Top 5 quality microcap stocks that are trading at cheapest valuations

")

- These microcaps are trading significantly lower from their book values and their 5-year average historical valuations.

"Investment is most intelligent when it is most businesslike," said Benjamin Graham, father of value investing.

Stocks are not mere pieces of paper but represent underlying businesses, and one should invest in stocks like they are buying a stake in the business.

Broadly, there are two ways to do such business-like investing.

First, you buy a stake in the business to profit from the rise in its fair value over time. As the company grows its business every year, its revenues increase. As its revenues rise, so do profits. And as this process continues over the years, the value of the company increases and with the profit-making capacity comes a higher market value.

While the above process takes place over the long term, it is not a smooth one-way street.

Let us move on to the second way of doing business, like investing. In the shorter term, stock prices see massive gyrations depending on how excited or disinterested the public is about stocks.

Due to this, stock prices sometimes exceed the company's underlying fair value and, at times, are much lower.

As a result, it is often possible to buy a company's stock when it is undervalued in the market and sell it when it reaches fair value.

In this case, you are trying to profit from the market's undervaluation of the business rather than a rise in its fair value on account of growth in revenues and profits.

In today’s article, we’ll look at five such microcap stocks that fall under this category.

These microcap companies are trading significantly lower compared to their original book value and their 5-year average historical valuations as well. Take a look…

