A little-known stock that quietly delivered 15,000% returns—and still has room to run

")

Consistent profitability and capital efficiency helped this small manufacturer quietly outperform the market.

What makes a stock truly stand out for long-term investors? Strong returns on invested capital, capable management, consistent profitability, and meaningful wealth creation for shareholders.

In this article, we spotlight a company that has quietly hit the sweet spot for nearly a decade. It has delivered consistent annual growth, remained profitable throughout, generated exceptional returns on every rupee of capital deployed, and rewarded its investors with a staggering 15,000% gain over the past five years.

The kicker? Even after this run, the stock is still trading at a discount.

Shilchar Technologies Ltd: A consistent compounder

With a market cap of ₹6,029 crore, Shilchar is a technology manufacturer focused on two broad verticals: electronics and telecom, and power and distribution transformers. Recently, it has also expanded into producing ferrite transformers.

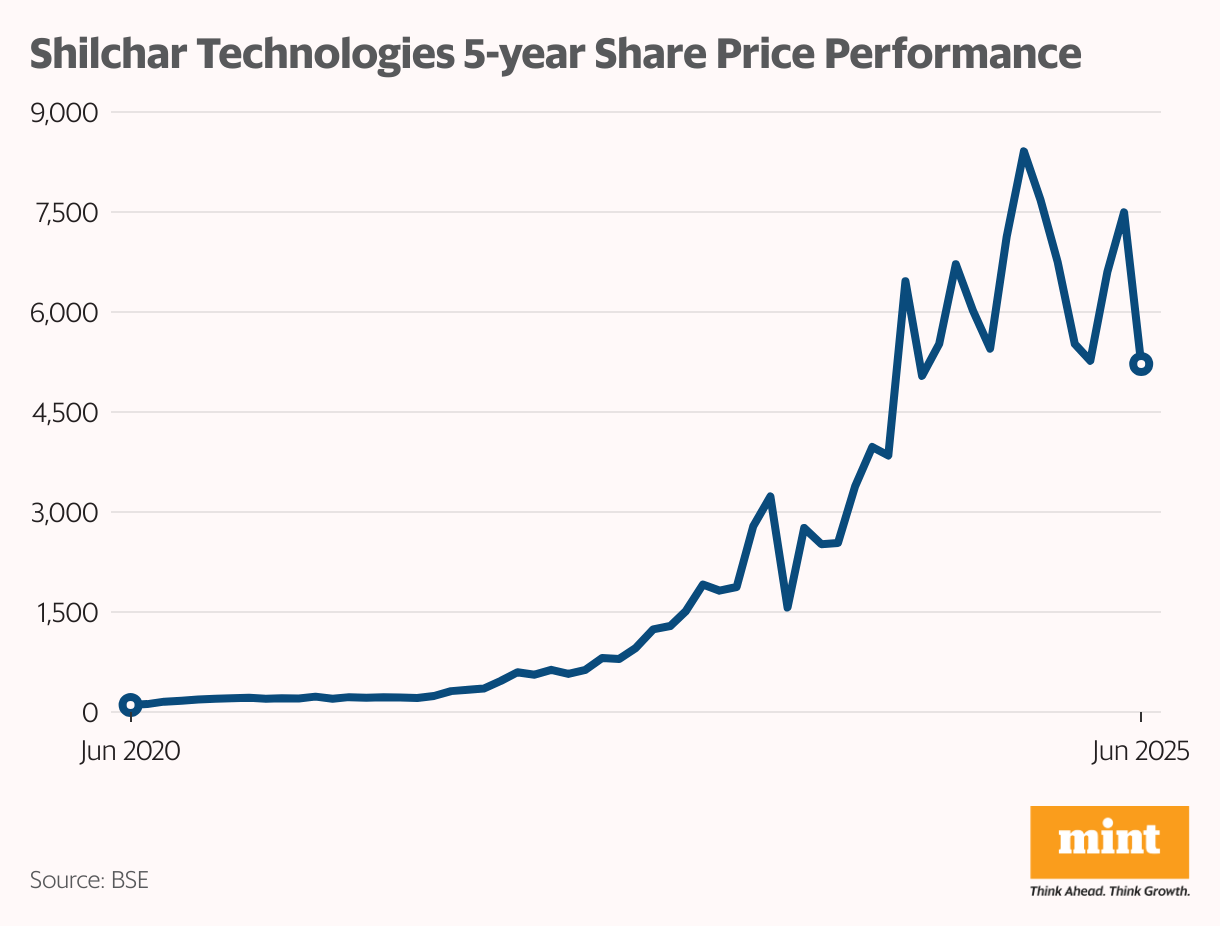

The stock’s performance over the last five years has been nothing short of spectacular. From ₹35 per share in June 2020 to ₹5,220 as of 23 June 2025, Shilchar has delivered an almost unbelievable 15,000% return.

