JM Financial stock rebounds 60% from its low. Will the clean-up rally sustain?

")

JM Financial has shifted away from risky wholesale lending to fee-based capital markets and retail housing finance. The benefits of this shift are expected to emerge gradually from FY26. So, how is the company repositioning for this transition?

JM Financial’s stock has bounced back sharply, rising 60% from a low of ₹88 on 7 April to ₹141 on 17 June. The rally reflects investor optimism around the company’s efforts to achieve steady growth and improve returns.

The company has shifted away from risky wholesale lending to fee-based capital markets and retail housing finance. With the clean-up largely done, it's now eyeing a leaner, asset-light model, with a sharper focus on its core capital markets businesses.

The benefits of this shift are expected to emerge gradually from FY26. So, how is the company repositioning for this transition?

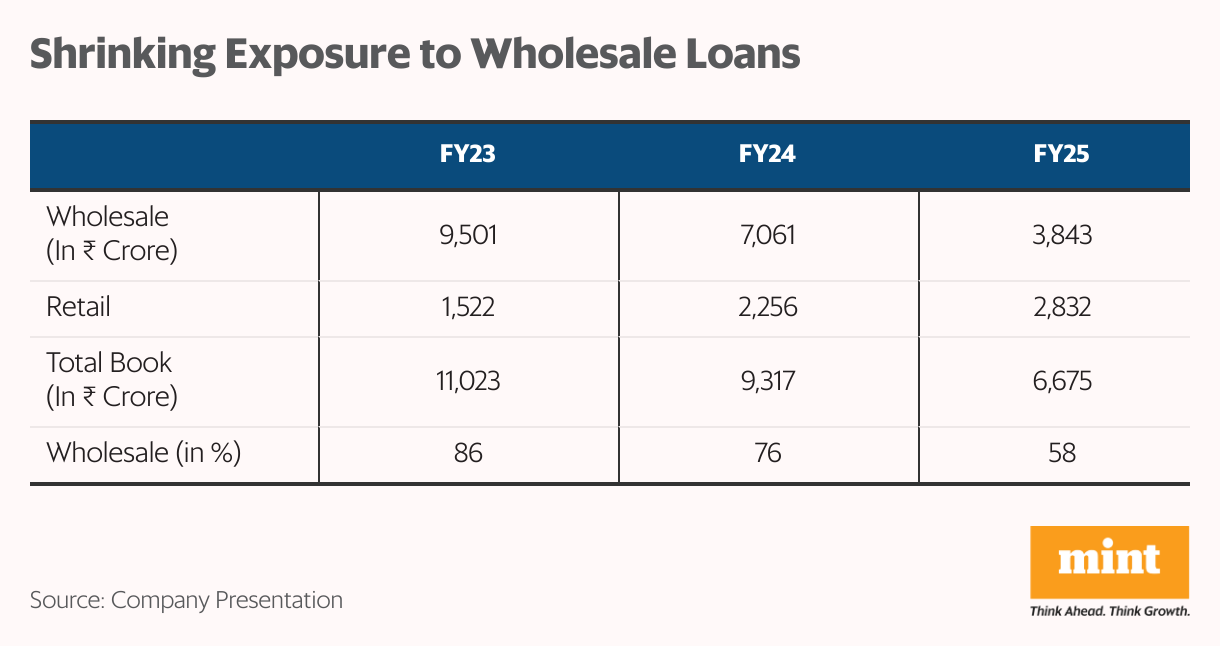

Wholesale book shrinks, retail picks up

This wholesale lending segment stems from the mortgage lending vertical, split between wholesale and retail lending. Mortgage lending contributes 29.6% to total revenue but only around 10% to profitability.

In wholesale lending, JM Financial had a high exposure to riskier areas, including real estate, project finance, and early-stage funding. These were largely funded through an on-balance sheet model that tied up capital, increasing the risk in case of default.

As of FY23, the wholesale book stood at ₹9,501 crore, accounting for 86% of the total loan book of ₹11,023 crore. The remaining 14% came from retail lending, primarily the affordable housing segment.

Also Read: Affordable housing financiers get a RBI rate cut boost. But it may not last.