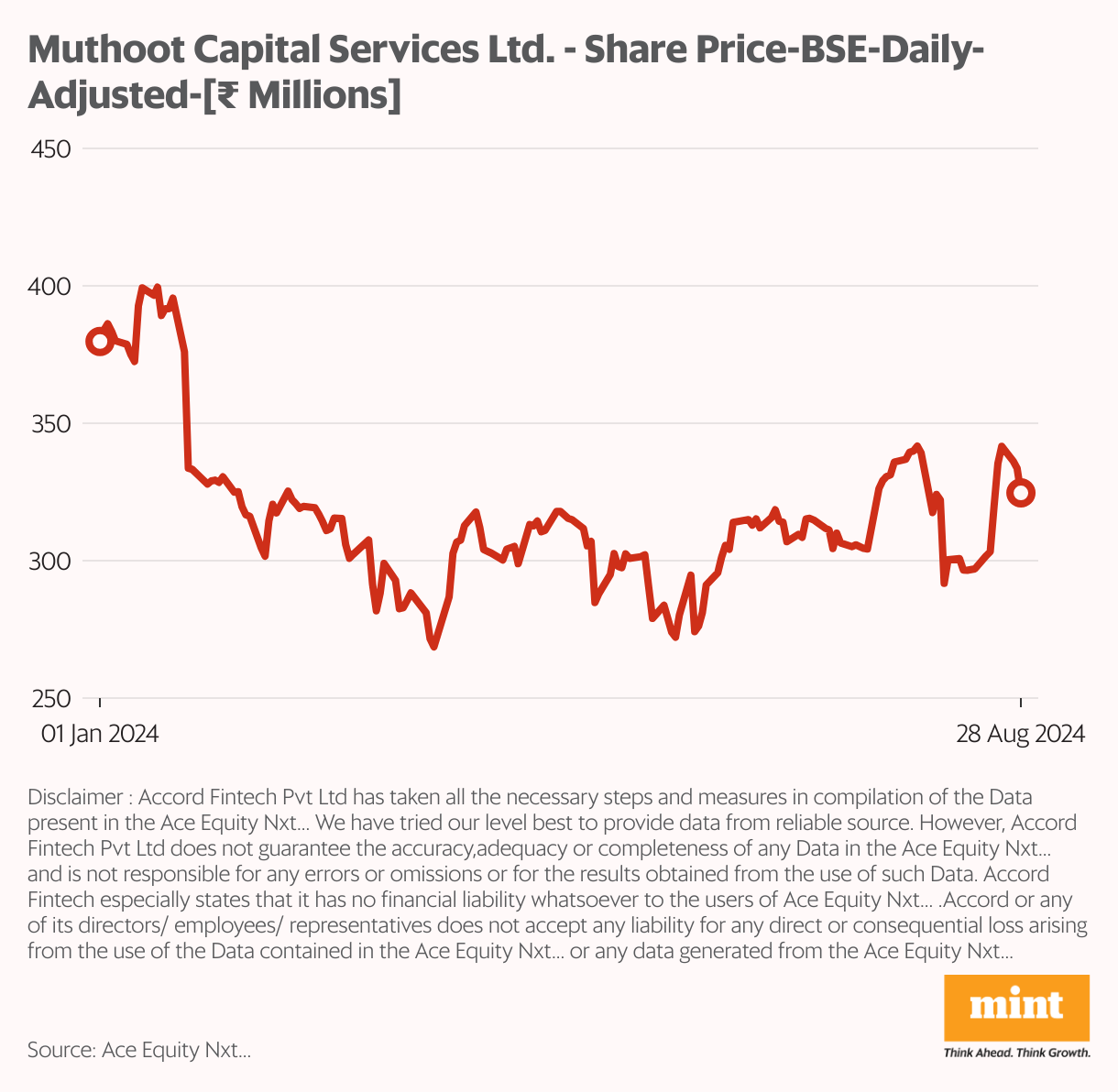

#1 Muthoot Capital

Incorporated in 1994, Muthoot Capital is a deposit-taking, systemically important non-banking financial company (NBFC).

Initially, it provided gold loans, but subsequently, as the group scaled up its gold financing business in Muthoot Finance, Muthoot Capital entered the two-wheeler financing segment in fiscal 1998 and gradually exited the gold loan business.

During the pandemic, the company faced various challenges, and even posted a loss in FY22.

But since then, it’s been in a clean-up mode. The company sold its portfolio (which was affected due to the pandemic) worth ₹240 crore to ARC.

The company is now on a growth trajectory with average monthly disbursements of ₹120 crore during FY24 against ₹110 crore during FY23, and ₹96 crore during FY22.

The company's latest credit ratings report also highlights the significant changes it has made in its collections mechanism by enforcing strong follow-up right from softer delinquency buckets.

Despite all this, the company's valuations are still reasonable. It is currently trading at adiscount to its book value, a discount of almost 10%, to be precise.

Muthoot Capital’s 10-year median P/BV multiple stands at 1.5x. At the current price of ₹332, Muthoot Capital trades at a P/BV multiple of 0.9x.

In 2024 so far, shares of the company have fallen around 15%.