To put it in perspective, ₹1 lakh invested five years ago would be worth around ₹1.5 crore today, excluding the impact of a recent 2:1 stock split and any other bonuses or splits along the way, which would push that figure even higher.

In FY25, the company reported a 61% year-on-year increase in earnings per share, jumping from ₹80 to ₹129. But this is just one part of a much deeper story.

The Secret: Shilchar’s ‘Circle of Wealth’

At first glance, Shilchar’s business may seem straightforward—it generates revenue entirely from its transformer segment, manufacturing power transformers, distribution transformers, inverter duty transformers for solar, generator transformers for wind, hydro transformers, and furnace transformers.

But behind this seemingly narrow business lies what can be called Shilchar’s Circle of Wealth—a self-sustaining cycle that quietly powers its growth.

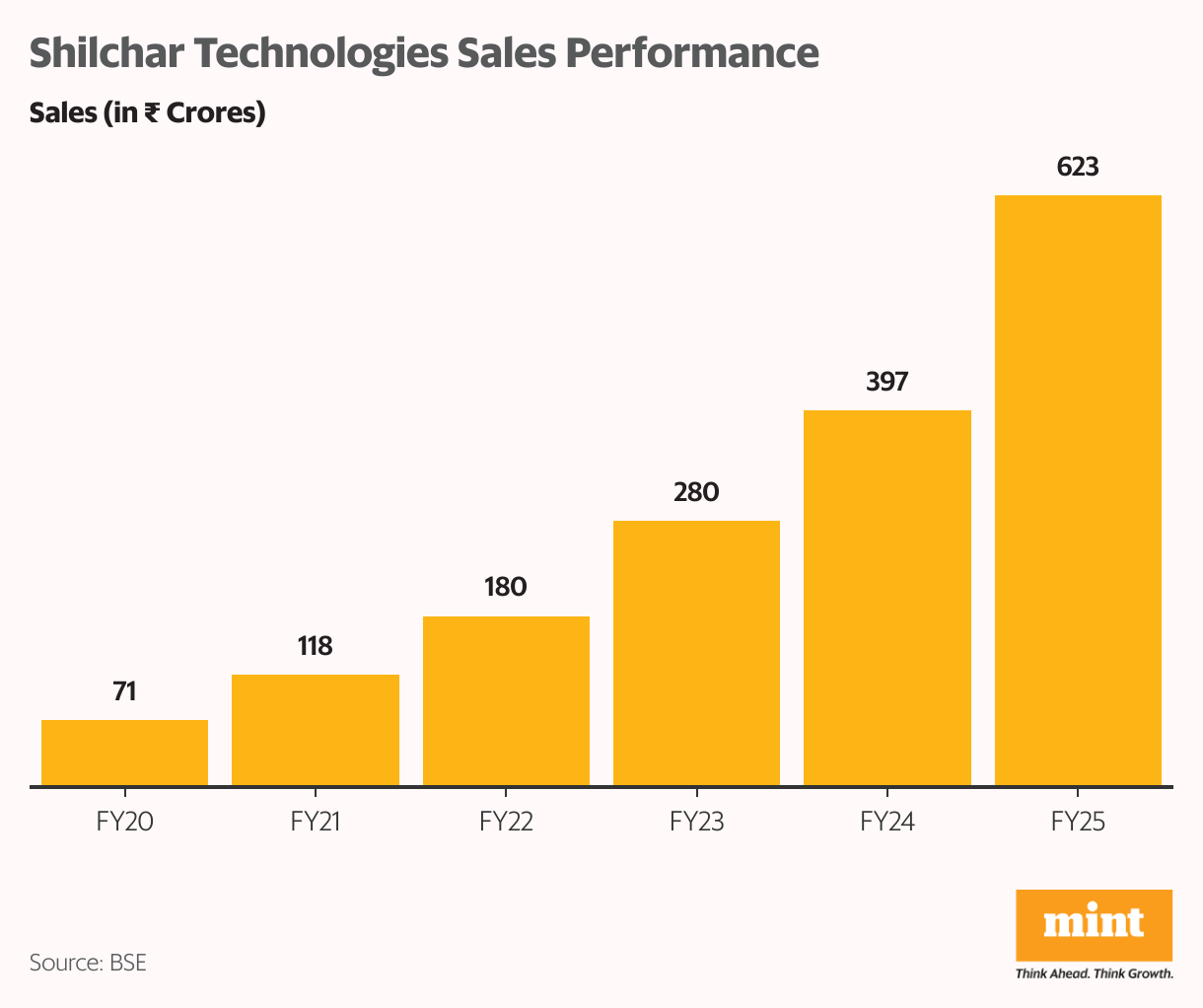

Take sales, for instance. Even with this single product segment, Shilchar’s revenue has been on a steady upward trend over the past five financial years, compounding at an impressive 54%. This sharp rise in sales has been driven largely by exports, which climbed from 19% of total revenue in FY21 to 56% in FY22, before settling at 43% in FY25.

