Markets

Markets

Investors are excited about NTPC Green’s IPO, but experts advise caution

Summary

- The Street is enthusiastic about renewable energy right now, as evidenced by Premier Energies’s listing earlier this month, but experts point to NTPC Green's less-than-stellar track record on executing projects.

The Street is excited about NTPC Green Energy’s recent announcement of an initial public offering (IPO), but industry experts said a better track record on executing projects would have offered investors more comfort.

The equity fund manager of a large mutual fund house, who did not wish to be named, told Mint, “Right now, NTPC Green is this large public entity which plans to have 60GW of renewable energy capacity by FY32. It will also start producing green hydrogen and green ammonia in the future. So it is on its way to becoming a one-stop solution for pure-play green energy. But the execution must follow. Their installed capacity should have been higher."

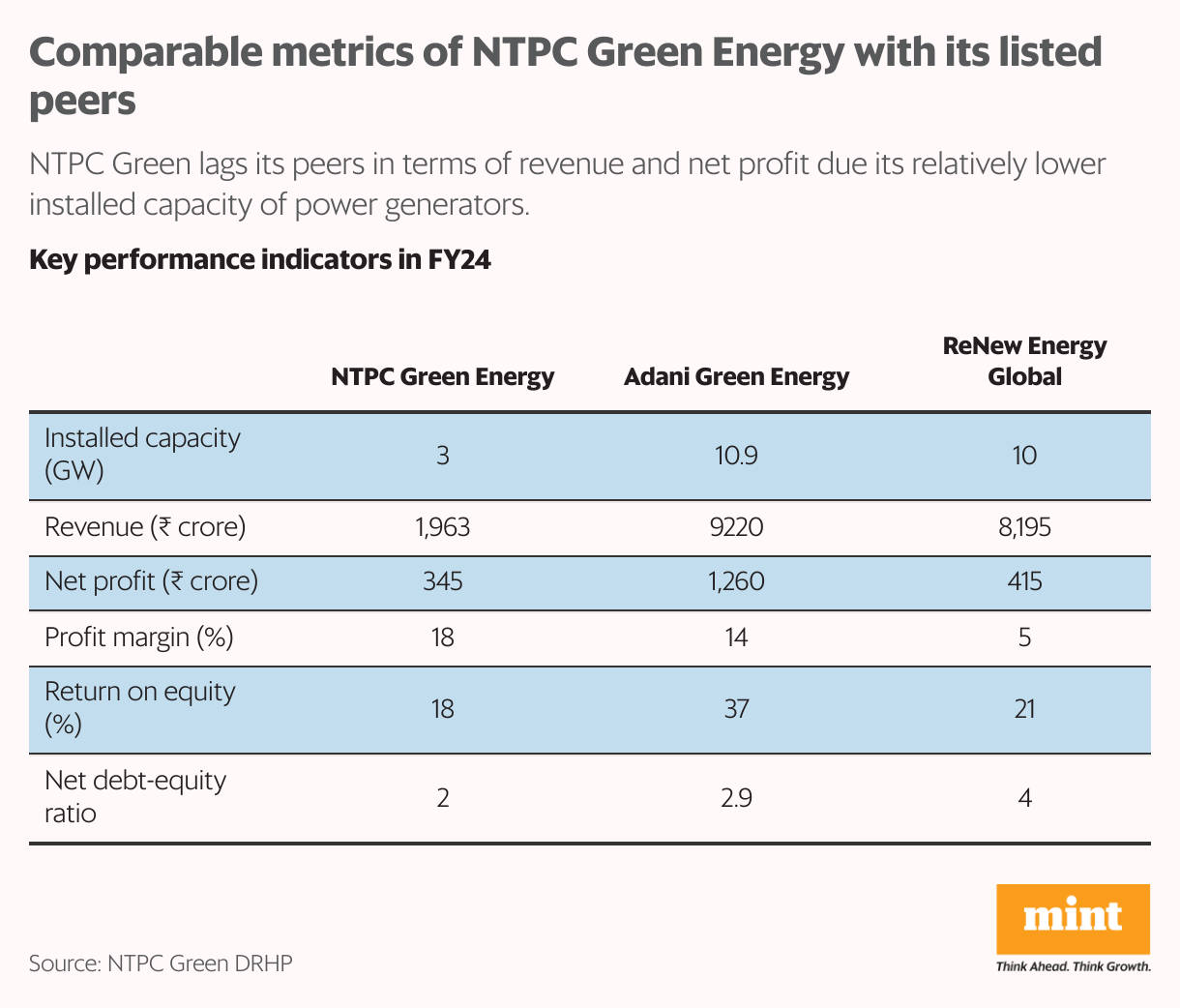

NTPC Green Energy had a modest 2.8GW or so of solar energy capacity and 100MW of wind energy capacity as of June. By comparison, its listed rival Adani Green Energy, which was formed five years before NTPC Green, had a total installed capacity of almost 11GW, including solar, wind and hybrid energy for the same period, according to NTPC Green’s draft red herring prospectus.