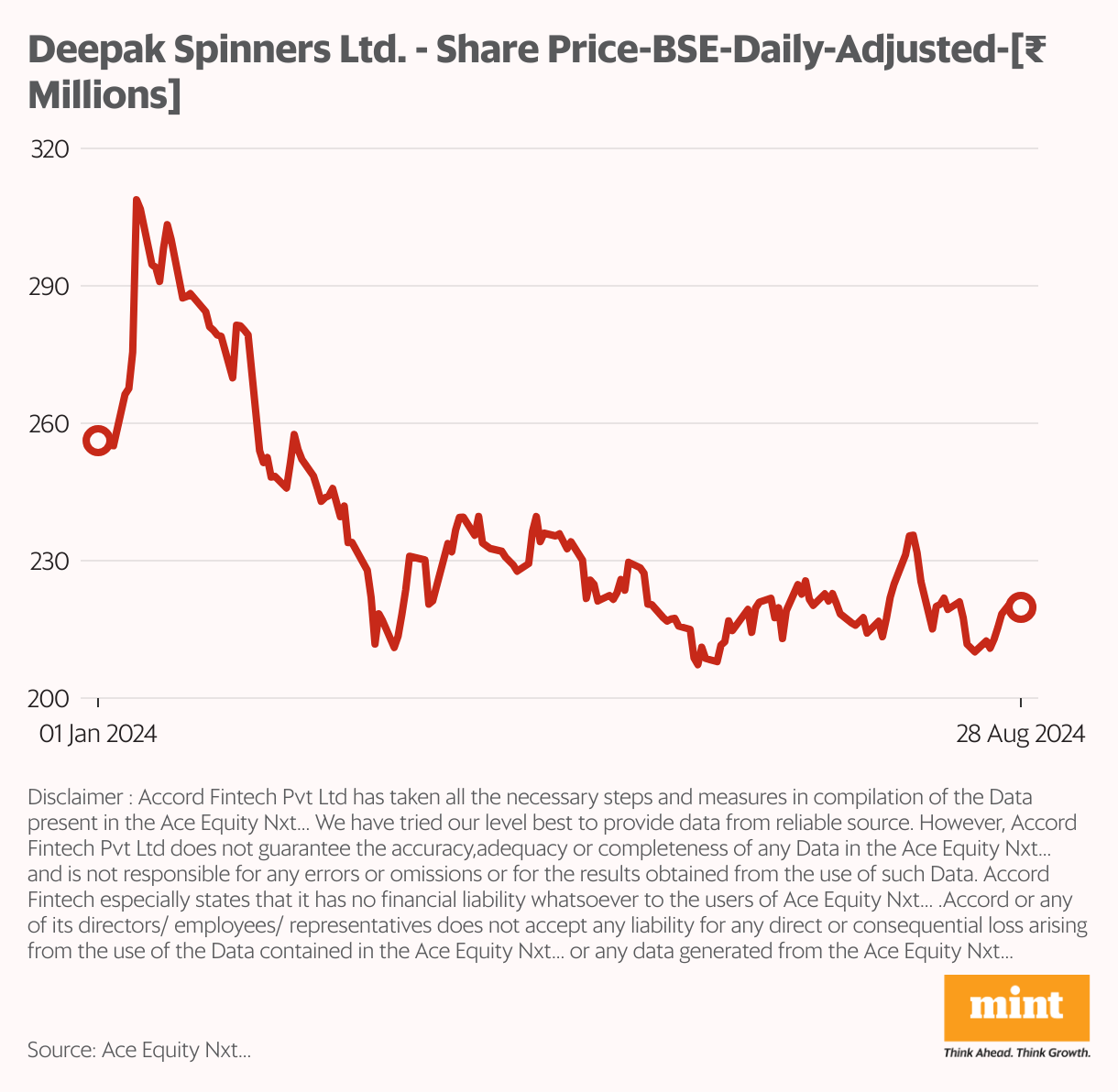

#2 Deepak Spinners

The company manufactures and distributes synthetic and blended yarn. Its product portfolio includes polyester, acrylic, viscose, polyester viscose blends, polyester acrylic blends, and among others.

Located in Chandigarh, Deepak Spinners is a well-established name in the textile industry. Under the leadership of its Chairman, Mr. P. K. Daga, the company has evolved into a leading manufacturer of dyed synthetic yarn.

In recent quarters, the company’s performance has slowed down due to an adverse demand-supply situation in the synthetic yarns industry.

This has resulted in the company posting losses in three consecutive quarters.

Nevertheless, it has strong growth prospects. Deepak Spinners is banking on demand outlook for MMF yarns to improve going forward as people opt for sportswear, performance wear and athleisure.

Since the company sells its products mainly through dealers and agents, it has established good relationships with customers, which helps it obtain repeat orders.

At the current price of ₹222, Deepak Spinners trades at a P/BV multiple of 0.67x, a 30% discount compared to its book value. It’s also below the 5-year median average P/BV of 0.75x. In 2024, so far, shares of the company have fallen 14%.

