Markets

Markets

World War 3 looms? The ultimate checklist for Indian investors

")

Summary

- The simmering tensions in West Asia took a dramatic turn last week after Iran fired a volley of ballistic missiles at Israel. How will the crisis impact the stock market? History is the best guide but check out our list of dos and don’ts.

New Delhi: “Buy on the sound of cannons, sell on the sound of trumpets."

— Nathan Mayer Rothschild

17 January 1991. Time: 2.38 am. Eight US Army Apache helicopters flew over the Iraqi–Saudi Arabian border and bombed some Iraqi radar sites. Five minutes later, 24 US Air Force fighter jets attacked airfields in Western Iraq. At 3 am local time, 10 more stealth attack jets raced to Baghdad and began bombing Iraq’s capital.

After months of frenzied diplomacy and military buildup, the US-led coalition forces had launched Operation Desert Storm, marking the beginning of hostilities in the Gulf War of 1991—the biggest global conflict since World War II.

Wall Street reacted to the momentous occasion by posting its second-biggest single-day jump ever, with the Dow Jones industrial average soaring nearly 115 points to close at 2623.51. Volumes on the New York Stock Exchange were the eighth-highest on record.

This was not an aberration.

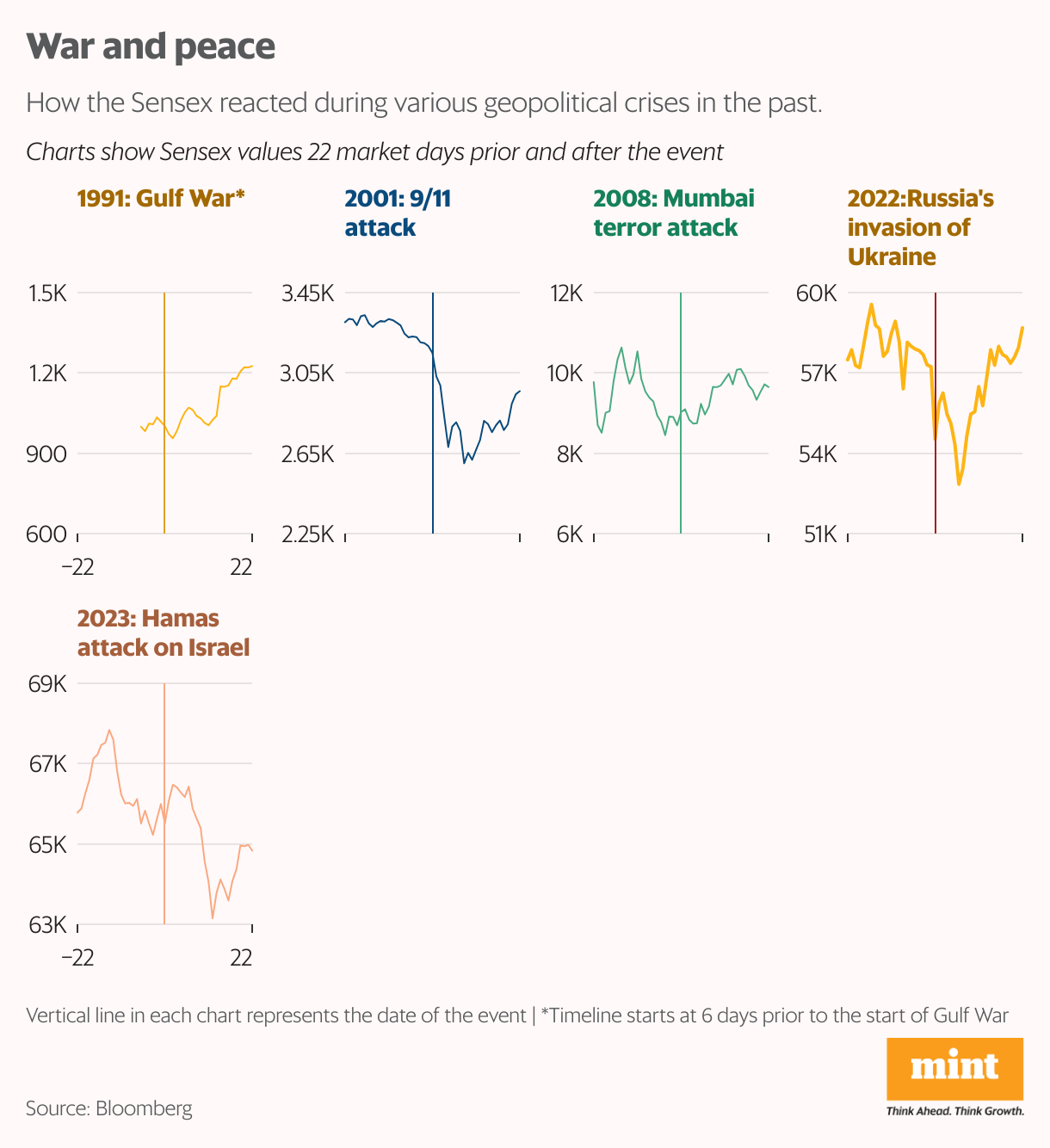

Despite being the eternal battleground between the bulls and bears, stock markets have reacted with remarkable equanimity during times of actual war.

