These 5 Nifty stocks delivered strongest EPS gains in a weak FY25

FY25 threw curveballs at India Inc., yet these five stocks outperformed. Here’s what’s fuelling their momentum—and what could derail it.

Corporate India has hit choppy waters in 2025. From sluggish domestic consumption to volatile weather, sticky inflation, and geopolitical shocks abroad—headwinds have come from every direction. For many firms, profits have taken a hit.

And yet, a few outliers are defying the odds.

In this article, we unpack how select companies are bucking the trend with strong bottom-line growth, the levers powering their profitability, and whether their winning streak can continue into FY26 and beyond.

Bharti Airtel

Bharti Airtel, one of India’s leading telecom players, reported a stellar 346% year-on-year (YoY) jump in earnings per share (EPS) to ₹58.85 in FY25, up from ₹13.20 in FY24.

This sharp surge was primarily driven by a significant turnaround in other income, which lifted the company’s bottom line substantially. Airtel’s net profit margin also expanded notably—from 5.7% in FY24 to 21.7% in FY25—highlighting a shift towards a more profitable revenue mix and better cost management.

Even on an already high base, Airtel’s revenue continued to grow steadily. The company reported a 15.3% YoY increase in revenue to ₹1.73 lakh crore, supported by strong performance in both India and Africa. Higher average revenue per user (ARPU) and growing adoption of premium digital services also contributed to the topline momentum.

Also read: Sebi's stricter ESG debt rules may deter mid-sized firms

With a solid operating foundation now in place, Airtel’s next phase of growth will depend heavily on its ability to maintain stable cash flows while managing its substantial debt burden.

As of FY25, Airtel's total debt stands at ₹2.12 lakh crore, while its cash reserves are limited to ₹16,720 crore. This mismatch points to the company’s continued reliance on operating cash flows and refinancing options to meet its financial obligations.

Management has indicated a focus on deleveraging, and to that end, the company has reduced its capex plans for FY26. Lower capital expenditure is expected to boost free cash flows, which in turn could improve its financial position over time.

Despite the overhang of debt, Airtel’s performance over the past five years has been consistently strong. The company has clocked a compound annual growth rate (CAGR) of 15% in revenue and 31% in net profit during this period. Its return metrics also stand out in the sector.

Airtel’s return on equity (RoE) is 28.34%, well above many of its peers who report negligible or negative returns. Its return on capital employed (RoCE) is also healthy at 15.36%, reflecting efficient deployment of capital in a high-investment industry.

Looking ahead, Bharti Airtel is expected to increase tariff charges further to strengthen its financial footing. It has also formed strategic partnerships across its mobile, broadband, and digital TV verticals—including tie-ups with Apple TV and Starlink—to expand its revenue base. Additionally, the company is prioritising growth in home broadband and data centres, with plans to double its data centre capacity to 400 megawatts over the next three years.

Brokerage firm Sharekhan has a ‘BUY’ rating on Bharti Airtel, with a revised price target of ₹2,170.