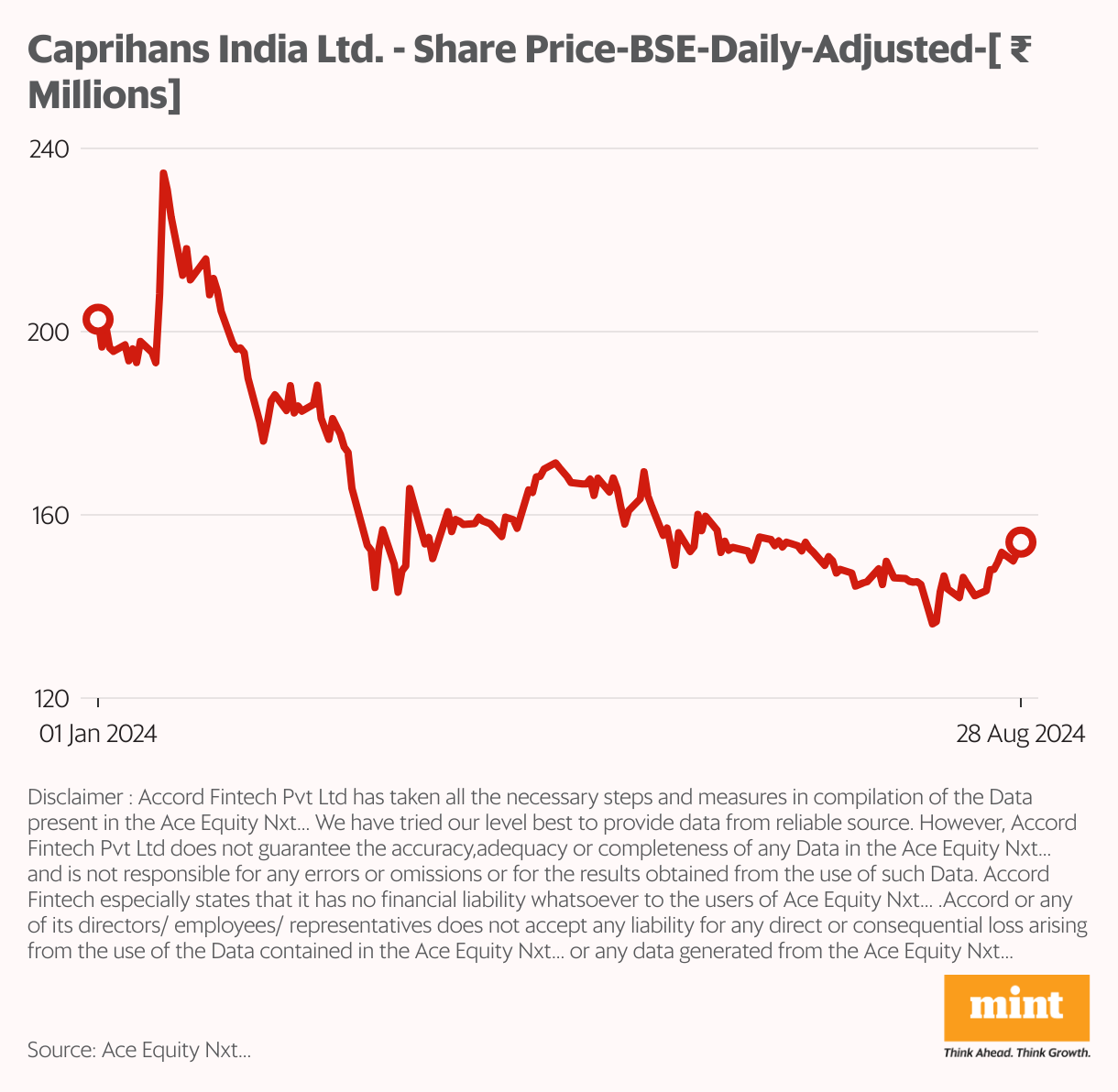

#3 Caprihans

Caprihans India is engaged in the business of manufacturing rigid and flexible PVC films, coated films and plastic extruded products.

It was incorporated as a privately held company in April 1946 and was then listed on the Bombay Stock Exchange in 1976.