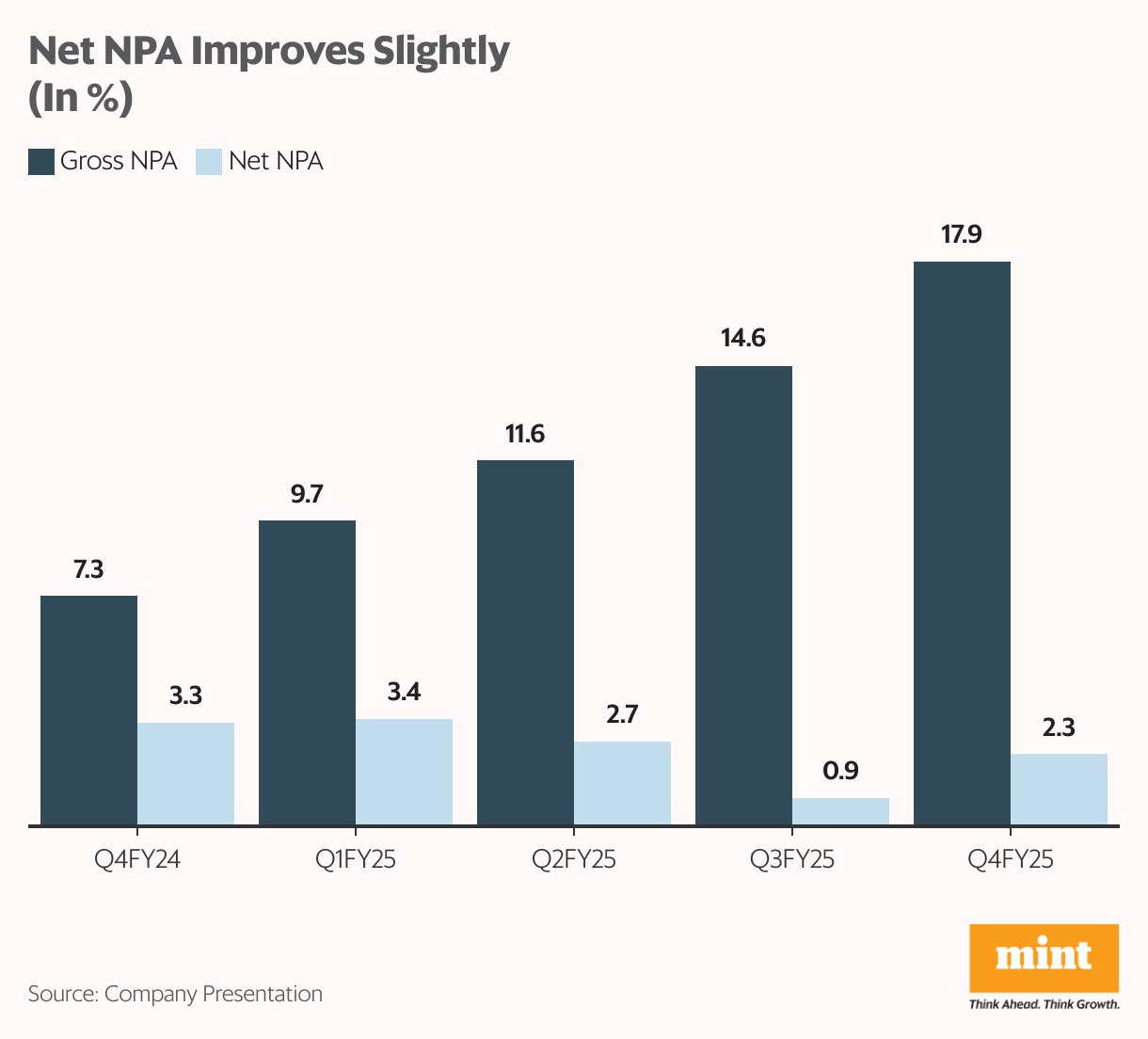

However, this concentration towards wholesale eventually backfired. Lower recoveries and asset quality stress pushed net NPA to 3.3% in Q4FY24, hurting profitability. At the same time, Reserve Bank of India's (RBI) regulatory changes in areas, including land financing and early-stage project funding forced JM Financial to reduce its exposure.

In response, the company started an impairment-led clean-up. It impaired its exposure worth over ₹1,000 crore, including ₹425 crore in FY24, and ₹577 crore in FY25. The effects of this clean-up are now showing.

The wholesale book more than halved to ₹3,843 crore in FY25, with its share in the loan book falling to 58% from 86% in FY23. At the same time, retail now accounts for 42%, up from just 14%. Net NPA improved to 2.3% in Q4FY25, down from 3.3% a year ago.

