Also read | How bad loans ruined India’s banking system

Risks remain

When private capex picks up, growth in corporate credit can be expected to surpass that in retail lending. This would work against retail-focused lenders like IDFC.

Furthermore, IDFC has seen significant stress in its infra book due to concentration in a business which turned belly up. Its rural and non-infra corporate books are under stress too. In fact, in its microfinance book, pre-NPA portfolio has increased significantly year-on-year from 1.27% to 4.56% in December 2024.

But IDFC proactively provisions for loans which turn overdue by even 30 days, even as regulations require provisioning only after 90 days. While these provisions have shaved at least Rs.425 Crore off its bottom line in FY25, they reduce the risk of hidden stress lurking around the corner. Its provision-coverage has seen an improvement from 68.8% in FY24 to 73.6% in December 2024, which limits further impact on its bottom line.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.