The company is among the prominent players in rigid packaging. It has two manufacturing facilities in Thane and Nasik.

Caprihans has been in the business of flexible PVC products since 1957. It has a well-established track record of around six decades in the packaging industry.

The company’s performance has been impacted in recent years. It has received a lot of backlashes for the acquisition of PPI unit from its holding company. After the acquisition, the company went from a zero-debt company to a highly leveraged one.

The company took over the liabilities of Bilcare worth ₹620 crore. This was done so that Caprihans could meet its base film requirement from the acquired unit and not rely on imports.

Nevertheless, the company is hopeful of turning a corner as the sectoral outlook improves.

The company may also show improvement in the coming quarters owing to the backward integration kicking off and Caprihans benefitting from the cost savings therein.

In terms of valuations, the stock is trading at a 60% discount on its book value.

Compared to its 5-year average P/BV of 0.6x, Caprihans trades at a P/BV multiple of 0.4x at the current price of ₹155. So far in 2024, the company's shares have fallen 24%.

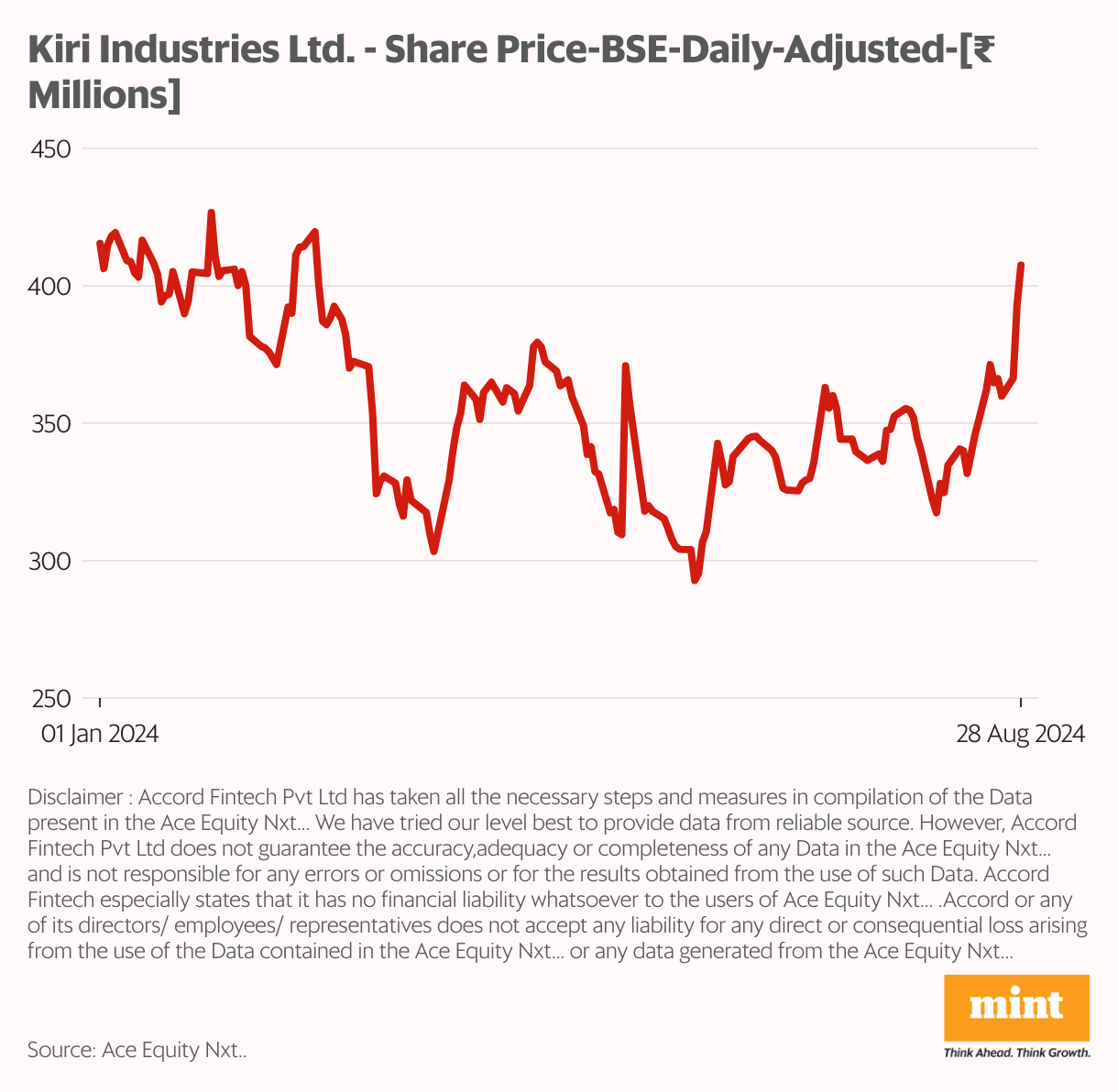

#4 Kiri Industries

Based out of Gujarat,Kiri is one of the largest manufacturers and exporters of a wide range of dyes, dye intermediates and basic chemicals from India.

