Markets

Markets

These are the five fastest-growing Indian stocks

in the past five years.")

Summary

- High-growth companies can be attractive investments as their stock prices can shoot up quickly. However, its best to treat them with caution as their stocks can be extremely volatile during uncertain times.

Investors are always looking for stocks with exceptional growth potential, particularly those capable of accelerating revenue growth and profitability.

When evaluating growth stocks, key factors to look for include robust revenue expansion, strong profit growth, impressive return ratios, and consistent dividends. This article highlights five rapidly growing stocks that exemplify these traits and offer promising opportunities across various sectors.

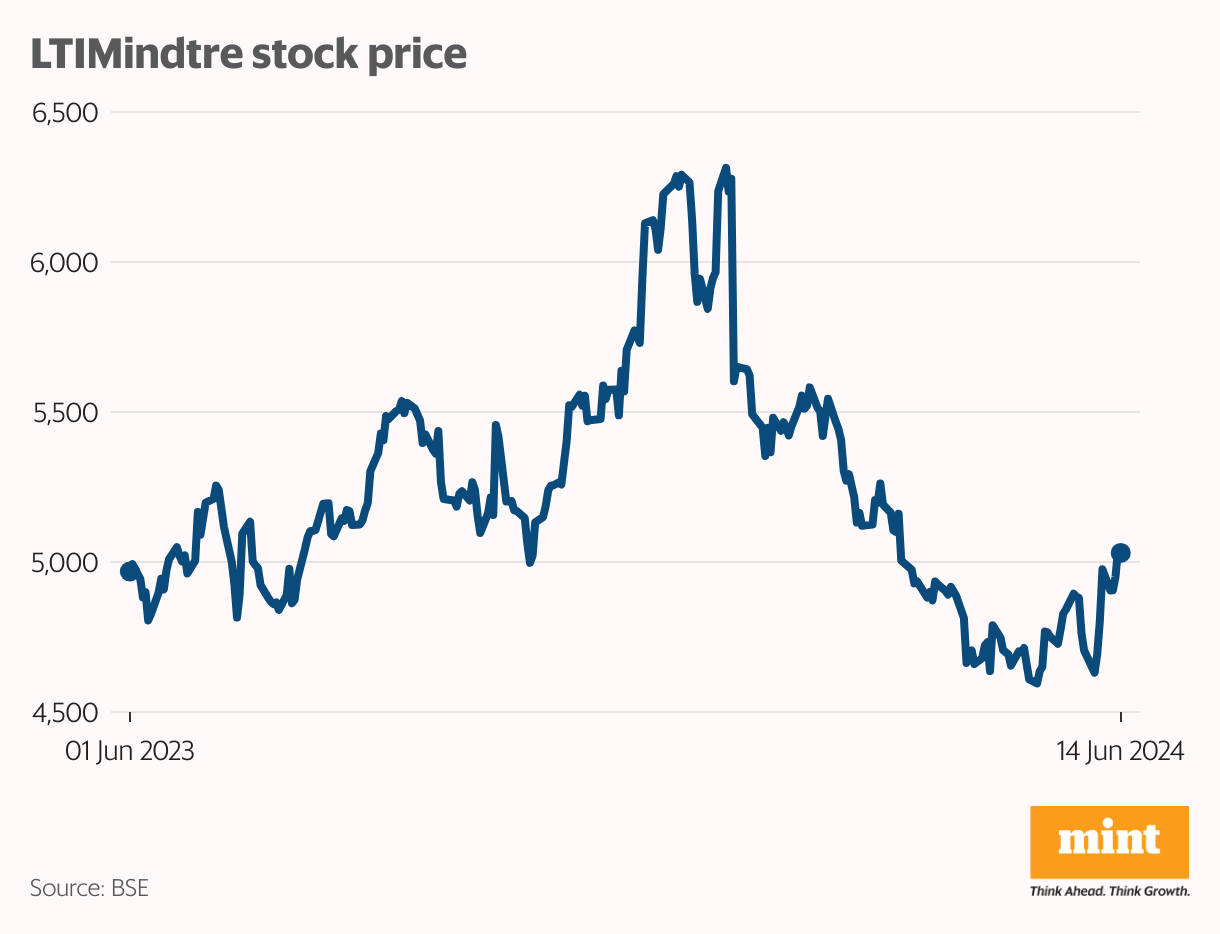

LTIMindtree

Larsen & Toubro Infotech and Mindtree merged in 2022 to become India's sixth-largest IT services company. It primarily offers IT services such as application development, maintenance, outsourcing, enterprise solutions, infrastructure management, and digital solutions.

Its principal business verticals are banking, finance and insurance, manufacturing, media, retail, travel, hospitality, and healthcare. The company has more than 700 clients across 30 countries.

In the past five years, sales have grown at a compound annual growth rate (CAGR) of 26.7%, driven by healthy deal wins, improved cross-selling and up-selling opportunities, and an increased ability to bid for large deals.

Earnings before interest, tax, depreciation, and amortisation (Ebitda) and net profit grew at a CAGR of 25.8% and 24.7%, respectively, due to high employee utilisation and client additions. Although profit margins fell slightly owing to merger-related integration costs, return on capital employed (RoCE) and return on equity (RoE) averaged 27% and 37%, respectively.

The company also has zero debt and pays large dividends to shareholders. Over the past five years, the dividend payout and dividend yield averaged 35% and 1.3%, respectively.

Currently, the company is focused on cross-selling and up-selling opportunities to win new deals and acquire more clients. It is also looking at improving profit margins by reducing discretionary spending and tail rationalisation – focusing on the most profitable projects and eliminating the least profitable ones.

It these efforts are successful, investors can expect strong revenue and profit growth.