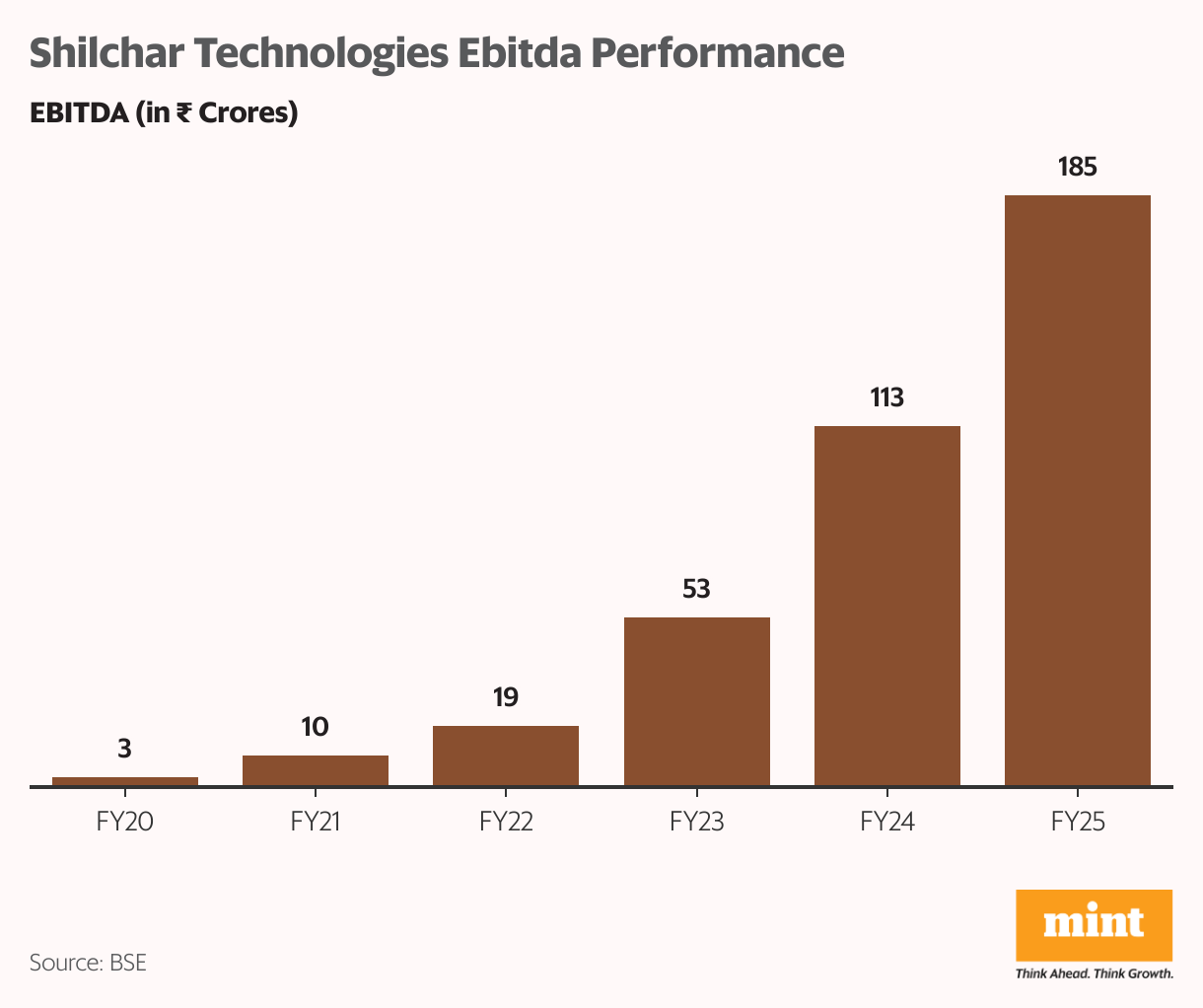

Strong sales have naturally translated into rising operating profits. Shilchar’s Ebitda (Earnings Before Interest, Taxes, Depreciation, and Amortization) has grown at a remarkable compounded rate of 128% between FY20 and FY25.