However, gross NPA rose to 17.9%, up from 7.3%, reflecting continued stress from legacy assets. The company, however, has increased its provision coverage to 87% from 65% to deal with future stress.

Segment profit declined to ₹31 crore in FY24, from ₹162 crore in FY23, due to impairment, and provisions. But with impairment tapering in FY25, PAT recovered to ₹85 crore. With most of the clean-up done, the segment is now expected to stabilise.

Leaner lending model

JM Financial is now moving towards a leaner, capital-light lending model. It is targeting high-quality developers, where it plans to participate in equity and credit transactions, offer construction finance, and syndication services.

The syndication model allows JM Financial to facilitate loan disbursements without deploying its capital, thereby generating steady fee income. It will, however, maintain a smaller exposure of under ₹3,000 crore.

The company expects to generate a 12-13% yield on this book, with an additional 1-2% from syndication fees. It also expects to recover the entire ₹1,000 crore impairment by FY28, which could support earnings over time.

Retail lending gains momentum

JM Financial is also doubling down on its affordable housing loan business. In FY25, revenue rose 43% from last year to ₹368 crore, while profit grew 50% to ₹59 crore. The loan book expanded 26% to ₹2,832 crore. The company aims to scale this business aggressively.

The management aims to grow the loan book at a 30% CAGR, reaching ₹5,000 crore by FY27 and ₹10,000 crore by FY30. The branch network is expected to expand from 128 to 200 by FY28 and further to 275 by FY30.

Return metrics are also expected to improve. Return on equity (RoE) is projected to rise from 8.5% to 12% by FY28, and to 14% by FY30. Return on assets (RoA), currently at 2.5%, is expected to improve to 3% by FY27. Improving overall metrics would be a major catalyst for the company's stock price.

Investment banking still leads

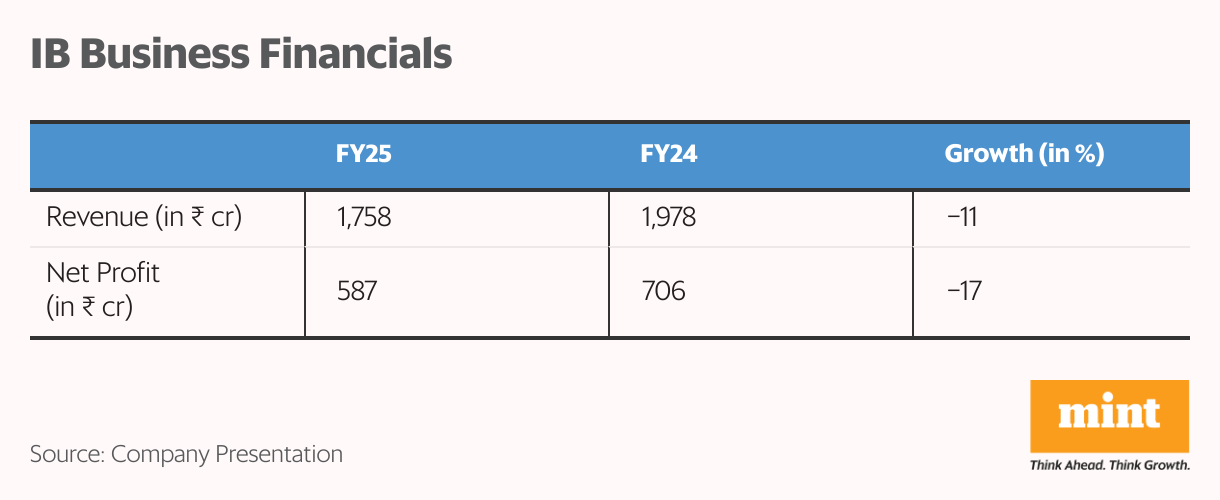

Investment banking remains JM’s core business, contributing 39.5% to revenue and 71.5% to profitability. It acts as a direct proxy for capital market activity.

In FY25, JM was the top player in QIP (qualified institutional placement) deals, helping raise over ₹80,000 crore for companies.With a robust transaction pipeline for the current fiscal year, management anticipates that the growth momentum will continue. It is also expanding its client base across sectors and geographies.

This segment also houses wealth management. In FY25, wealth AUM rose 11% from last year to ₹1.1 trillion. Of this, ₹78,388 crore came from the non-retail segment and ₹31,191 crore from retail clients.