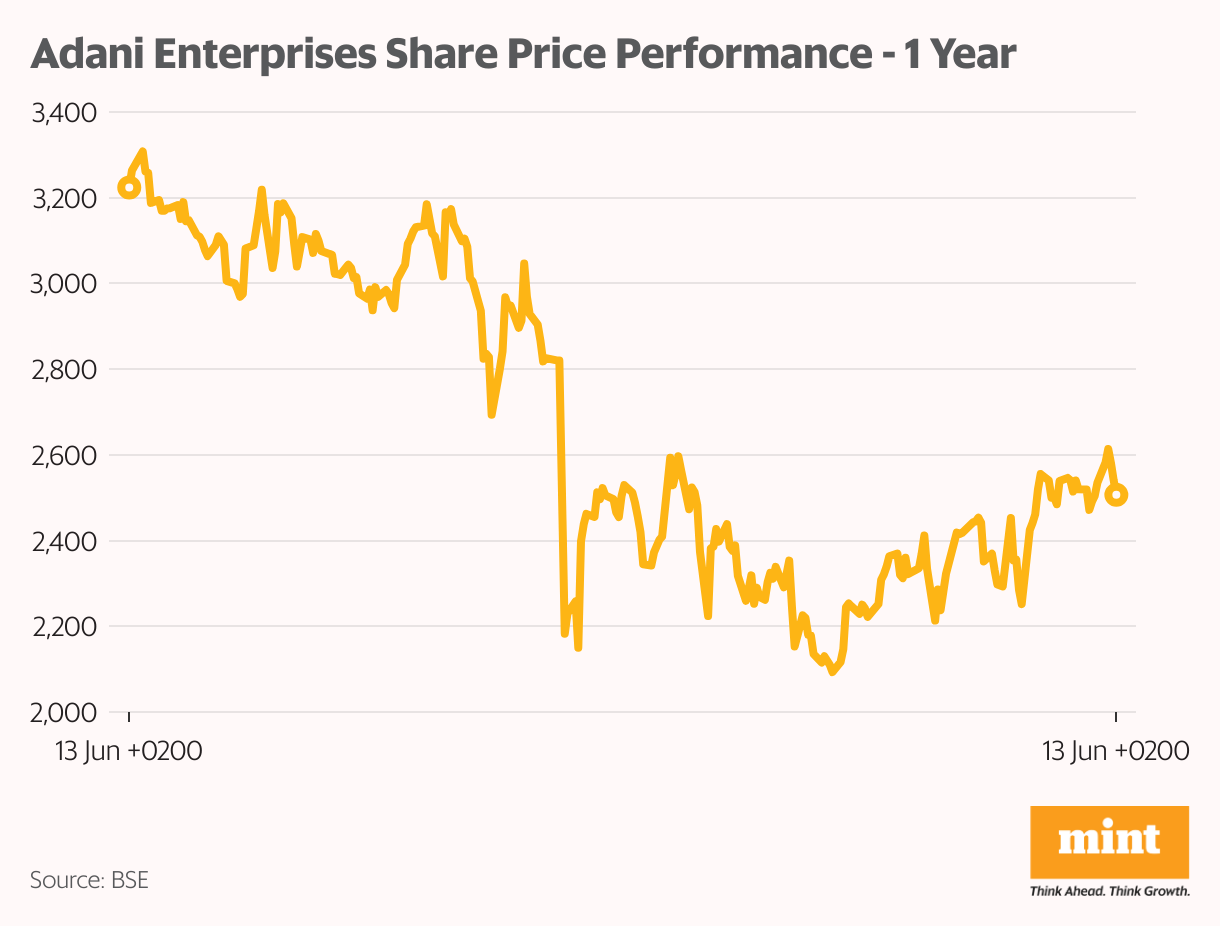

Adani Enterprises

Adani Enterprises, the flagship company of the Adani Group, saw its EPS more than double in FY25, rising 117% year-on-year to ₹61.62 from ₹28.42 in FY24.

The surge was largely driven by a one-time post-tax gain of ₹3,286 crore from the sale of a 13.5% stake in AWL Agri Business Limited (formerly Adani Wilmar Ltd). However, on the revenue front, growth was muted. Sales inched up just 1.5% over the year—from ₹96,421 crore to ₹97,895 crore—following a strong expansion in the previous fiscal.

Despite the flat topline, the company reported strong operating leverage. Its operating profit margin rose from 12% in FY24 to 15% in FY25, indicating better efficiency and cost management.

Looking ahead, Adani Enterprises continues to back its well-known incubation model, with planned investments across emerging and core infrastructure sectors. The group is placing big bets on green hydrogen, data centers, airports, roads, copper, and petrochemicals to drive long-term value creation.

To fund these ambitions, the company expects to spend between $15–20 billion ( ₹1.3–1.7 lakh crore) annually on capex over the next five years. For FY26 alone, it has earmarked ₹5,500 crore for building its green hydrogen ecosystem. But such large-scale plans will require heavy funding.

Adani Enterprises already carries a sizeable debt of ₹91,819 crore, pushing its debt-to-equity ratio to 1.82 times. With cash reserves of just ₹6,962 crore, the company remains reliant on external financing and asset monetisation.

