Lalithaa Jewellery IPO: Is the gold rush hiding governance glitches?

The company, which filed draft IPO papers this month for a ₹1,700-crore offering, has grown impressively over the past few years without taking on more debt. But it has also drawn flak for its governance practices.

Lalithaa Jewellery is planning its public debut as gold trades near all-time highs. Acquired from a struggling jeweller in 1999, the company has grown manifold over the years. Now, management aims to take the business to the next level with an IPO.

The draft red herring prospectus (draft IPO document) filed this month details a public issue worth ₹1,700 crore, comprising a fresh issue of ₹1,200 crore and an offer for sale worth ₹500 crore by the promoter. More than ₹1,000 crore of the proceeds will be used to add more stores, the company said.

So far so good, but the company has drawn flak for its governance practices. Specifically, related-party transactions related to the payment of brand ambassador fees to its promoter has raised eyebrows. That said, the brand ambassador deal with the promoter has since been terminated, and the controversial fees will not feature on its statements starting FY25.

But does this hint at deeper governance issues, or can it be discounted as a one-off slip up by an otherwise promising business?

Focus on south holds potential

India is the world’s second-largest gold market, with 70% of the demand attributable to gold jewellery. Often viewed as “stree dhan" (women’s wealth) in India, Indian women are almost certain to receive gifts of gold jewellery during their weddings to help them become financially secure. According to the Gold and Jewellery Export Promotion Council (GJEPC), India’s fine-jewellery market is valued at ₹4.5 trillion.

With south India having a higher share of working women and a seemingly greater love for gold, the region accounts for 40% of the national gold jewellery market. This bodes well for Lalithaa Jewellery, which derives 95% of its revenue from gold jewellery and has stores concentrated in the south.

Also read: A little-known stock that quietly delivered 15,000% returns—and still has room to run

Of course, organised players comprise only about 40% of the market. But as the economy evolves, the middle-class expands and the trust for branded jewellery picks up, their share is expected to rise.

Growth and deleveraging have gone hand-in-hand

Lalithaa’s revenues have increased at a healthy compound annual growth rate (CAGR) of 16% from R 6,083 crore in FY17 to ₹16,788 crore in FY24. The company clocked ₹12,595 crore in just the first nine months of FY25.

Commendably, the company has managed to grow without taking on more debt. As per reports, back in FY17, debt amounted to almost two times the company’s equity. With consistent fiscal prudence, the debt-to-equity ratio has been slashed to 0.5 as of December 2024. The company reported total debt outstanding at ₹1,215 crore as of April 2025.

Margins leave investors wanting

The company has made low prices its selling proposition. In its advertisements, Lalithaa challenges customers to find comparable designs at lower prices elsewhere. Almost 60% of its revenue is from relatively cost-conscious customers in tier-2 and tier-3 cities. Its store expansion has been focused on these cities.

The south, where the company has established its presence, is also known to prefer traditional plain (unstudded) jewellery. While this reduces the financial risk from unsold stock compared to studded jewellery, plain jewellery is typically associated with lower margins.

The result? Lalithaa Jewellery operates at a profit-after-tax (PAT) margin of just about 2%. For comparison, consider its smaller and newly listed peer RBZ Jewellers, which boasts of margins above 7%. While this can be chalked up to its small size and other differentiating factors, even a larger player such as Kalyan Jewellers reports net profit margins of almost 3%. In fact, Lalithaa’s margins rank among the lowest in the industry.