As per an oft-quoted study by LPL Research, the US stock market slipped by an average of only 5% during 20 major geopolitical events since World War II, including the Cuban Missile Crisis, John F. Kennedy’s assassination and 9/11 terror attacks. Not just that, the market was able to recoup the losses in less than 50 days, on average.

Not that this is peculiar only to the Mother Market.

When the Russia-Ukraine war started on 24 February 2022, the NSE Nifty was the third-worst-performing major index globally, with a 4.78% decline. However, it soon found firmer ground and took just eight sessions to go from 15,863 to 17,000—in lockstep with a robust rally overseas.

Even during the present conflict in West Asia, Indian markets were little changed in the aftermath of Hamas’s attack on Israel on 7 October 2023, and continued its upward march unabated.

Will markets follow a different trajectory this time round?

Flare Up

The simmering tensions in West Asia took a dramatic turn last week after Iran fired a volley of ballistic missiles against Israel in response to Tel Aviv’s military action in Lebanon. Israeli air strikes had killed Hezbollah chief Sayyed Hassan Nasrallah in late September, dealing a massive blow to the Iran-backed militant group.

Meanwhile, Iran’s supreme leader Ayatollah Ali Khamenei, who led Friday prayers in Tehran for the first time in 5 years on 4 October, has warned of further retaliation.

Israel, which has intensified its action against both Hamas and Hezbollah, is reportedly mulling attacks on Iranian oil rigs as well as nuclear sites. This has sent alarm bells ringing across global capitals, with the US, EU and other powers scrambling to de-escalate the situation.