The sale of its remaining 30.42% stake in Adani Wilmar is expected to provide interim support for upcoming capital investments. Over the past five years, Adani Enterprises has delivered impressive financial growth, with revenue rising at a CAGR of 18% and net profit at 39%.

That said, its return ratios remain in single digits, with RoE at 9.8% and RoCE at 9.5%, indicating room for improvement in capital efficiency.

Regulatory risks continue to loom over the company. Credit rating agency ICRA has flagged that the US Department of Justice (DoJ) and the Securities and Exchange Commission (SEC) have filed an indictment and a civil complaint involving the group’s promoters, which remain under judicial consideration.

In India, the Securities and Exchange Board of India (Sebi) is in the final stages of its investigation into the group, following the allegations raised in the Hindenburg report. Investors are advised to closely monitor these developments, as they could significantly impact investor sentiment and corporate governance evaluations.

Despite its strong profit performance, Adani Enterprises’ stock has declined 22% over the past year. Yet, it continues to trade at a steep valuation, with a price-to-earnings (P/E) ratio of 66x—well above its 10-year average of 27.3x.

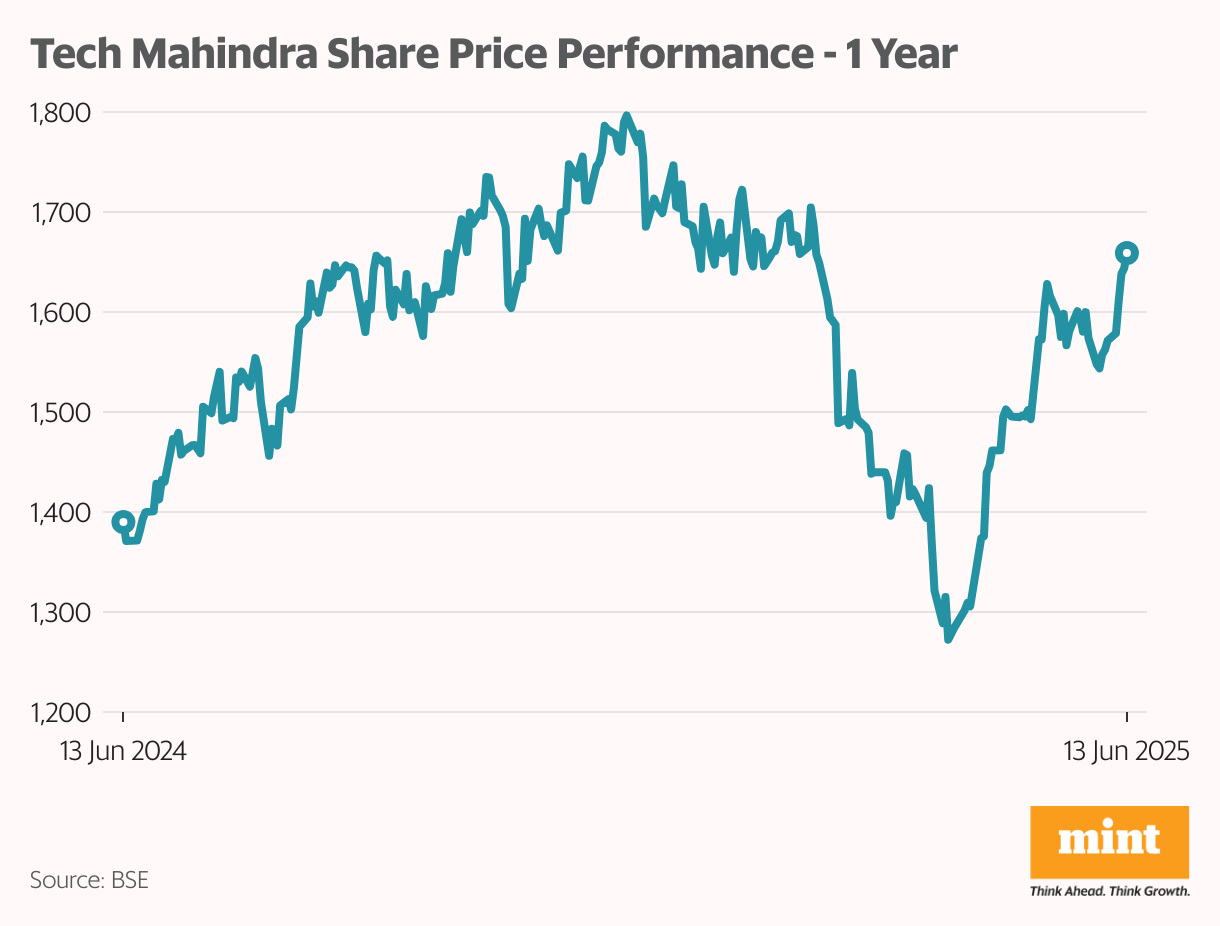

Tech Mahindra

Tech Mahindra, the IT arm of the Mahindra Group, saw a strong rebound in profitability in FY25, with earnings per share (EPS) rising 79.9% year-on-year to ₹43.43.

This impressive bottom-line growth came despite subdued revenue momentum and was largely driven by margin recovery and operational efficiency gains. Revenue rose a modest 1.9% year-on-year to ₹52,988 crore, reflecting continued weakness in IT spending across key global verticals.

The real improvement came on the cost side. Operating margins expanded from 9% in FY24 to 13% in FY25, thanks to tighter cost controls and a reduction in wage inflation pressures. This 400 basis point margin improvement follows a low point in FY24 and signals progress in the company’s turnaround efforts.

