Portfolio reshuffle: Private banks, consumption stocks find favour with mutual funds on attractive valuations

Fund managers steer clear of pricey capex-driven bets such as capital goods, engineering and public sector units.

Fund managers are steering clear of pricey capex-driven stocks, switching focus to private banks and defensive bets such as pharma and consumer goods that are still available at relatively cheaper valuations.

The sectoral rotation is evident in the performance of these segments as Nifty Pharma index surged 17% and the Nifty Healthcare gauge jumped 16% over the past three months. The Nifty Private Bank, FMCG, and IT indices rose 6-25% during the period against a 9% rise in S&P BSE Capital Goods index.

Sectors that led the rally in the past two years appear to be richly valued; hence, certain stocks in capital goods, engineering and public sector may not create alpha—beat the benchmark —in the near term, said Gaurav Dua, senior VP and head of capital market strategy at Sharekhan by BNP Paribas. Some fund managers have readjusted their portfolios, he said, as valuations are supportive in healthcare, private banks and select consumer stocks.

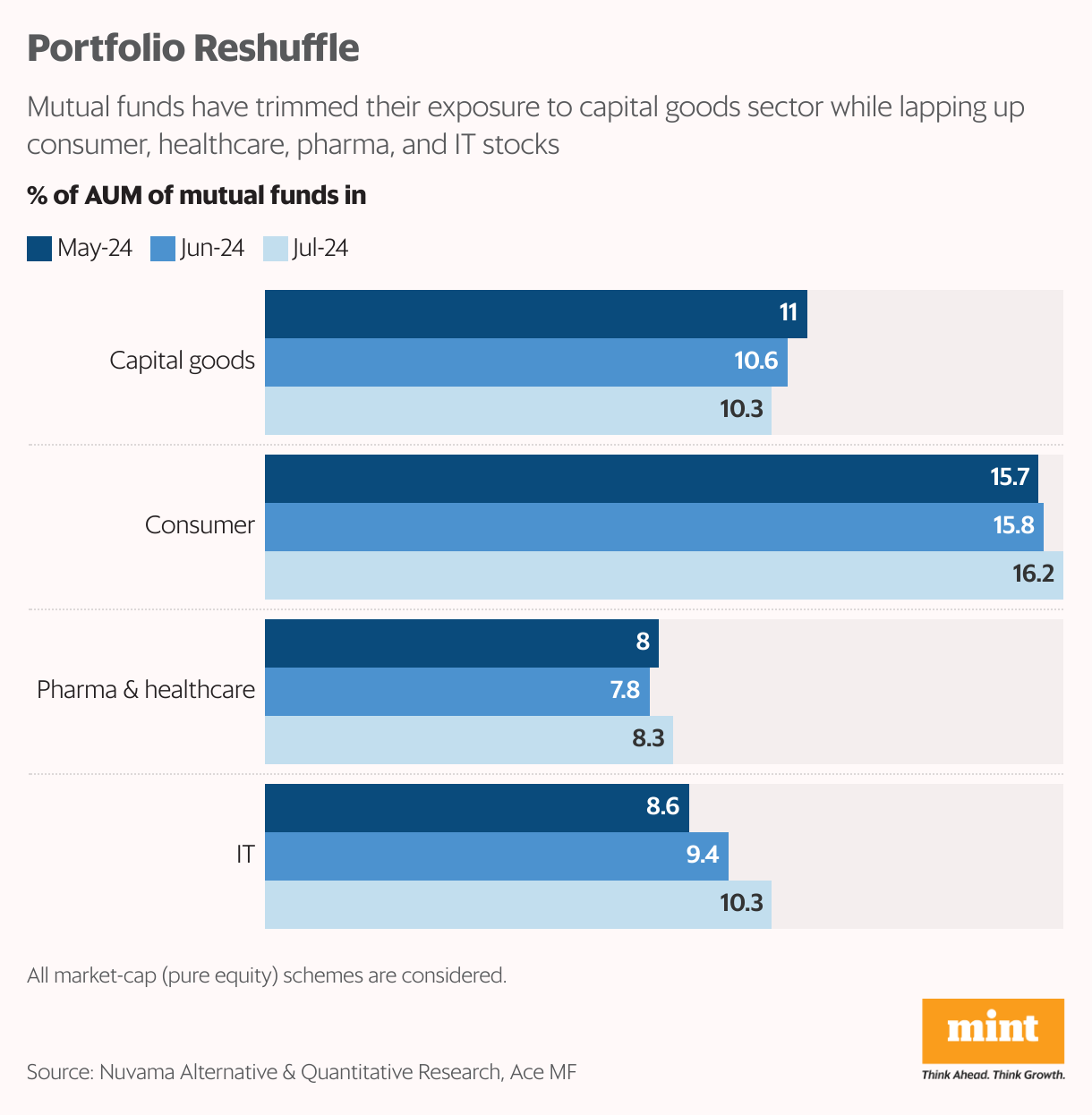

In July, capital goods stocks accounted for 10.3% of the assets managed by mutual funds, compared with 11% in May, show data compiled by Abhilash Pagaria, head of Nuvama Alternative and Quantitative Research. In contrast, holdings in consumer and pharma and healthcare stocks edged up to 16.2% from 15.7%, and to 8.3% from 8%, respectively. Mutual funds also increased their IT exposure to 10.3% in July from 8.6% in May.

The government's pivot from prioritizing capital expenditure and infrastructure to focusing on the rural sector and job creation suggests conditions conducive for the former themes (like capital goods, engineering, infrastructure, power, defence sectors) are less prevalent now, said Dhiraj Relli, MD & CEO of HDFC Securities. “Conversely, the previously underperforming consumption sector may revive due to this policy focus shift."

Also Read: Investors need to temper their expectations: Nippon India Mutual Fund CIO

Supportive valuations

Analysts said private banks hold potential since they are trading at below-average multiples.

“The risk-reward in private sector banks is currently attractive, with stocks trading below their 5- and 10-year average valuations," said Karthikraj Lakshmanan, senior vice-president and fund manager-equity at UTI AMC. "These lenders are showing double-digit growth, outpacing banking industry growth."

While their return on equity (RoE) have dipped slightly due to leverage coming down post-Covid, they remain reasonably strong, according to Lakshmanan. He expects a better monsoon this year to drive a rural recovery, helping consumer companies with a higher exposure to the hinterland.