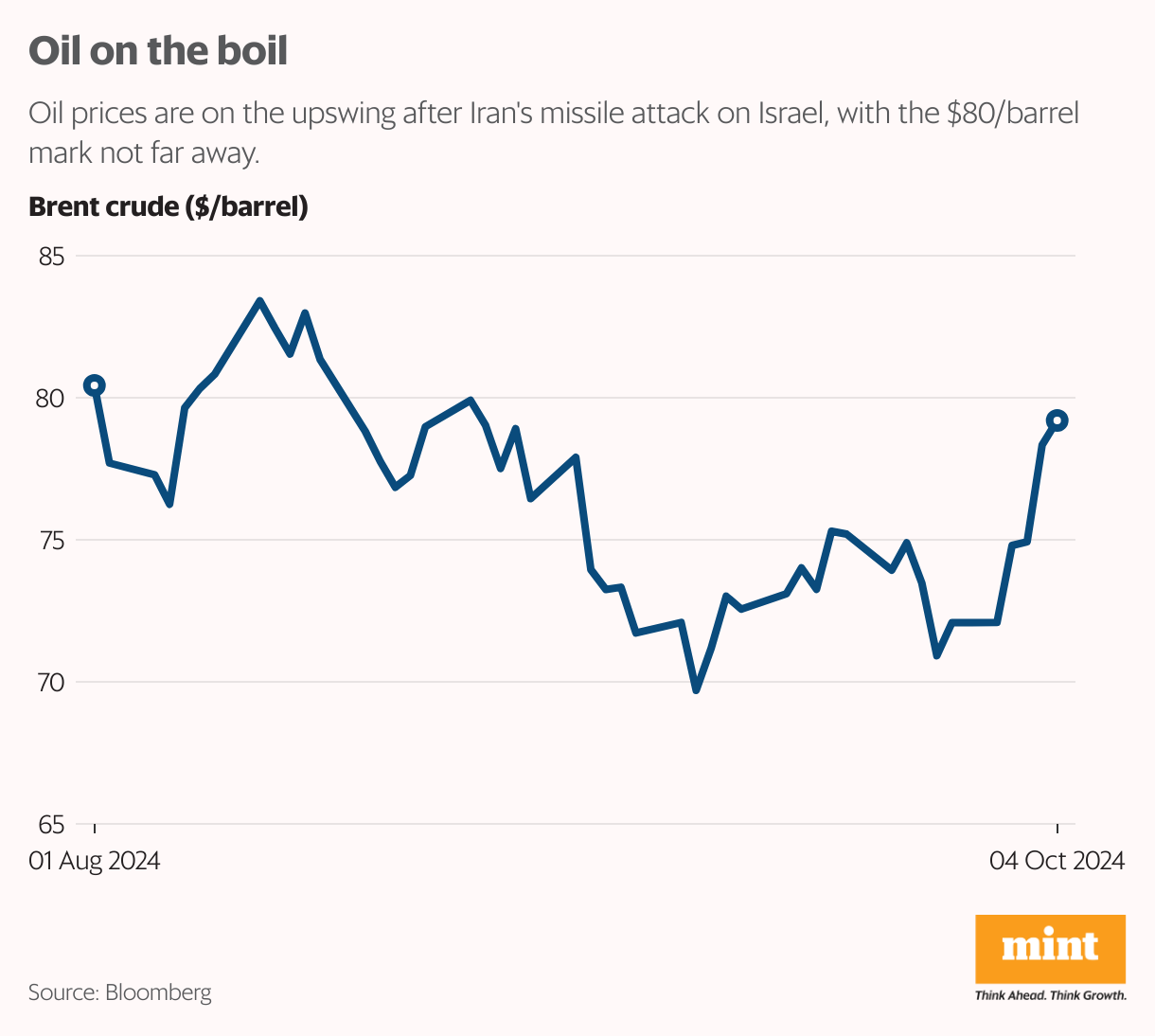

For India, the immediate concern is oil prices.

Global oil benchmark Brent crude surged 8% last week—the biggest weekly gains in over a year—on concerns over West Asia erupting into a full-fledged regional war.

The oil market is looking warily at the latest crisis, which comes after a year of turmoil in which Israel has confronted Iran and its proxies in Palestine, Lebanon, Yemen and elsewhere. West Asia accounts for about a third of global supply, and traders are fretting over a massive supply crunch if Iranian oil facilities are bombed or sea routes are blocked.

Oil is among the most crucial components of India’s macroeconomic health. The country is the world’s third-largest oil consumer and importer, after China and the US. India meets over 85% of its oil requirement through imports, making it particularly vulnerable to global price shocks.

India’s crude oil import bill dropped 16% in 2023-24, thanks to lower oil prices. India imported 232.5 million tonnes of crude oil that year, which is refined into fuels like petrol and diesel, almost the same as in the previous financial year. But it paid $132.4 billion for the imports in 2023-24 as against $157.5 billion import bill in 2022-23, according to data from the oil ministry’s Petroleum Planning and Analysis Cell (PPAC). This also helped contain the current account deficit to $23.2 billion or 0.7% of GDP in 2023-24, from $67 billion or 2% of GDP during the previous year.