In its latest earnings call, management acknowledged that macroeconomic conditions remain tough, with FY26 expected to be another challenging year due to global headwinds.

Despite this, Tech Mahindra remains focused on its FY27 goals, which include outpacing industry growth, achieving a 15% EBIT margin, and delivering an RoCE of over 30%. The company is banking on its strong deal pipeline to fuel this growth. In FY25, it reported total deal wins of $2.7 billion, up 42.5% from the previous year—a sign of improving client traction.

However, when viewed over a longer time frame, the company’s financial performance has been underwhelming. Over the last five years, revenue has grown at a CAGR of just 8%, while net profit has increased by only 2%. This muted growth reflects sustained macroeconomic pressures in core markets like the US and Europe, as well as competitive pressures from both larger and mid-tier IT rivals.

Also read: China’s rare earth crackdown: Time to rethink these Indian EV stock holdings?

Tech Mahindra’s return ratios also lag behind its peers. Its RoE stands at 15.7% and RoCE at 20.1%—both lower than industry leaders like TCS and Infosys. Even some mid-cap IT firms, such as HCL Tech and Persistent Systems, have posted stronger capital efficiency metrics.

While recent deal momentum is encouraging, the company still has considerable ground to cover to match the operational and financial performance of its top-tier competitors.

That said, brokerage firm Sharekhan remains optimistic. It has maintained a ‘BUY’ rating on Tech Mahindra, revising its target price to ₹1,650. The firm believes that despite the broader industry slowdown, the company has made meaningful progress and is now on firmer footing to narrow the performance gap with its larger peers.

