Interested in penny stocks? These three debt-free companies may be right up your alley.

- It's important to remember that penny stocks are inherently volatile, and that even debt-free companies aren't immune to market fluctuations, competition and other challenges.

Penny stocks can offer exciting opportunities for investors seeking high returns with relatively little capital. While these stocks come with higher-than-average risk, their potential for growth makes them appealing to those with a risk appetite to match.

But not all penny stocks are created equal. A key factor that sets some apart is their ability to remain debt-free, which gives them the flexibility to invest in growth and navigate challenges without the burden of loans.

As we look ahead to 2025, a few debt-free penny stocks exhibit strong growth prospects. These companies have established a solid foundation with smart management, a clear vision, and the financial discipline to avoid debt.

Also read: Keep an eye on these three SME stocks that insiders are buying

By operating with low overheads and focusing on expansion, they are positioning themselves to capitalise on market opportunities in the near future.

In this article, we'll highlight three debt-free penny stocks that have potential for substantial growth owing to their strong fundamentals.

For investors seeking both value and growth, these companies are worth keeping an eye on.

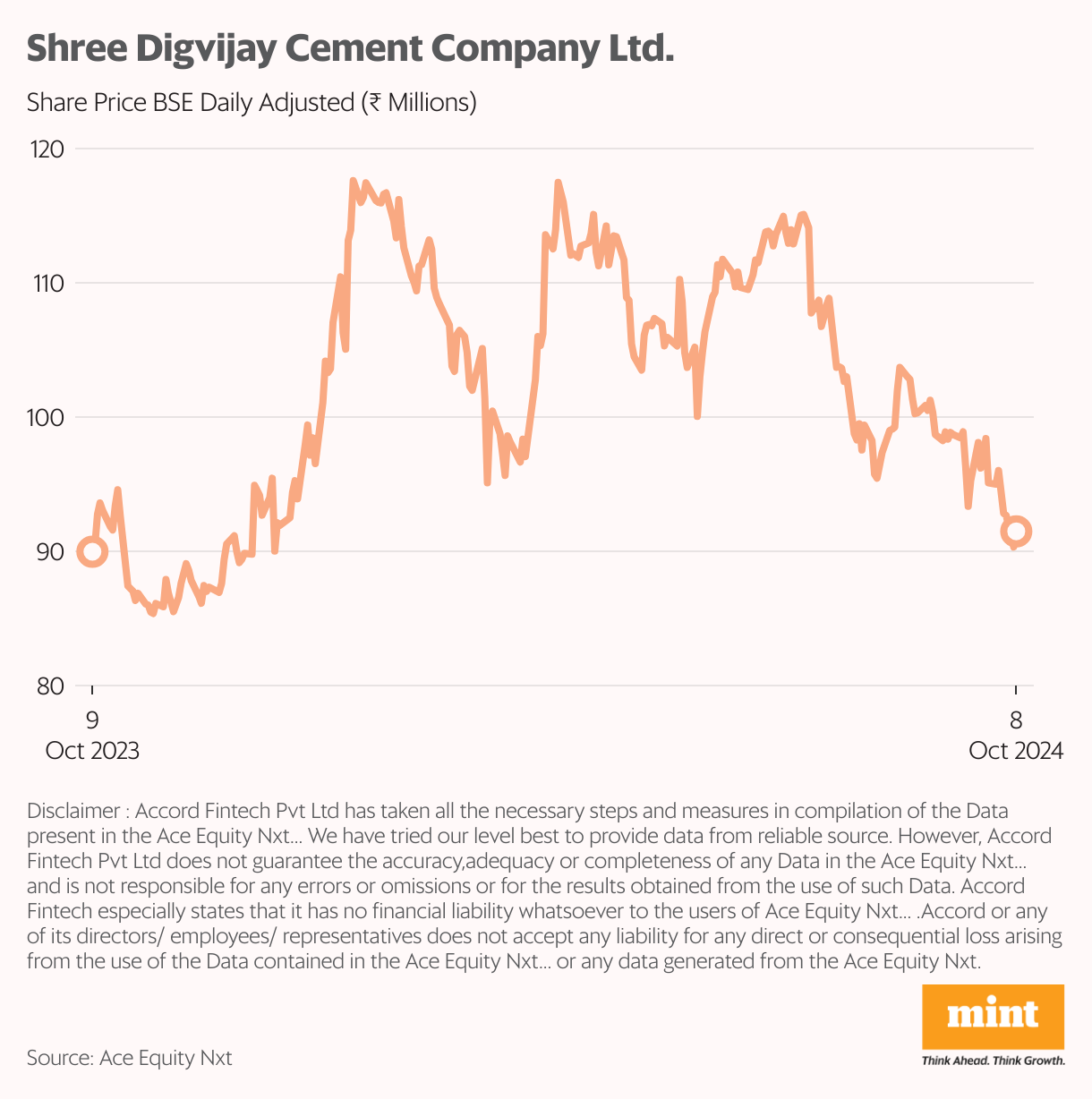

#1 Shree Digvijay Cement