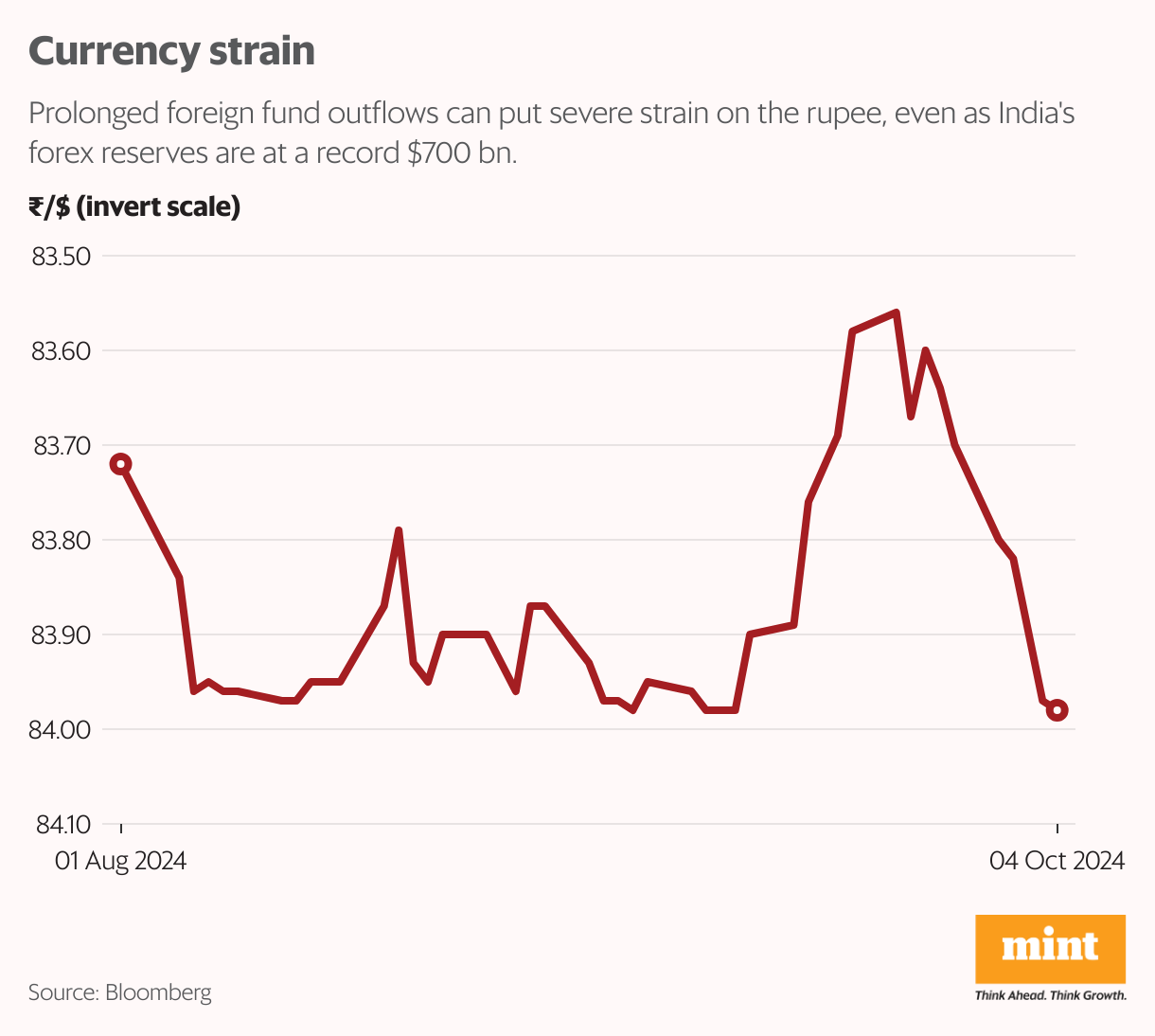

But oil prices hardening in response to the rising tensions could reverse this positive trend, as oil constitutes around a third of India’s import basket. This, in turn, will have a spillover effect on the rupee by spurring dollar demand—the Indian rupee was Asia’s worst-performing currency last quarter.

A widening current account deficit will put further pressure on the currency, especially since gold imports (and prices) show no signs of easing.

It also goes without saying that higher crude prices will stoke inflationary pressures by driving up the prices of petrol and diesel, which has a cascading effect on the prices of most goods and services.

India’s retail inflation has been below the 6% mark since September 2023, remaining within the central bank’s tolerance range of 2-6%. Core inflation–which excludes the more volatile food and energy prices—makes up nearly 50% of the basket. Any uptick in the inflation numbers will also delay the much-awaited rate cut from the Reserve Bank of India (RBI), which will be a dampener on market sentiment.

That said, some experts believe it’s not all gloom-and-doom for India.

“In the short term, the Indian economy is unlikely to be significantly affected by an escalating West Asia conflict, thanks to its robust macroeconomic fundamentals. However, it would face an impact if the conflict were prolonged. While rising oil prices is a concern, we believe Opec (the Organization of the Petroleum Exporting Countries) has sufficient spare capacity to offset a complete loss of Iranian oil supply," said Anil Rego, founder and fund manager at Right Horizons, a portfolio management service provider.

“Additionally, rising US inventories further demonstrate that the market is well-supplied and capable of handling potential disruptions, so price gains are likely to be capped. Tensions have been on the rise for some time and we believe markets are looking ahead to the earnings season which is likely to have more of an impact in the near term," he added.