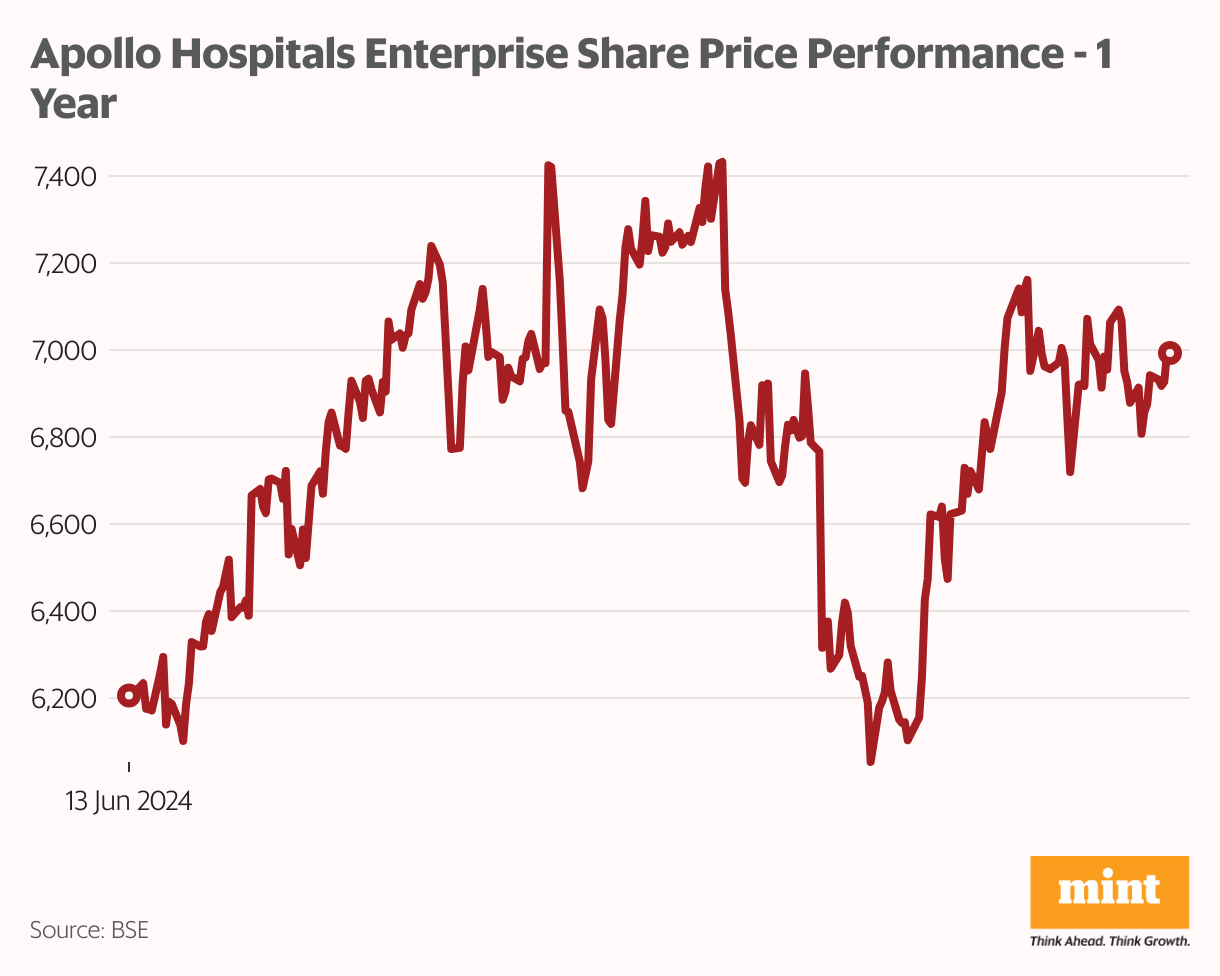

Apollo Hospitals Enterprise

Apollo Hospitals Enterprises, one of India’s largest integrated healthcare service providers, reported a strong performance in FY25, with earnings per share (EPS) rising 61% year-on-year to ₹100.56.

The growth was driven by better asset utilization, margin expansion, and a solid performance across its hospital and pharmacy distribution businesses.

Revenue grew 14.3% YoY to ₹21,794 crore, supported by strong demand across key verticals including tertiary care, diagnostics, and the digital platform Apollo 24/7. The post-pandemic trend toward organised healthcare and wellness services also continued to support overall business momentum.

Operating margins improved by 100 basis points—from 13% in FY24 to 14% in FY25—reflecting tighter cost controls and stronger pricing power, particularly in specialized care offerings.

Looking ahead, Apollo has laid out an ambitious growth plan focused on expanding its integrated healthcare ecosystem while maintaining profitability. The company plans to invest over ₹8,000 crore to add 4,300 beds over the next 3–4 years. Of this, ₹1,000 crore has already been deployed, with the remaining capital expenditure to be funded largely through internal accruals. Apollo’s healthy free cash flow generation—exceeding ₹1,000 crore annually—offers a strong foundation for self-financed growth.

Over the past five years, Apollo has posted consistent financial gains, with revenue rising at a CAGR of 14%, and net profit growing at a much stronger 37% CAGR. This has been supported by rising operating leverage across business verticals.

