Props pump up derivatives volume; retail falls behind

")

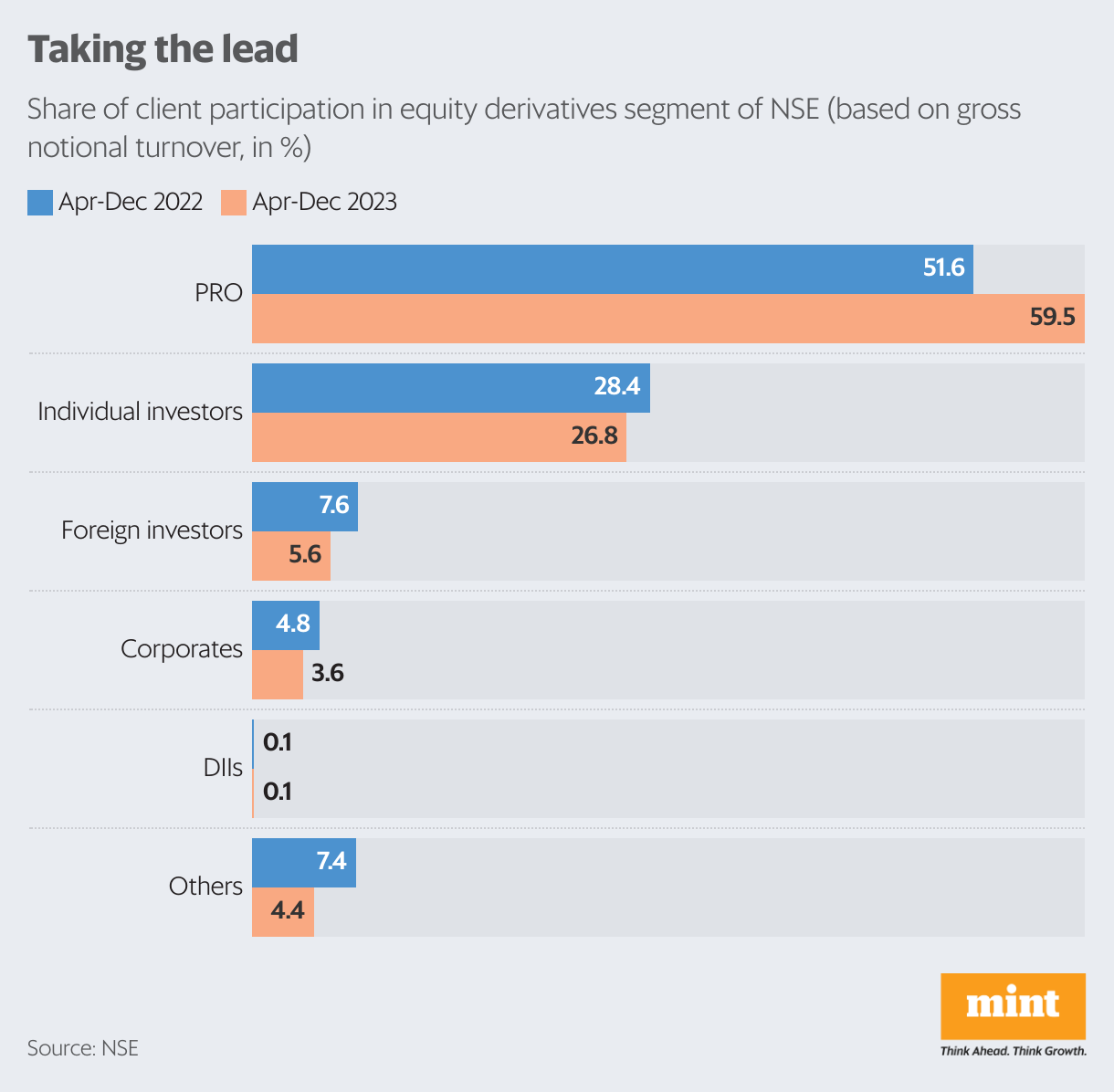

- Proprietary traders’ share of gross turnover surged to 59.5% in Apr-Dec 2023, up 783 bps from a year ago, while retail investors’ market share dipped

Retail investors dabbling in derivatives often get the short end of the stick. But few know that they lose out to proprietary traders or props—brokers trading on their own account with sophisticated algorithms.

Prop traders pay hefty sums to place their server racks in the exchange data centre (called colocation), something retail investors can’t do. This enables props to access data of price movements fractions of a second quicker than retail investors, who use Internet-based trading and mobile apps.

The National Stock Exchange of India (NSE) charges ₹12 lakh to colocate a (full rack) server in its data centre, plus connectivity charges and taxes. The exchange started the colocation facility in 2009 so that brokers located in, say, Mumbai and Chennai would get data feeds at the same time, despite the Mumbai broker being closer to the exchange’s servers.

Interestingly, exchange data shows that colocation-based trades accounted for 60.7% of gross turnover in April-December 2023, up 247 basis points (bps) from a year earlier, followed by mobile-based trade at 17.6% (up 22 bps), Internet-based trades at 8.9% (down 106 bps) and algo trades 1.1% (up 45 bps). A basis point is one-hundredth of a percentage point.

Prop was the only category whose market share on NSE—the world’s largest derivatives exchange by contracts—has risen in the current fiscal year through December. Their share of gross turnover surged to 59.5% in April-December 2023, up a whopping 783 bps from a year ago. Individual or retail investors’ market share dipped by 163 bps to 26.8%, according to NSE data.

The share of foreign portfolio investors, corporates and others (partnership firms, trusts, societies, etc.) declined while the share of domestic institutional investors (mutual funds, insurance and banks) remained steady, the data shows.

Gross turnover (buy side plus sell side) stood at ₹110,510 trillion in FY24 (April-December) against ₹76,446 trillion in FY23. The turnover is calculated using the notional turnover of index options, the most popular derivatives instrument on NSE.

“Quick decision-making and speed of execution are keys to success in the derivatives space," said Rajesh Palviya, senior vice-president, Axis Securities.

“Thanks to colocation and discretionary automated trading platforms (algos), prop is invariably ahead in the race compared to their counterparties, retail most of the time. They keep entering and exiting the market at regular intervals in a day, which retail can’t do because they lack the resources," he added.

Algos or automated trades are of two types: decision and execution algos (also called black-box algos) and execution-only algos. Palviya said algos used by props tend to be black-box types, which can reverse direction rapidly in case of a contra market movement.

For instance, if an algo initiates a short position at 21,900 with a stop-loss at 21,950 and the market moves to 21,950, the black-box algo reverses direction at the stop loss and initiates a long position. In the same situation, a retail trader is stopped out of the market and can’t play for greater upside, he explained.

However, Rajesh Baheti, managing director of Crosseas Capital, one of the country’s largest arbitrageurs and jobbers, said it wasn’t resources but “informed decision-making" that gave prop an edge over retail. “Retail tends to act on tips, whereas prop enters after doing deeper research," said Baheti.

Jay Prakash Gupta, founder of market platform Dhan, said it was resources, deeper pockets and being sellers of options that put prop ahead (of retail) in the game.

“Retail tends to be buyers of options, while an options seller (prop) makes money eight out of 10 times as an option loses value with the passage of time, something that retail doesn’t seem to understand. So, if the market doesn’t move, an option loses value each day it’s held, enabling the option seller to pocket the premium paid by the option buyer."

Index options derive their value from the NSE’s Nifty and Bank Nifty indices.