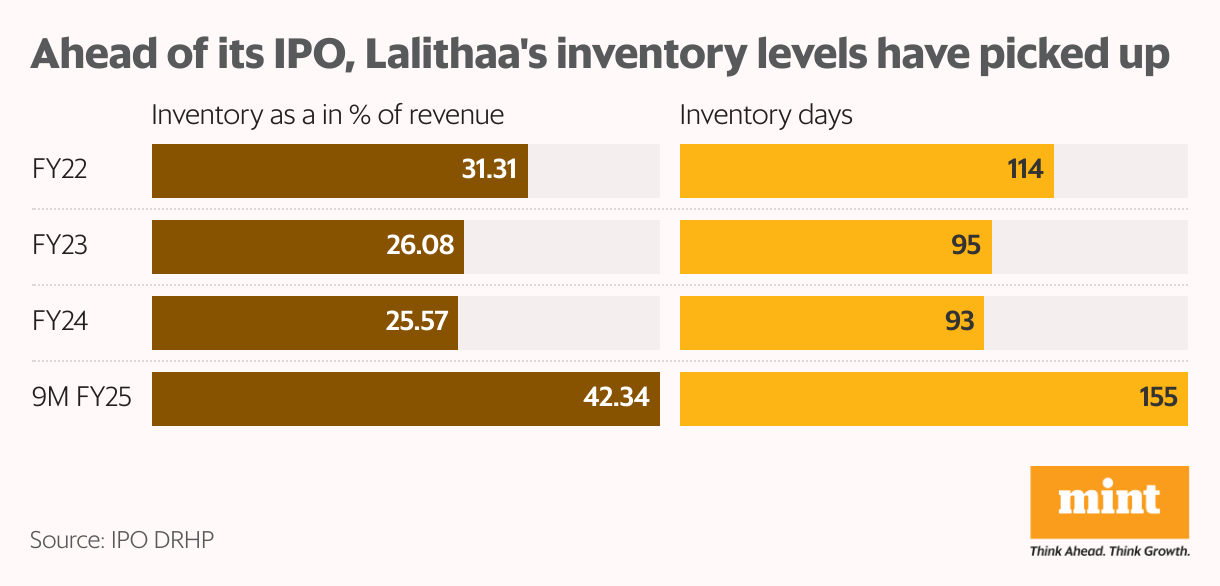

Concerns about cash-flow management

The company has had a history of intermittent negative cash-flows from operations. This is at least partially attributable to vendor concentration risk. With almost 70% of the cost of goods attributable to its top three vendors, the company’s payment terms are likely to have weighed on its working capital cycle.

To make matters worse, inventory has grown as a percentage of revenues from 25.6% in FY24 to 42% in the first nine months of FY25.

Also read: Zee’s ₹2,237 crore raise hides deeper strategic retreat

Unless the company achieved sufficient inventory clearance in Q4, cash-flow management in FY25 is likely to have become trickier. Even as plain jewellery is more easily recyclable, unsold stock still leads to loss of material and adds to manufacturing costs, affecting margins and cash flows.

Gold rally cuts both ways

Gold has turned significantly dearer in recent years as geopolitical and macroeconomic uncertainty has pushed investors towards the safe-haven asset. With a bulk of the uncertainty emanating from the US, gold has also benefited from the falling appeal of the US dollar among central banks. As yields fall amid monetary easing, the opportunity cost of holding metals falls.

But the rising price of gold cuts both ways. On one hand, it leads to inventory gains for jewellery manufacturers. On the other hand, it can result in higher raw-material costs and subdued demand. Currency depreciation and changes in import duties are adjacent risks.

Unlike its competitors, Lalithaa refrains from hedging its exposure to gold. This leaves it particularly vulnerable to fluctuations in its price. This could pose significant risk in subsequent quarters given that gold is trading near its peak, Lalithaa’s margins are already narrow, and the company is sitting on multi-year high inventory levels.

Other risks loom

Apart from the concern related to the brand ambassador fees paid out in previous years, the draft IPO papers also point out a deemed promoter group, Dilip Chhabria Design. It is under liquidation, and information on the group has been declared as unavailable. Lalithaa has also declared non-compliances under the Companies Act. Such a lackadaisical approach to governance and procedural controls does not inspire confidence.

The quality and design aesthetics of the company’s jewellery are deeply dependent on the skills of their employed and contractedkarigars. Loss of karigars to the competition, or their failure to adhere to quality standards, could erode Lalithaa’s edge over the competition and even affect its brand image.