The company’s return metrics are also impressive: its RoE stands at 19.1%, while RoCE is 17.1%—both well above the industry median. Its RoE is among the top three in the sector, and its RoCE exceeds its cost of capital, which helps justify its expansion-led strategy.

That said, Apollo’s debt-to-equity ratio is relatively high at 0.96x—currently the highest among major listed hospital chains. While this adds some financial risk, the company’s strong cash flows and internal capital generation help mitigate the concern.

Management has also expressed confidence in maintaining momentum in FY26, aiming to sustain hospital margins at around 24%, even as new facilities come online.

Brokerage firm Motilal Oswal has a ‘BUY’ rating on Apollo Hospitals with a target price of ₹8,050. It expects upcoming bed additions, narrowing of losses at the health-tech level, and a turnaround in diagnostics to support earnings growth in the coming quarters.

Hindalco

Hindalco Industries, one of India’s leading producers of aluminium and copper, capped off FY25 with a record performance. The company reported an EPS of ₹71.20, marking a 57.6% year-on-year increase.

Net profit climbed to an all-time high of ₹16,002 crore, buoyed by higher volumes, an improved product mix across both aluminium and copper businesses, and easing input costs. A stable interest burden and consistent tax rate further supported bottom-line growth.

Revenue grew 10.4% YoY to ₹2,38,496 crore, aided by resilient domestic and export demand across industrial and packaging segments. Despite global commodity volatility, Hindalco benefited from favourable pricing trends and continued operational efficiency.

Operating margins also improved from 11% to 13%, reflecting better realizations and tighter cost controls—particularly in its Novelis subsidiary and India’s upstream operations.

Looking forward, Hindalco has set its sights on scaling up production in both its aluminium and copper divisions. The company aims to quadruple downstream Ebitda by FY30 compared to FY24, with significant investments planned to support this target.

A key initiative includes securing raw materials by acquiring the Bandha coal mine, which will ensure coal supply to its Mahan smelter for the next 45 years.

For FY26, the company has earmarked capital expenditure of ₹7,500–8,000 crore, with even higher outlays projected for FY27 as large-scale projects take off. With cash and cash equivalents of ₹10,846 crore, Hindalco remains well positioned to fund this expansion without excessive reliance on debt.

Over the last five years, the company has delivered robust financials, with revenue and net profit growing at compound annual growth rates (CAGR) of 15% and 34%, respectively.

Hindalco’s return metrics reflect its operational strength, with RoE at 14.5% and RoCE at 15.2%—well above most mid- and small-cap aluminium peers, though slightly below NALCO’s levels.

Its debt-to-equity ratio stands at 0.52x, in line with the industry average and significantly lower than more leveraged players like Arfin and Euro Panel. Strong internal accruals provide a cushion for upcoming capex cycles, keeping leverage in check.

However, emerging risks remain. Crisil Ratings recently flagged U.S. tariffs on aluminium imports from Canada and Mexico—countries that supply raw material to Novelis' U.S. plants—as a potential supply chain headwind. The management has clarified that any price increases due to these tariffs will be passed on to customers, helping safeguard margins.

Brokerage ICICI Securities has a ‘BUY’ rating on Hindalco with a target price of ₹770, citing its strong operating performance, comfortable leverage, and robust growth outlook.

Conclusion

In a year clouded by macroeconomic uncertainty, erratic consumption patterns, and sector-specific headwinds, these five companies—Bharti Airtel, Adani Enterprises, Tech Mahindra, Apollo Hospitals, and Hindalco—have stood out by delivering strong earnings growth. Their performance has been anchored by margin expansion, strategic capital allocation, and operational discipline.

Yet, investors should look beyond the headline EPS figures. Ambitious capex plans, rich valuations, and risks ranging from telecom debt and global tariffs to regulatory scrutiny and competition all merit careful scrutiny.

As the Indian economy enters a new phase of growth and adjustment, the ability of these companies to sustain their momentum—and manage volatility—will determine their long-term value creation.

Also read: Battery energy storage stocks: A small-cap watchlist

About the author:

Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India. She is a certified Financial Risk Manager (FRM) and is working toward the Chartered Financial Analyst (CFA) designation.

Disclosure:The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.