NLC India misses lignite target, but recovery plan sparks comeback hopes

")

- If execution remains on track, FY25 could mark a significant recovery for NLC India and set the stage for sustained growth.

NLC India has recently been in the news after a parliamentary standing committee on coal, mines, and steel stated in its report that the company failed to meet its lignite production target for FY24.

The report said the company produced 23.68 million tonnes (mt) of lignite against a production target of 26.5 mt, achieving only 83.36% of the target.

Of the three coal-producing public sector undertakings (PSUs), the company was the only one that did not meet its target.

Note that 23.68 mt is 78.9% of NLC’s lignite mining capacity. NLC India has a total mining capacity of 50 million tonnes per annum (mtpa), with 30 mtpa for lignite and 20 mtpa for coal.

The average plant availability for NLC’s portfolio also remained below the normative level of 85% in FY24.

The company failed to meet its lignite production target in FY24 due to prolonged delays in land acquisition at its thermal power station–II (TPS-II) plant.

Revenue from lignite sales also decreased as a result because there were no open sales in Mine IA. Mine IA supplies lignite to the TPS-II plant.

Land acquisition issues are not new to NLC. In 2023, areas near NLC's opencast mines in Cuddalore district of Tamil Nadu were a hotbed of protests over the company’s decision to take control of the lands acquired more than a decade ago.

Acquiring land for large-scale mining projects is a significant challenge due to complex land ownership patterns and compensation negotiations. Any delay, however, can disrupt and hamper a company’s operations.

This can be seen in the company’s numbers for FY24. Its revenue declined by 19.6% year-on-year to ₹12,999 crore from ₹16,165 crore in FY23.

While the decline in revenue was largely due to a decrease in the sale of power and the absence of many favourable regulatory/tariff orders that had boosted revenue in FY23, the drop in lignite production was also a major contributor.

Also Read: Bajaj Finserv’s insurance bet fails to impress investors

No lignite shortage anymore

The company’s management has said that it has resolved the aforementioned issues by working with the Centre and the Tamil Nadu government.

In its recent conference call, the management said that it does not foresee any issues with the availability of lignite in the near future.

All of the company’s units are operating at their full capacity, and with a substantial amount of land in the company’s possession, it doesn’t foresee any problem in the next financial year either.

It has already taken short-term and long-term measures to improve the availability and reliability of its TPS II expansion units.

The short-term measures have already resulted in an improvement in the availability and reliability of its units. Long-term modification in one of the units is expected to be completed in the second week of March. The unit will start its operation with improved reliability and availability.

These changes have already resulted in an improvement in the company’s financials.

For the first nine months of FY25, the company’s revenue has grown 21% YoY to ₹11,445 crores on the back of an increase in sale of power.

Lignite production, too, has increased 5.3% YoY to 171.35 lakh mt, while coal production has risen 40% to 82.19 lakh mt. This is the highest-ever lignite plus coal production reported by the company.

Tracking this increase, the company’s net profit has grown 28% YoY to ₹2,245 crores.

Expansion plans to fuel growth

While the company saw a few setbacks concerning lignite production in FY24, its outlook for the near future seems promising.

By 2030, the company plans to increase mining capacity to 102 mtpa from the current 50.1 mtpa.

It also plans to increase its renewable capacity to 10 GW by 2030, up from the current 1.4 GW. Ongoing projects include 300 MW in Barsingsar, 600 MW in Khavda, and 810 MW in Rajasthan.

It is exploring various avenues for renewable capacity addition, including joint ventures with multiple state governments.

The company recently bagged a contract from SJVN Ltd to develop and operate a 200 MW wind power project. The project is set to generate 526 MU of clean green power each year offsetting an equivalent amount of greenhouse gas emissions.

Concerning the mining business, the company is in the advanced stage of getting the stage 2 forest clearances for the Pachwara Coal block linked to the Ghatampur plant and expects to start production by July 25.

It has also signed a coal mine development and production agreement for the New Patrapara South Coal Mine project, which has an annual capacity of 12 mtpa, bringing the total group capacity to 100 mtpa.

These capacity expansions are estimated to be over ₹1.25 trillion, which the company will fund through debt and equity as per regulations.

The management is confident of funding the equity from the additional revenue as the expansion projects start contributing to the top line.

NLC is also in the process of transferring all its existing renewable assets to NLC India Renewables Ltd, and all the new renewable energy capacity will be moved to NLC India Green Energy.

It expects to proceed with its green energy IPO by March 2026 or June 2026.

Also Read: As the weight of promoter pledge lifts, Aster DM is free to grow again

What the numbers say

Over the last five years, NLC India’s revenue has grown at a meagre CAGR (compounded annual growth rate) of 6%, and net profit has grown at 4%.

While the increase was driven by a rise in blended power tariffs and a new revenue stream from the external sale of coal from Talabira mines, issues related to the TPS-I and TPS-II plants weighed on the company’s performance.

Going forward, this is expected to improve as the company increases the production of thermal coal via its Ghatampur plant and Talabira Mines.

However, any delay in the execution of these projects and ramp up in lignite and coal production could slow down this growth, as highlighted by analysts at Axis Direct.

A delay in the ramp-up of renewable power generation capacity and recovery of dues from the state distribution companies (discoms) could also hinder performance, they added.

Nevertheless, if these projects are executed as per the company's plans, operating profit margins (OPM) are expected to improve from 27% as reported in FY24.

Operating profit margins (OPM) are also expected to improve from 27% as reported in FY24.

Historically, the company has maintained an OPM of more than 25%. Its average five-year operating profit margin (OPM) stands at 32%.