The company manufactures and sells cement. Its products include Portland Pozzolana Cement, Ordinary Portland Cement, Sulphate Resisting Portland Cement, and oil well cement, sold under the brand name 'Kamal'.

In the past five years, revenue and net profit have grown at a compound annual rate of 13% and 115%, respectively, on the back of higher sales realisations and volumes.

The company expanded its capacity from 1.2 million tonnes per annum (MTPA) to 1.5 MTPA, which helped improve realisations. This translated into stronger return ratios as well. The return on equity (RoE) was 24.9% and return on capital employed (RoCE) was 34.1% as of March 2023.

Shree Digvijay Cement has been reducing its debt over the past few years and is now debt-free. It also pays dividends consistently. It has a three-year average dividend payout of 80.7% and a dividend yield of 3.2%.

For FY25, the company's volume is expected to grow due to demand from the infrastructure segment and brownfield capex to increase cement grinding capacity from 1.5 million tonnes to 3 million tonnes.

Also read: Is 2025 the perfect time to invest in India’s green finance stocks?

The project is estimated to cost ₹250 crore. Half of it will be funded through debt and half through internal accruals. It’s expected to be commissioned in the fourth quarter of fiscal year 2025.

Given the size of the project, the company is exposed to execution risks, so it’s important to monitor whether it sticks to the timeline and budget. However, its track record on completing various capacity-addition projects provides comfort.