Also read: How Vedanta's debt burden turned Hindustan Zinc into a net-debt company

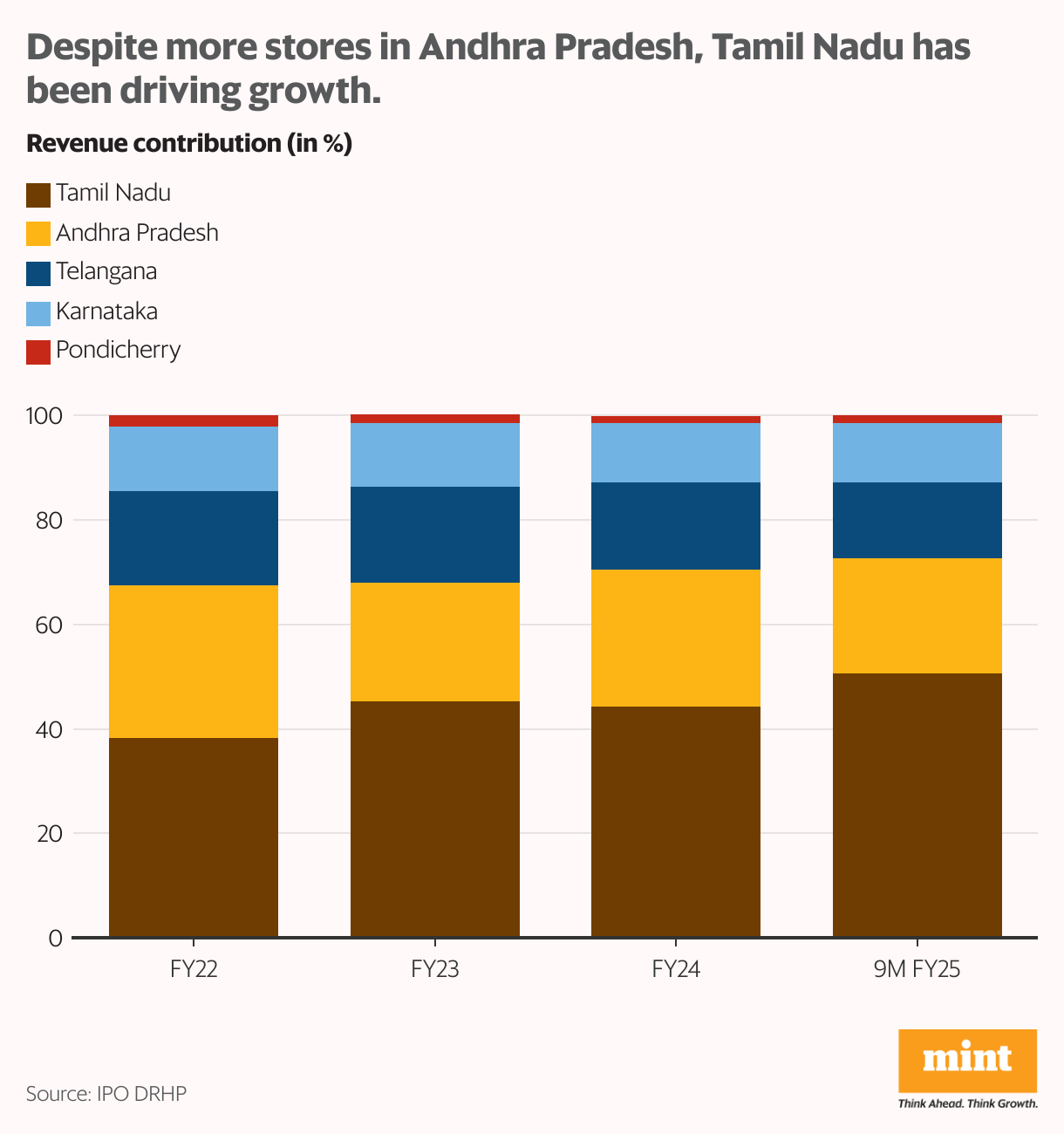

Stiffer competition from both organised and unorganised players could also derail the company’s plans. Despite a bigger store footprint in Andhra Pradesh, Tamil Nadu has been driving growth for the business. So, it’s no stretch to extrapolate that the planned store expansion may not yield the expected returns. This could result in closed stores and/or affect its already-thin margins.

The company has also drawn attention to legal and regulatory proceedings amounting to more than ₹600 crore against it and its promoter. A tax demand worth more than ₹1,000 crore is also under litigation. These numbers amount to more than four times the ₹360 crore profit reported in FY24. That said, the company expects the tax demand to drop by more than ₹600 crore, once the requisite order is issued by the appropriate authorities.

Finally, the company is valued at 44 times earnings, which is still lower than the 98 multiple for Kalyan Jewellers. But it is important to note that Kalyan Jewellers has seen faster growth and has wider margins.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.