Coming to financial ratios, the return on equity and return on capital employed of the company have been in the range of 8-12% in the last five years on account of lower revenues. Going ahead, this could continue to be stable as revenue increases.

With respect to leverage metrics, the company’s debt-to-equity ratio has come down from 2.1x in FY20 to 1.35x in FY24, indicating a strong financial position.

Its interest coverage ratio also increased from 3x to 4.39x over the same period, suggesting that the company is more than capable of meeting its financial obligations.

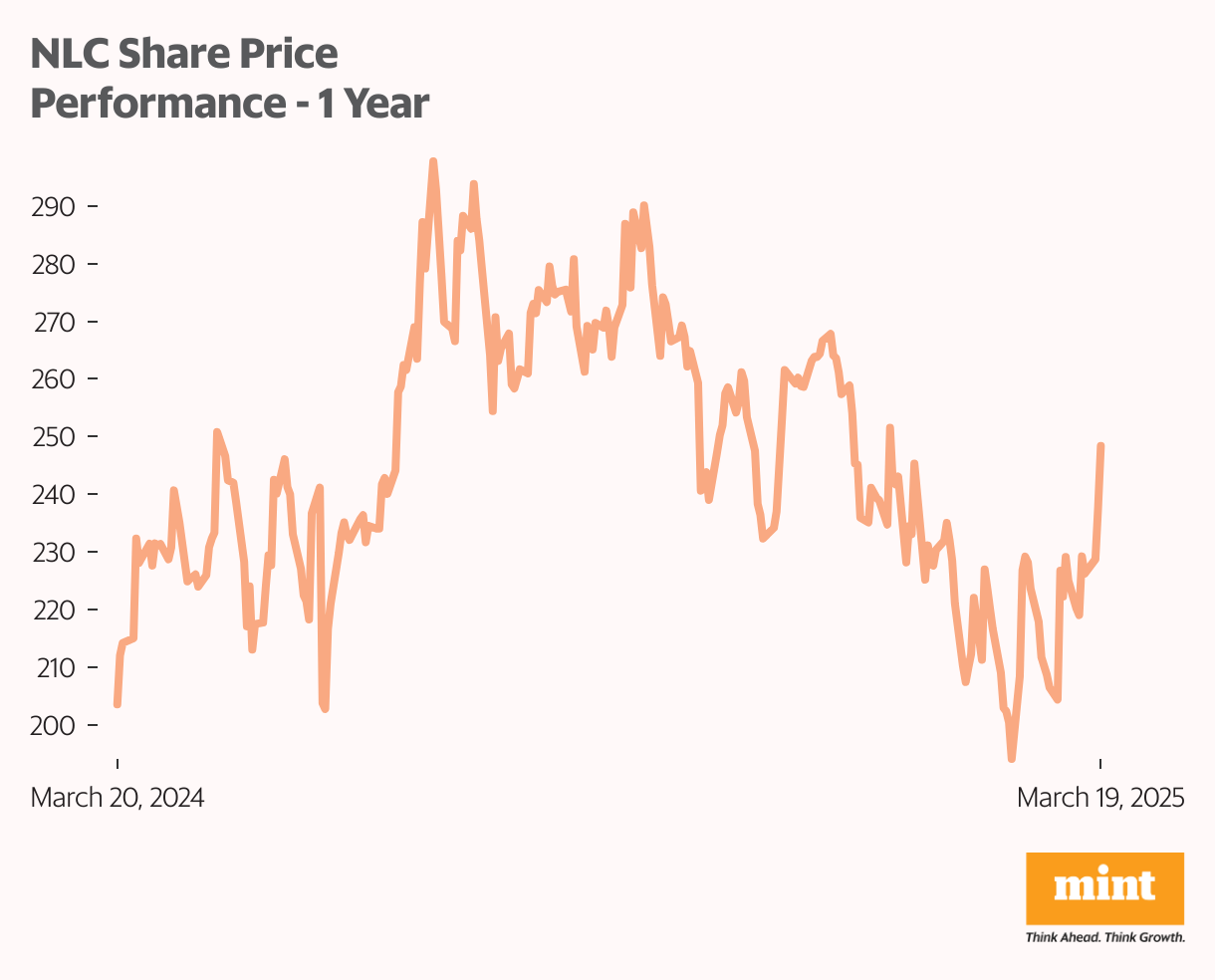

The company’s shares are down almost 20% from their all-time high. However, the stock has gained 4% in 2025 so far and over 18% over the last year.

Shares of the company hit their 52-week high of ₹311.65 on 16 July 2024 and 52-week low of ₹185.85 on 17 February 2025.

Axis Direct maintains a ‘buy’ rating on the stock with a target price of ₹305. This implies a 21% upside from the current price.

The stock has seen major interest from FIIs and DIIs over the last few quarters. FIIs have increased their stake from 2.18% in June 2024 to 2.86% in December 2024, whereas DIIs have increased their stake from 8.85% in December 2023 to 14.46%. Both are a sign of increasing confidence in the company.

Also Read: LG India’s IPO eyes a premium valuation—will investors bite?

Conclusion

NLC India faced various problems with its lignite production in FY24. However, the business has seen a turnaround in FY25 supported by several measures and resolution of its land acquisition issues.

The company has ambitious growth plans that it plans to see through over the next five years. It also has improving financials to support its growth.

If execution remains on track, FY25 could mark a significant recovery for the company and set the stage for sustained growth.

For more such analyses, read Profit Pulse.

Ayesha Shetty is a SEBI- registered research analyst. She holds the Financial Risk Manager (FRM) charter and is also pursuing the Chartered Financial Analyst (CFA) designation.

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.