Relli, too, has a positive outlook on private banks despite the challenges faced in mobilising deposits and early signs of stress in asset quality. “These challenges are already factored into their pricing."

Moreover, private banks’ RoE improved in FY24, surpassing the BSE500 and industrial sectors, indicating that the worst may be over for them, he said.

Also Read: Rural markets to grow faster than urban in FY25 on good monsoon: Kantar

It’s not that capital goods, defence, infrastructure, and power sectors companies are not growing. Analysts flagged their exuberant valuations.

The BSE Capital Goods index is trading at 47.64 times its earnings compared with its five-year average of 29.5 and the 10-year average of 28.81, according to Bloomberg data.

"When you consider both factors, these sectors have likely outperformed significantly, making the risk-reward less favourable," Lakshmanan said.

He is overweight on private banks and information technology and consumer durables/retail, also his preferred bet over fast-moving consumer goods. Lakshmanan finds healthcare stocks reasonably valued, but advises caution on power, suggesting it is wiser to increase weight when valuations are more reasonable.

Flip side

There are some fund managers who look at things differently.

A major shift in the Indian economy is the move from a service-driven model to a manufacturing-driven one, said Ashish Naik, fund manager at Axis Mutual Fund. While the past decade was consumption-focused, he said, this one will blend consumption with investments,

Unlike services, large-scale manufacturing requires diverse infrastructure—power, water, ports, and roads. Setting up mobile or auto manufacturing units also drives demand for ancillary services, creating a broader growth narrative.

“These investments are generally long term, which is why many stocks in this sector may seem expensive in the short term," Naik said.

Also Read: Is it end of the road for debt mutual funds with new capital gains tax norms?

If these companies sustain their growth and achieve higher targets, they could deliver substantial returns, he said. This trend could persist for a decade or more, driving major shifts and creating numerous sub-themes and sub-sectors in the market.

“To that extent, I am overweight on these sectors," Naik said.

In recent years, there has been a strong uptick in high-end consumption, leading to a K-shaped economic recovery.

“Eventually, we should also see growth in the lower segments of the economy," Naik said. “And an increased spending in the rural sector could stimulate growth in various other sectors."