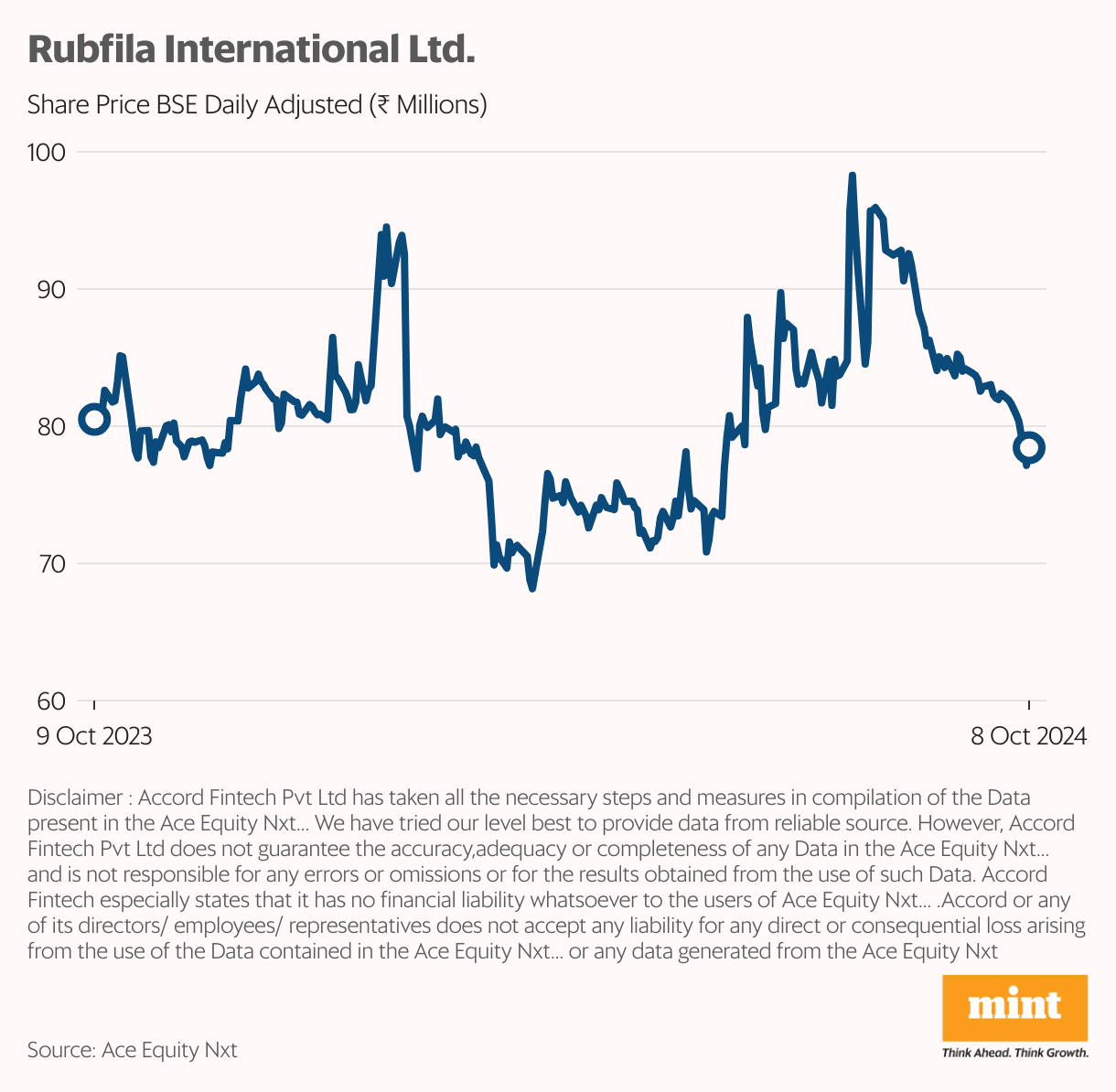

#2 Rubfila International

Rubfila International is one of India's largest manufacturers of heat-resistant rubber threads. It’s the only Indian company that manufactures both talcum and silicon-coated rubber threads.

Its products are used in niche areas such as toys, meat packing, medical webbing, and bungee jumping cords. It has also entered the hygiene segment by acquiring Premier Tissues.

Rubfila has a manufacturing capacity of 20,000 metric tonnes (MT) and is expanding its capacity to meet the growing demand for rubber threads. It has a strong domestic presence and exports to more than 30 countries.

In the past five years, revenue has increased at a compound annual growth rate (CAGR) of 17%, led by high demand for rubber threads. Net profit has also grown at a healthy 6% over this period. The company is debt-free, which gives it the flexibility to take on leverage to expand.

Also read: Top 5 debt-free stocks to watch out for in 2025

Rubfila has consistently paid dividends in the past three years, and has a three-year average dividend payout of 24% and a dividend yield of 1.5%.

Its brand Rubfil has a good reputation in India and overseas and remains its biggest strength, allowing it to expand to more international markets.

Though there has been a slowdown in the innerwear and garment markets in the past couple of years, they are expected to bounce back.