The company is a certified key business partner with world's top dyestuff majors across Asia Pacific, the EU and the USA.

It provides products and services across the whole value chain in numerous industrial sectors including apparel, hosiery, automotive, carpets, leather, paper, home upholstery, industrial fabrics, among others.

The company has a manufacturing facility at Padra (Baroda, Gujarat).

After posting a loss in the last quarter of FY24, the company started FY25 on a good note by quickly turning around. It reported consolidated revenue of ₹270 crore, a 17% YoY growth.

While net profit came in at ₹78.2 crore, primarily due to the share of profit from DyStar amounting to ₹80.5 crore.

A big overhang for Kiri has been the legal proceedings for its DyStar case. Recently, the Singapore International Commercial Court (SICC) ordered an en bloc sale of DyStar without a reserve price, with a long-stop date set for December 2025.

Kiri Industries is set to receive $603.8 million in priority from this sale proceeds.

To diversify from core operations, the company is exploring investment options in renewable energy sector.

It’s also looking to wade into the electric vehicle (EV) sectors, and fertilizers, reflecting a strategic shift towards high growth.

For all this, Kiri has planned a massive capex of ₹5,000 crore.

Kiri Industries, at the current price of ₹410, trades at a P/BV multiple of 0.8x, a discount of 20% and in line with its 5-year average of 0.8x. In 2024 so far, shares of Kiri Industries have fallen 2%.