Sector Watch

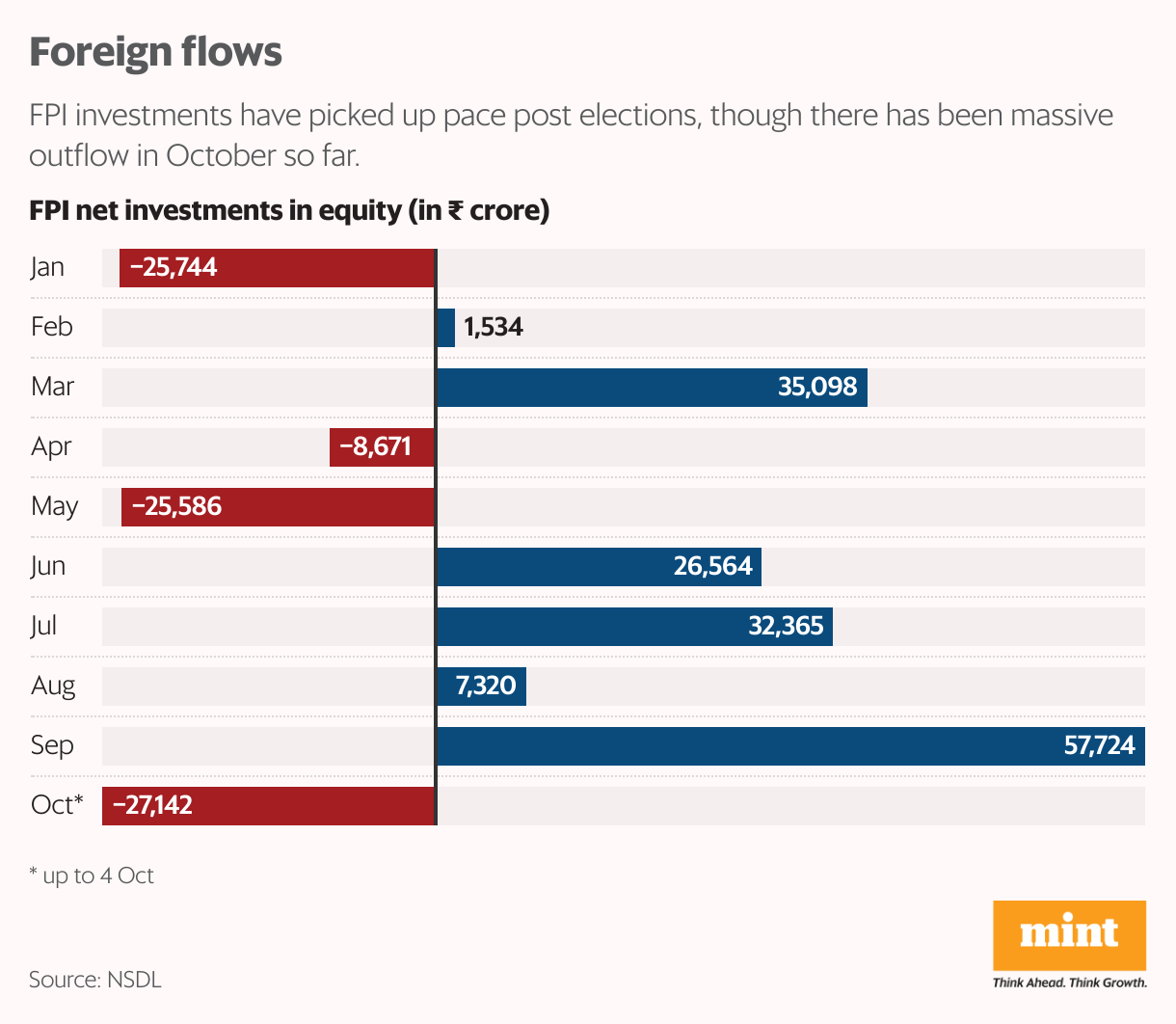

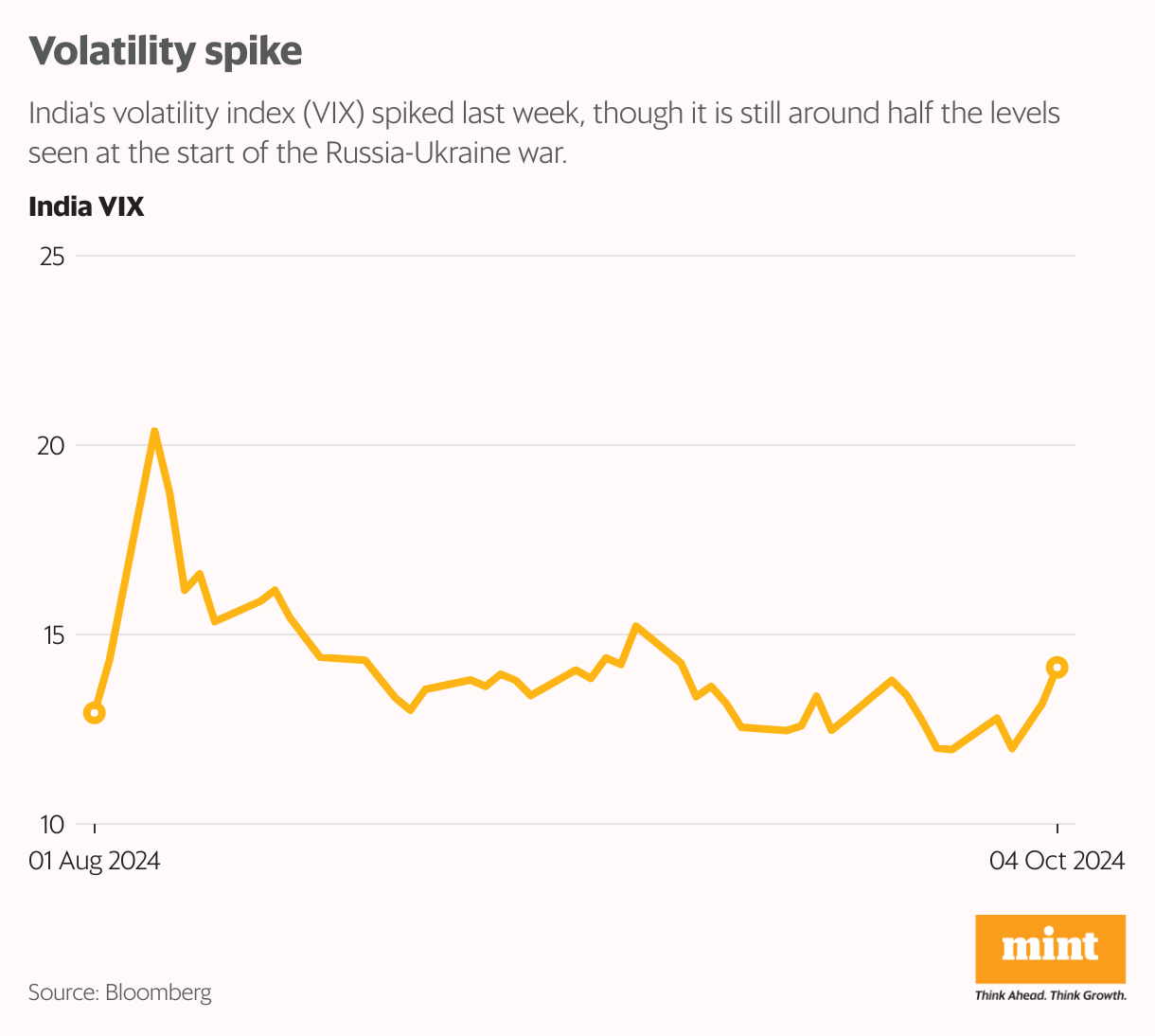

Macroeconomic implications aside, domestic markets were dealt a heavy blow last week as the Sensex posted its worst week since June 2022, crashing 3,884 points or 4.5%. Investors suffered a wealth erosion of ₹16.3 trillion.

On 3 October, foreign portfolio investors (FPIs) dumped shares worth ₹15,243 crore—the highest ever in a single session—followed by ₹9,897 crore the next day.

While markets are expected to stabilize soon, thanks to heavy buying by mutual funds and other domestic institutional investors, investors need to track certain sectors a bit more closely amid the current upward pressure on oil prices.

Tyre and paint manufacturers, fast-moving consumer goods (FMCG), carbon black and lubricant makers and specialty chemicals firms are heavily reliant on crude oil and its derivatives. The biggest blow, of course, will be on state-owned oil marketing companies (OMCs).