A 100% subsidiary of NTPC Ltd, NTPC Green Energy came into existence in 2020. It announced its plan for a ₹10,000-crore public offering on Wednesday amid an IPO frenzy in India. Analysts said the cash infusion from the IPO would significantly aid the company’s capacity expansion plans as the current installed capacity of its power generators does not bring in enough revenue to support its goals.

Also read: NTPC powers ahead with plans for expansion, renewable energy business

However, of the ₹10,000 crore it plans to raise, the company will only use ₹2,500 crore for capital expenditure on new projects. The rest will be used for debt repayment and prepayment, according to the company’s draft red herring prospectus.

“The equity cash infusion will support around 2.5GW of capacity addition following the IPO. They can add 3-4GW of capacity every year, not more," Rupesh Sankhe, vice president of institutional equity research at Elara Capital told Mint. “With 3.1GW of operational capacity, they do not have enough cash flow to go for higher capacity addition than that each year, at least for the next five to six years."

Edge over private competitors

A modest installed capacity has generated lower revenues and profits for NTPC Green relative to its listed peers. However, the company’s revenue and net profit grew by 1,057% and 101% on-year to ₹1,963 crore and ₹345 crore, respectively in FY24, according to its draft red herring prospectus.

Adani Green’s revenue and net profit grew around 19% and 30% on-year to ₹9,220 crore and ₹1,260 crore, respectively during the same period. However, analysts noted that the difference in growth between the two companies was due to the statistical effect of a higher base for Adani Green.

Despite its lower revenue and net profit, NTPC Green has been more profitable than its listed peers. Its profit margin was 18% in FY24, Adani Green’s was 14% and ReNew Energy Global’s was 5%.

Analysts said since NTPC Green is the subsidiary of a ‘Maharatna’ public sector undertaking with sovereign backing, it can raise funds for its projects at a lower cost than its private, listed peers. Moreover, with a debt-to-equity ratio of 1.98, its level of debt is also the lowest among its peers. This helps the company be more profitable and offers a significant competitive edge over others, they said.

Also read: NTPC arm in talks with HPCL, Hindalco for green hydrogen JVs

“In the renewable space it is all about financial engineering – whether you can raise money at a lower cost or not," Sankhe said. “Since 80% of the project cost is usually financed with debt, cost of funding becomes a huge differentiating factor."

Moreover, as a state-owned entity, NTPC Green also has an advantage over others in acquiring land for its projects, industry experts said. “It is easier for NTPC to enter into agreements with state governments to build large solar parks than for its competitors. It can also source its raw materials at a fixed cost through PPAs (power purchase agreements) and bundle its power from different sources for its customers at a cheaper rate," the fund manager quoted above said. “NTPC is an ecosystem, and being its subsidiary turns the game in NTPC Green’s favour."