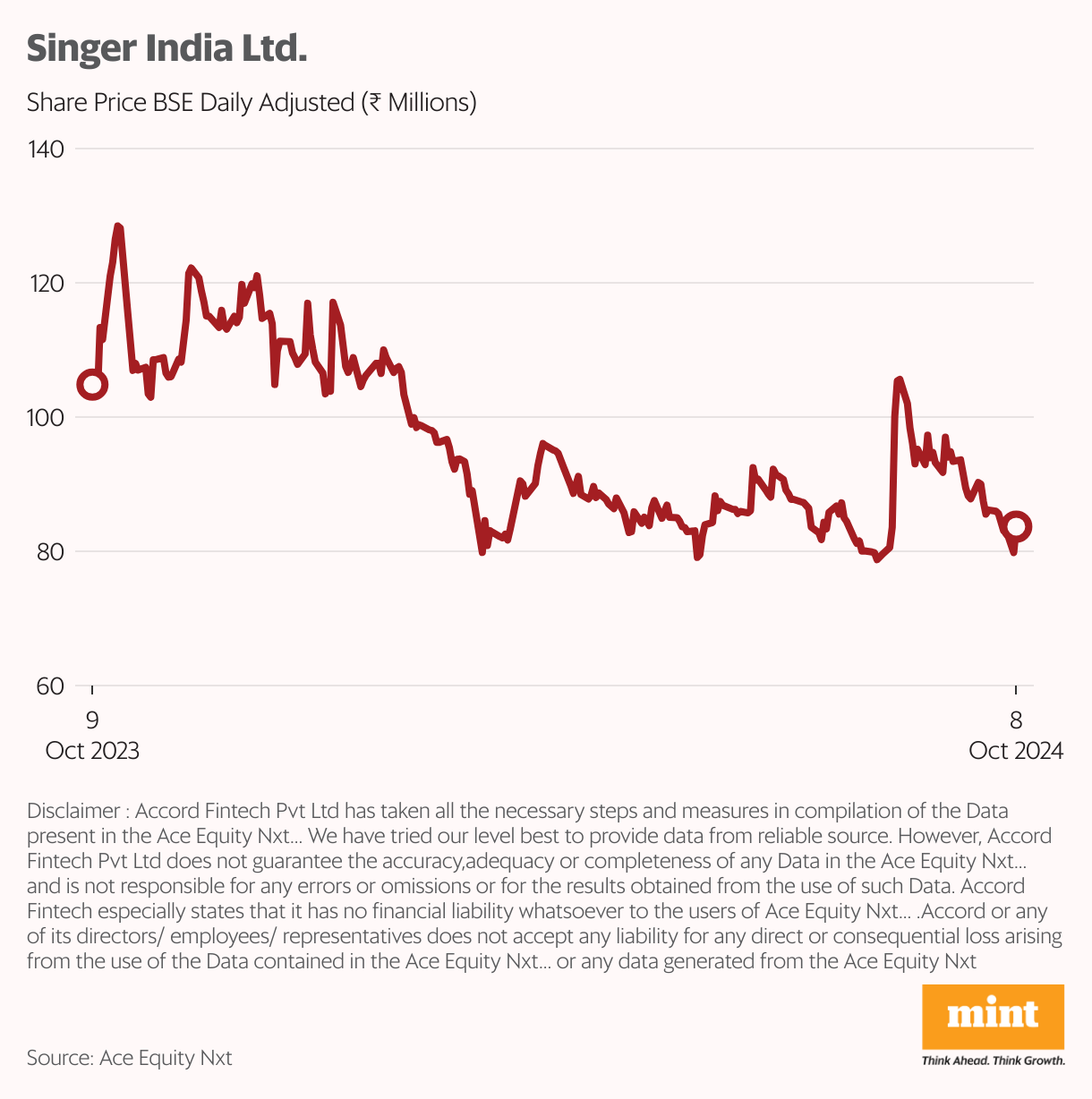

#3 Singer India

The company manufactures sewing machines and domestic appliances. It has an asset-light model with outsourced contract manufacturing and a back-to-back warranty with vendors for major defects. A back-to-back warranty is one in which the warranty in a resale is identical to that of the original transaction.

However, Singer India’s growth has suffered in the past few years. The entry of several large players into the consumer durables segment has led to significant competition on price, hamperingprofitability. However, it’s expected to improve in the coming years, partly because it remains debt-free.

This year the company is working on value engineering and reducing costs to offer better products at competitive prices as it looks to improve its gross margin and capture a bigger market share. It plans to grow the industrial sewing machines business by introducing a new range of efficient sewing machines at reasonable prices.

Also read: How hybrids are reshaping India's green auto market

Its Zig Zag household sewing machines have incredibly low penetration in India and offer immense potential for expansion. The company plans to introduce a new range of Zig Zag machines capable of embroidery. It also plans to drive profitable growth in the appliances segment by increasing its brand familiarity and through premiumisation.

Recently, Rakesh Jhunjhunwala and Associates bought shares of Singer India. The late super investor's company holds 4.3 million shares of the company, which account for 6.9% of its portfolio as of the June quarter.

Conclusion

Investing in penny stocks can be risky, but focusing on debt-free companies with strong growth potential can help mitigate some of that risk.

The three companies above offer a unique combination of financial discipline and growth prospects, and thus stand out in the world of penny stocks.

By operating without debt, these businesses can reinvest profits, expand operations, and pursue growth opportunities without the burden of loans.

Also read: 10 stocks to play the great Indian wedding boom

However, it's important to remember that penny stocks are inherently volatile, and that even debt-free companies aren't immune to market fluctuations, competition and other challenges. Investors should conduct thorough research and consider their risk tolerance before making any decisions.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com