“OMCs like BPCL and HPCL may face margin squeezes since they would find it difficult to fully pass on the higher cost up the supply chain. However, the increase in crude oil prices can help oil producers like ONGC," Ravi Singh, senior vice president of retail research at Religare Broking, told Mint.

According to him, investors should steer clear of two sectors in the short term.

“The first is aviation, as the sector would take a cut in profitability in case of a hike in fuel prices. New positions in this aviation sector should be best avoided since the industry is very sensitive to high variability in oil prices," he said. “The second is commuter vehicles. Automobile companies are going to feel the impact of decreasing demand in the case of increasing fuel rates. For now, they look less attractive."

")

Other sectors, too, will bear the brunt in the event of elevated crude rates.

FMCG and consumer durables industries may be squeezed through margin compression due to rising transportation as well as raw material costs. If the resultant high prices are passed on to the consumers, then demand may slow down, especially in the price-sensitive markets. Chemicals and manufacturing sectors can see a spike in their input costs as they use petroleum-based raw materials.

At the other end of the spectrum, Singh recommends increasing allocation to some segments. “The immunity of IT services and tech stocks against geopolitical events makes companies like TCS and Infosys safe havens in unpredictable market times," he said. “Besides, the defensive pharmaceuticals sector is more likely to perform well in uncertain global situations. Indian pharmaceutical companies, especially those with substantial diversification across the world in their business line, such as Sun Pharma and Cipla, are quite likely to remain stable in this period," he added.

Geopolitical conflicts do not necessarily mean investors have to take a defensive approach. For those looking to play offence, there’s one industry which has risen remarkably in prominence in recent times.

“The defence sector is likely to perform well, particularly companies exporting to Israel. India exports surface-to-air missile components to Israel, and some listed companies are seeing record revenues from this," Sreeram Ramdas, vice president at Green Portfolio PMS, told Mint.

Defence sector stocks have seen a furious rally over the past year, pushing their price-to-earnings multiples to stratospheric levels. After rising about 100% over the past year, the Nifty India Defence Index has succumbed to a severe bout of profit-booking in the past month. However, the valuations are still uncomfortably high, which investors should keep in mind. But for those looking to play a long-term game, the sector clearly offers an attractive opportunity.

Real Risk Lies Elsewhere

Global catastrophes, by their very nature, trigger an avalanche of frenzied headlines which is hard to escape from. Investors may think tracking every update on the West Asia situation will keep them ahead of the curve, but the fact is that for Indian markets, the biggest risk right now is not whether Israel bombs Iran but whether ‘narratives’ will continue to eclipse ‘numbers’.

“Since 2022, Indian markets have held up despite the widening West Asia conflict. However, given the overvaluation of our markets and the rapid spread of the war, it’s highly likely we will see a prolonged correction," Ramdas said.

It is sentiment which is finding greater traction among market participants.

In a report on 1 October, Kotak Institutional Equities noted that the large inflows into domestic markets from retail investors show the high levels of “greed" in the market. The increase in greed among investors has been accompanied by a concurrent and corresponding decline in the fear of risks.

“Institutional investors have focused on potential sources of risk... but oddly ignored the fact that the biggest source of risk could simply be the large gap between current prices and fair values of stocks across the board (negative margin of safety). Stocks have been at inflated levels for a while, which increases the odds of a correction. The driver of a correction could be anything but the outcome will be the same," it said.

According to Kotak, the current large gap between the stock prices and fair values of stocks raises the worrisome prospect of massive loss to a certain set of investors, as and when stock prices were to align with their fundamental levels. The question is not of “if", it added ominously.

Another potential trigger for foreign portfolio investment (FPI) outflows from India is the sudden rebound in China stocks, which is expected to suck money from other emerging markets.

Equity markets in China have rallied over 25% in two weeks after Beijing announced a string of measures to shore up the economy, including lowering lending rates to spur the embattled real estate market.

Attractive valuations as compared to India also make China a more attractive bet for foreign fund managers.

")

That said, the days of the Indian market being overly dependent on foreign institutional investor (FII) flows is long gone. But experts say the unabated domestic inflows should not lull market participants into a false sense of complacency. Bull market corrections are usually short, sudden and severe.

For investors, it would be prudent now, more than ever, to curb their speculative instincts and focus on the fundamentals.

“We believe sound resilient businesses with consistent strong financials, high growth potential, and high return on invested capital that are available at reasonable prices are likely to outperform relatively," Right Horizons’ Rego added.