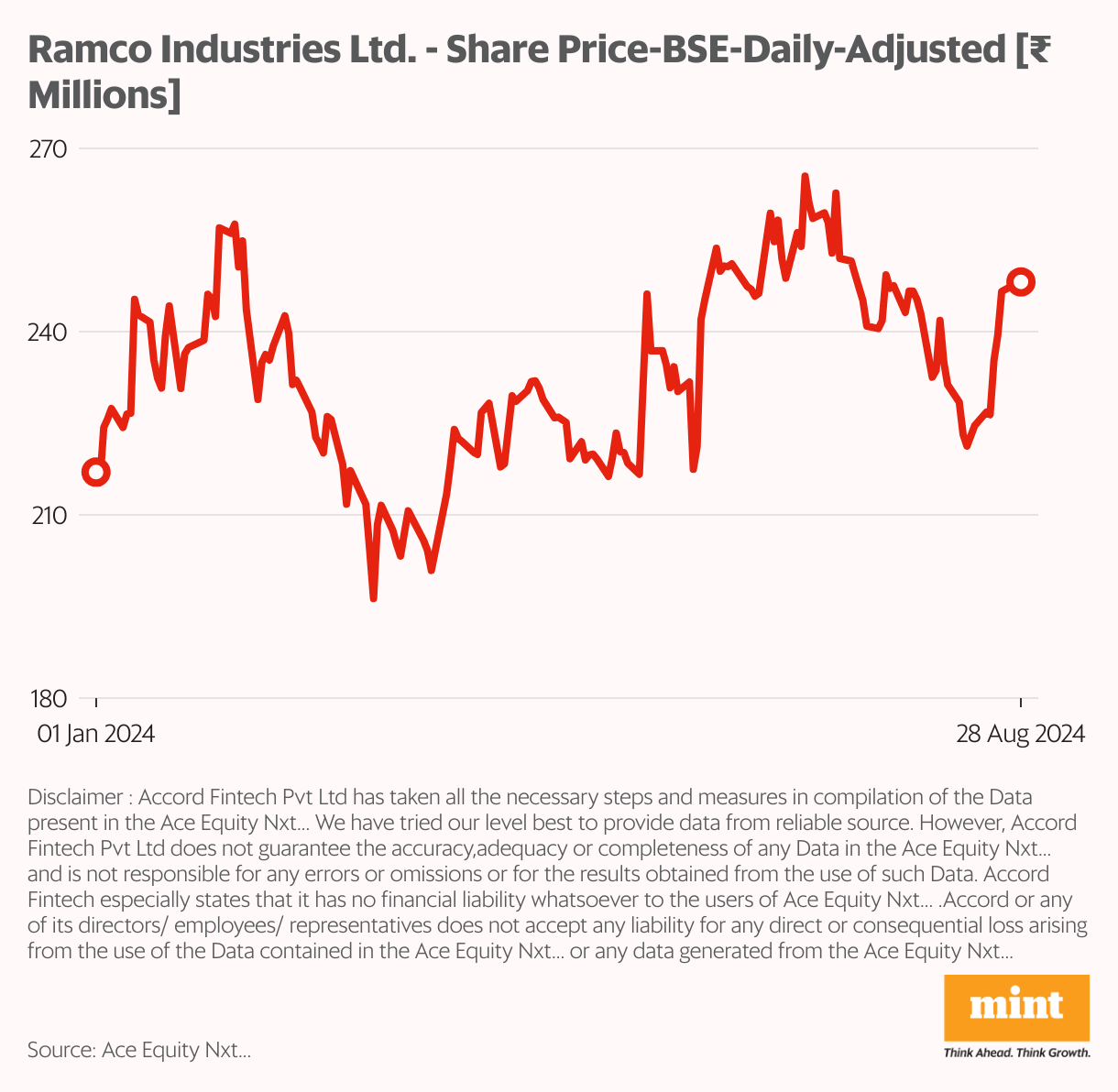

#5 Ramco Industries

Part of the Chennai-based Ramco Group, Ramco Industries is engaged in the manufacture of fiber cement (FC) sheets and calcium silicate boards (CSBs).

It is also engaged in the spinning of cotton yarn, sale of surplus electricity generated from its windmills and computer software.

In FY23, the company’s operating performance was impacted largely due to increase in raw material prices and global challenges.

However, as input costs started to come down, the company marked an improvement. The company’s sales and profit have seen decent growth in the past three quarters.

As part of its diversification efforts, the company has entered the non-asbestos based roofing products while it also has a presence in the Sri Lankan market.

The company recently postponed its capex plans to the latter part of FY25 owing to uncertain market conditions.

Coming to its valuations, Ramco Industries trades at a P/BV multiple of 0.53x, a discount of almost 50% from its book value.

The median average P/BV multiple for Ramco has remained in the range of 0.5x-0.6x.

In 2024 so far, shares of the company have moved up by 15%.

In Conclusion

These were just a few examples of beaten down, fallen out of the favor stocks that look undervalued right now on a price to book value basis.

Before you go about investing in any stock, it is important to do your own research and understand the risks involved.

No matter how great the prospects, you must consider your risk-bearing capacity and investment horizon.

Happy Investing.

Disclaimer:This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com