In the non-retail category, 24% of AUM comes from recurring revenue, a more stable recurring income stream. The rest is transaction-based and depends on transaction volumes. JM aims to increase the share of recurring revenue, which provides better revenue visibility.

It sees wealth management as a key long-term growth driver. The company has already doubled its sales team in the past two years, in line with peers. In FY25, this segment reported revenue of ₹1,300 crore and a net profit of ₹133 crore.FY24 numbers for this segment aren’t disclosed separately.It plans to scale this business over the next 3–5 years, positioning it as a key growth driver.

Overall, the investment banking segment revenue fell 11% to ₹1,758 crore, while net profit fell 17% to ₹587 crore. The decline was primarily due to a high base in FY24 and weaker market activity in H2FY25.

Also Read: Adani Ports bets big on doubling revenue by FY29. But execution is everything.

Platform AWS scaling, but profitability low

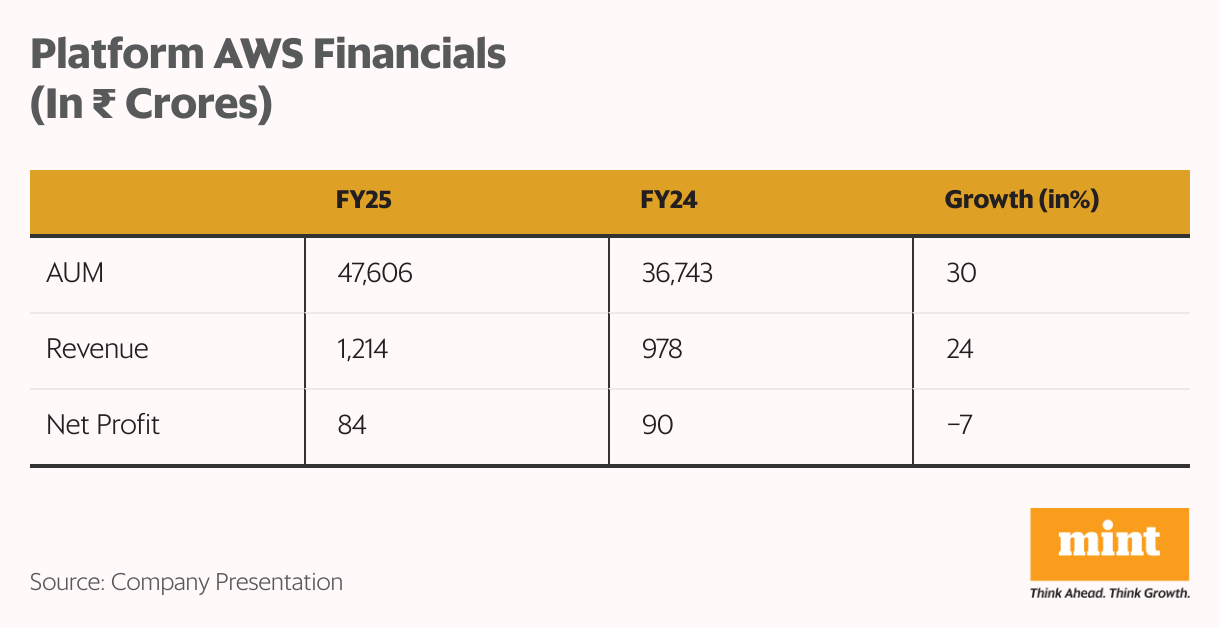

This segment includes mutual funds, retail wealth, and elite wealth businesses. It contributes 27% to revenue and about 10% to profitability. In FY25, total AUM rose 30% to ₹47,606 crore. Mutual fund contributed 28%, while retail and wealth together make up 72%.

The mutual fund (MF) business has established a significant presence in the industry over the last two years, driven by retail-led growth and strong fund performance. In FY25, MF AUM nearly doubled to ₹13,419 crore from ₹6,189 crore in FY24. About 77% of AUM is in non-liquid funds, with the rest in liquid funds.

The company currently operates in 18 cities across India and plans to expand into tier 2 and tier 3 locations. It has also announced plans to set up alternate investment funds (AIFs) across asset classes. However, this business is still in its early stages. Revenue stood at ₹78 crore in FY25, with a net loss of ₹26 crore. Management expects this vertical to break even by FY27.

Beyond mutual funds, retail wealth AUM rose 8% to ₹31,191 crore, while elite AUM rose 36% to ₹2,584 crore. It has also launched a digital broking platform—BlinkX—which is expected to gain traction in FY26, depending on market conditions.