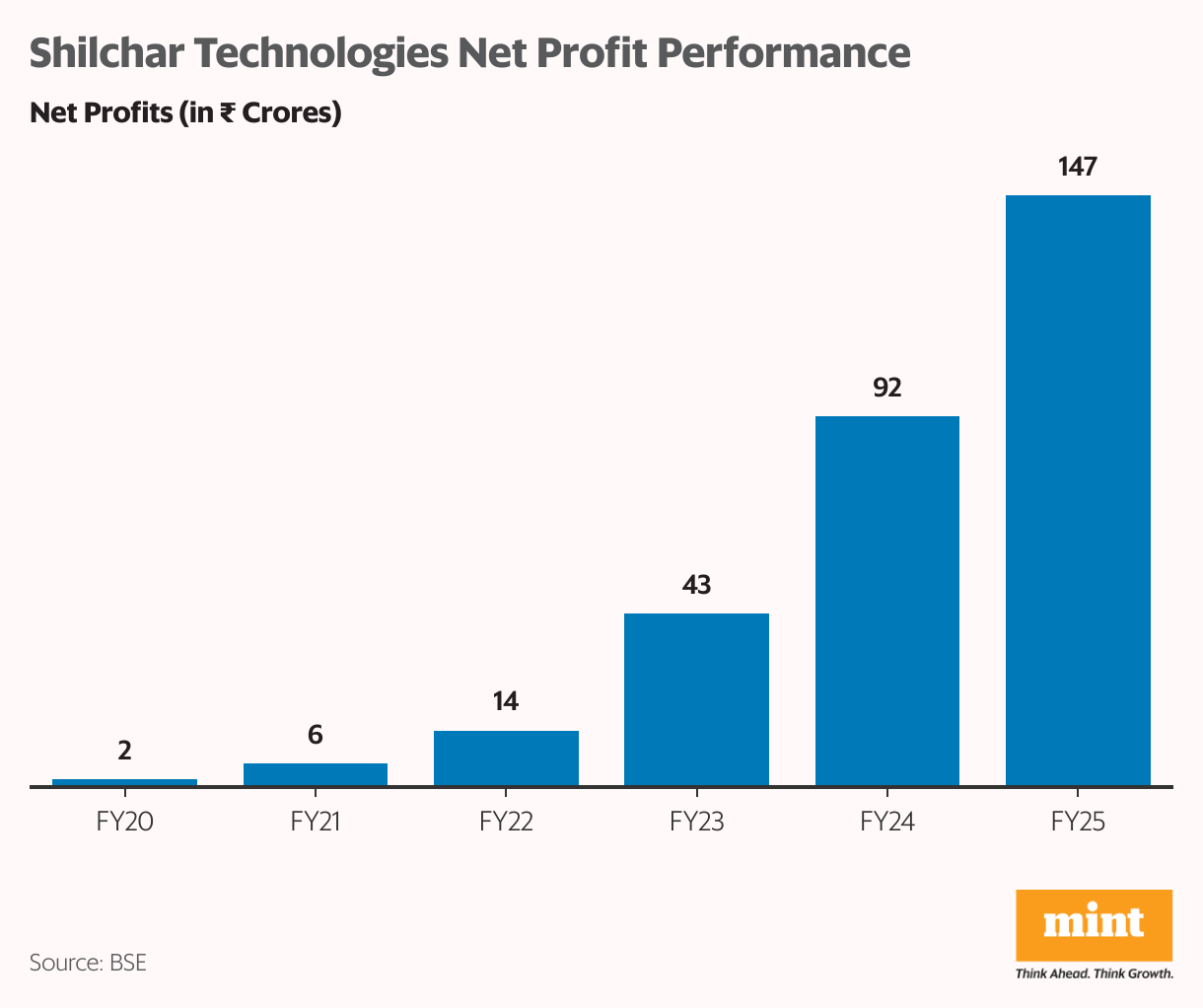

And strong operating profits have led to surging net profits. Over the past five financial years, net profit has compounded at a substantial 151%. The company has remained consistently profitable for more than a decade.

With robust sales and profits in place, management’s capital discipline has further strengthened this growth cycle. Shilchar’s Return on Capital Employed (ROCE) currently stands at an impressive 71%—one of the highest among industry peers.

Put simply, for every ₹100 invested, the company generates ₹71 in profit. These profits are then reinvested to grow the business further, pay down any obligations, or reward shareholders through dividends.

Efficient capital use has allowed Shilchar to eliminate debt entirely. While being debt-free reduces financial risk and preserves shareholder value, it also means the company relies entirely on internal accruals for expansion, which could limit large-scale growth in the future.