Betting on renewables

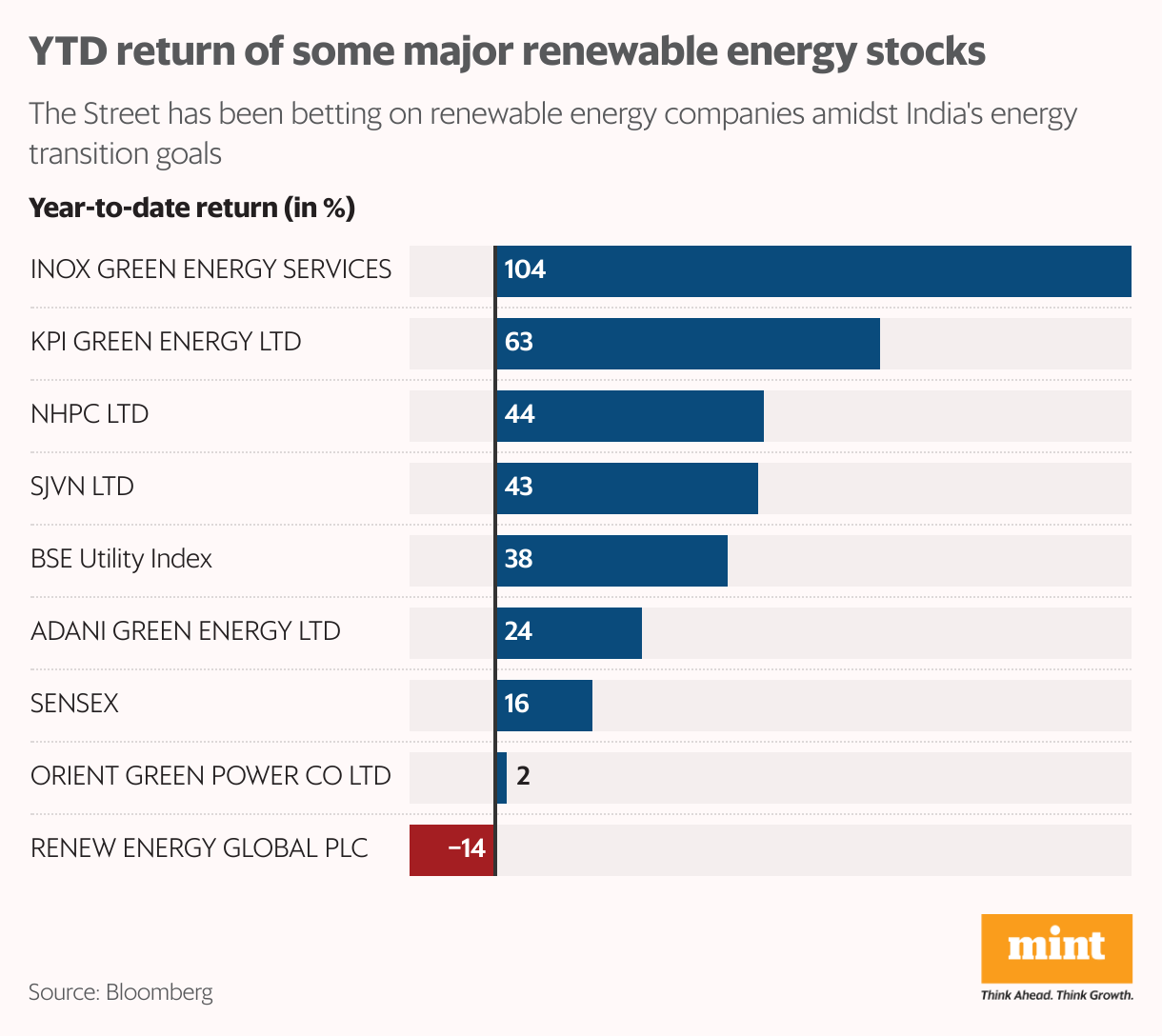

The Street is quite enthusiastic about renewable energy right now, as evidenced by Premier Energies’s listing earlier this month. The domestic solar cell and module manufacturer’s ₹2,830.40 crore IPO was oversubscribed by almost 75 times. It received bids for 332.02 crore shares against the 4.46 crore shares offered.

In this scenario, where incremental liquidity is finding its way into fresh IPOs every week, industry experts expect strong demand for NTPC Green’s stock market debut.

“Investors are very much interested in renewable energy as the entire sector is gaining pace. Right now, we have around 200GW of renewable energy capacity. We still have to reach the 500 GW target," the fund manager quoted above said. “Investors see a long road ahead and they want to get in early. Also, from an ESG (environmental, social and governance) perspective, NTPC Green is a good choice for investors who do not want any exposure to coal."

Also read: NTPC eyes $50 billion capex to transform into a complete energy company

Analysts believe that once India becomes self-sufficient in solar module and cell manufacturing in the next couple of years, it will significantly boost NTPC Green’s pace of project execution and further reduce overall costs for the industry. However, they also remain wary of the fact that NTPC Green currently has no hybrid power generators. Adani Green had around 2.1GW of hybrid energy capacity as of June.

“Moving ahead, more tenders for hybrid power generators will be floated. Those who have hybrid capacities installed are better positioned," Ankit Jain, senior equity fund manager at Mirae Asset Investment Managers (India) told Mint. “The goal is to reduce India’s peak power deficit. Hybrid generators are a reliable source of power, particularly during peak deficit hours, even though the cost of production is higher than that of solar or wind generators."

The valuation question

Considering all these factors, “we are looking at a ₹40,000-50,000 crore valuation if they go for a 20-25% dilution," Sankhe said. “The market is expecting 20GW of installed capacity (for the company) in the next five years, which will require an equity infusion of ₹20,000 crore. This is a best-case scenario on a conservative basis."

While the company’s valuation is anybody’s guess at this point, industry experts agreed that NTPC Green’s IPO is a crucial step to positioning itself as a one-stop solution for pure-play renewable energy in India.

“If you are embedded into a large entity like NTPC then it is difficult for investors to take cognisance of what you are doing. Hence, the idea of the IPO is to let investors know what NTPC Green is doing and discover its value," said the fund manager quoted above.