Platform AWS segment revenue rose 24% to ₹1,214 crore, but net profit fell 7% to 84 crore. This is due to higher cost-to-income ratio, due to the ongoing expansion.

Also Read: The ONDC mutual fund pipeline has arrived. Will it take over the industry?

Profitability may improve after FY25 reset

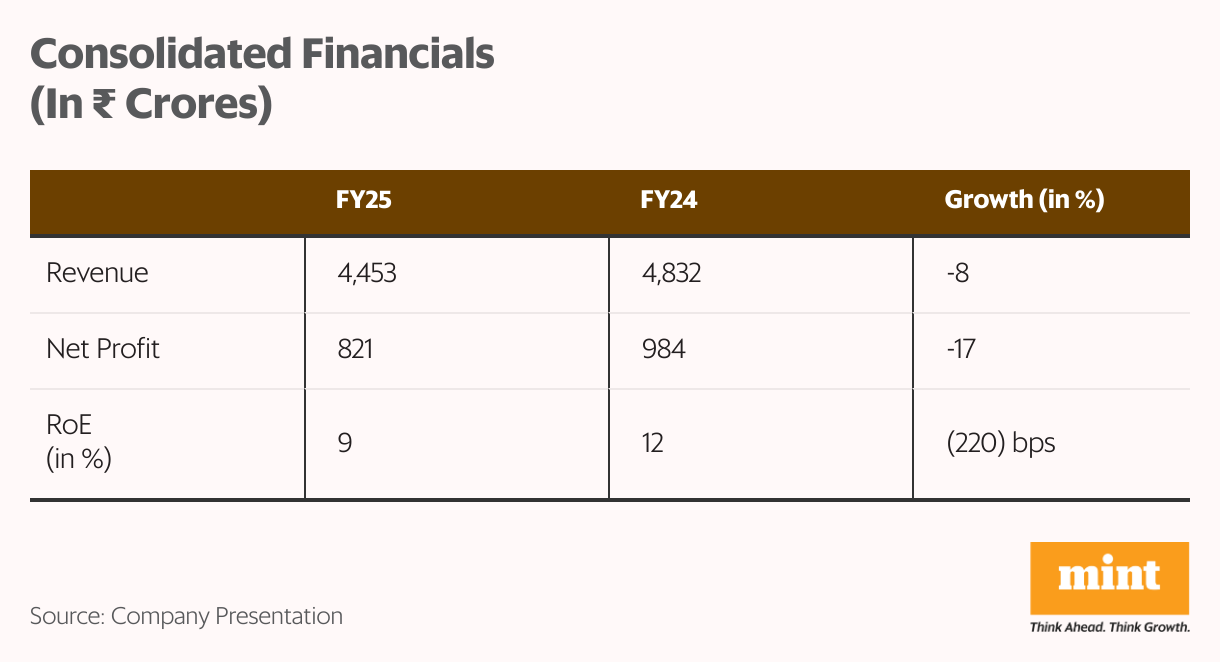

On a consolidated basis, JM Financial's revenue declined 8% to ₹4,453 crore, from ₹4,832 crore in FY24. At the same time, net profit (adjusted for exceptional items) declined 16.5% to ₹821 crore. It also paid its highest-ever dividend of ₹2.7 per share (up from ₹2 in FY24), and aims to double this over the next three years.

Management has termed FY25 a reset year. As segments like mutual funds and wealth management scale, profitability is expected to improve. The improving dividend also signals confidence in earnings quality.

With the wholesale book behind and capital-light segments scaling up, profitability and, in turn, return metrics should improve. RoE, currently at 9.4% (down from 11.6%), is also expected to inch back up.

Rerating in progress, but still undervalued

JM Financial trades at a P/E of 18x, above its 10-year median of 13x. But compared to Edelweiss Financial (P/E: 26x), which has a similar business mix, JM still trades at a discount. So, despite the recent stock rally, valuations remain reasonable.

Also, with a pure capital market focus, JM can attract higher valuation, in-line with peers. However, execution remains the key. Earnings growth, expansion of mutual fund and wealth management business along with improving return ratios should be the key catalysts for the stock.

That said, JM’s business remains cyclical. A slowdown in capital markets or fundraising could affect its core investment banking business. While the company is diversifying into wealth and asset management, concentration risk remains for now.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article. The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.