In short: zero debt, consistently rising sales, soaring profits, and industry-leading capital efficiency—all of it has combined to drive Shilchar’s extraordinary 15,000% share price surge over the past five years.

Operational excellence meets profitability

Shilchar also boasts a high Return on Equity (ROE) of 53%, meaning that for every ₹100 of equity invested by shareholders, the company generates ₹53 in profit. A strong ROE signals management’s efficiency in deploying capital and enhances the prospects of strong shareholder returns.

Over the past five years, Shilchar has maintained a consistent average ROE of 44%—a level widely seen as a hallmark of financial strength and prudent management, suggesting the company is consistently creating significant value for its shareholders.

The company has steadily expanded its asset base as well, with fixed assets growing from ₹39 crore in FY20 to ₹59 crore in FY25, indicating a continued commitment to capital expenditure and capacity expansion.

Shilchar’s debt-free status, combined with its strong profitability, suggests that these expansions are being funded entirely through internal accruals. In addition, the board’s recent recommendation of a 1:2 bonus issue reflects a strategy to broaden the equity base without resorting to external borrowing, likely to support future capacity enhancements.

In terms of valuation, the stock is currently trading at a price-to-earnings (PE) ratio of 41x, close to the current industry median of 44x. However, Shilchar’s own 10-year median PE stands at 16x, compared to the industry’s 10-year median of 28x—indicating that the stock has seen significant re-rating over the years.

As of April 2025, the company’s order book remains robust at over ₹400 crore. Shilchar is also exploring entry into higher MVA/kV class transformers as part of its expansion plans.

In short, nearly every indicator seems to be working in the company’s favour. But as always, risks remain.

Sustainable, unbroken growth?

While the headline numbers may look highly attractive, every company carries its own set of risks—and Shilchar Technologies is no exception. One area of concern is receivables management. The company’s debtor days increased from 86 in FY24 to 134 in FY25, indicating slower collection of payments, which could create liquidity pressures if not addressed promptly.

Working capital days have also stretched significantly—from 77 days in FY24 to 144 days in FY25—meaning the company is taking much longer to convert its working capital into revenue, further raising potential liquidity concerns.

In addition, with approximately 44% of its revenue coming from exports, Shilchar remains exposed to currency fluctuations and geopolitical risks that could impact profitability if global conditions turn unfavourable.

Another potential red flag for some investors is the company’s low dividend yield of 0.16% and a payout ratio of just 9%. Despite strong profit growth and a debt-free balance sheet, such modest payouts may deter certain income-focused investors.

Yet, there are compelling positives as well. In Shilchar’s latest investor presentation, chairman and managing director Ajay Shah said, “We have achieved full capacity utilisation ahead of schedule, as demonstrated by our strong Q4 performance. Initially, we anticipated reaching this milestone by FY26; however, on a run-rate basis, we accomplished it in Q4 itself. Further, Q4 being a strong quarter on account of financial year end, we have been able to do well in our domestic business. Consequently, this has led to a slight shift in our business mix, favouring the domestic segment for FY25."

The same presentation notes that, based on this year’s performance, the board has recommended a final dividend of ₹12.5 per equity share, subject to shareholder approval, along with a 1:2 bonus issue.

Overall, supported by strong profitability, healthy gross and operating margins, and its highest-ever quarterly and annual profits, Shilchar appears well-positioned for sustained growth. Its growing focus on renewable energy transformers and exports, combined with government-led grid modernization initiatives, further strengthens its long-term prospects.

Conclusion

Shilchar Technologies has delivered strong performance across every key metric—sales growth, operating profits, and net income—while maintaining exceptional capital efficiency, reflected in its 71% Return on Capital Employed. Backed by a healthy order book and management’s confidence in its expansion plans, the company offers a compelling proposition for investors.

That said, these strengths do not come without risks. As always, past performance is no guarantee of future results. In a global environment marked by uncertainty—from tariff wars to cold wars to actual wars—investors must remain vigilant, especially given Shilchar’s significant reliance on exports.

How Shilchar Technologies navigates the near and long term will be closely watched. For now, though, the stock is trading at a 15% discount from its all-time high, making it an intriguing name to track.

Suhel Khan is an equity market enthusiast with 10+ years of experience in reading and analysing Indian financial markets. Former Head of Sales & Marketing at a leading Mumbai-based equity research firm, he has a knack of finding stocks running under the radar. He now dedicates his time studying and writing about a range of stocks from the biggest bluechip to the almost unknown ones.

Note: We have relied on data from www.Screener.in, www.trendlyne.com, and www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclosure: The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.