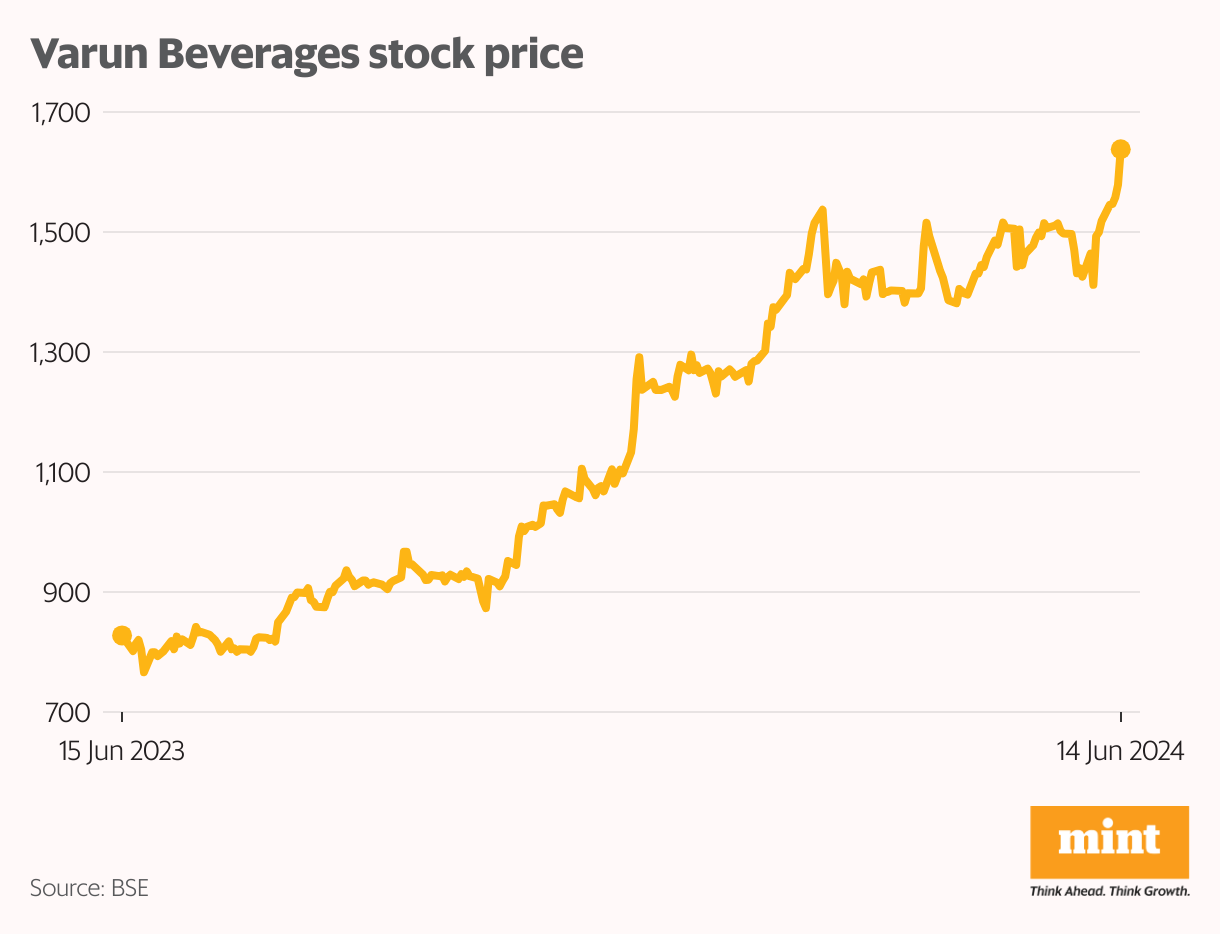

Varun Beverages

One of the largest franchisees of PepsiCo worldwide, the company produces and distributes a wide range of carbonated and non-carbonated drinks and packaged water. It sells popular brands such as Pepsi, Seven-Up, Mirinda, Mountain Dew and Tropicana.

The company has 43 manufacturing facilities in India and abroad, and a robust distribution network of more than 110 owned depots, 2,500 owned vehicles, 2,400 primary distributors, and 925,000 visi coolers.

Its robust distribution network has given it a unique advantage, helping it become the market leader and grow its sales at a CAGR of 17.6% over the past five years.

Varun Beverages also has large facilities with backward integration for producing crowns, plastic closures, corrugated boxes and shrink-wrap film. This has helped it cut costs and grow Ebitda and net profit at a CAGR of 19.9% and 34.8%, respectively.

Profit margins have also expanded over the past few years due to operational efficiencies. The five-year average Ebitda and net profit stand at 20.6% and 9.2%, respectively. RoE and RoCE have also expanded consistently, with the five-year average at 20.7% and 22.6%, respectively.

Although not a huge dividend payer, the company pays regular dividends to its shareholders. In the past five years, the dividend payout and dividend yield averaged 9.6% and 0.2%, respectively.

As one of the largest franchisees of PepsiCo, the company has worked on improving its network and expanding its production facilities. In December 2023, it laid the foundation for its 44th manufacturing facility with a capital expenditure of ₹2.7 billion, and also plans to set up three new manufacturing facilities in Maharashtra, Jharkhand, and Odisha. It has also acquired franchisee rights in South Africa as part of its international expansion.

Going forward, both revenue and profitability are expected to grow in the medium term.

Titan

Titan, part of the Tata Group, is one of India's most respected lifestyle companies. Its established products include watches, eyewear and jewellery, and it recently expanded into fragrances, bags and apparel.

The company owns several popular brands such as Skinn, Fastrack, Titan Eye+, Tanishq, and Sonata. It is the world's fifth-largest watch manufacturer and accounts for more than 6% of India's jewellery market.

Titan has an extensive network of outlets across product categories, including 898 jewellery outlets, 1,080 exclusive and 8,000 multi-brand watch outlets, and 975 eye-wear outlets. It also has a presence in more than 200 large stores for its emerging businesses. It operates in more than 40 countries.

Strong distribution networks in India and abroad have helped the company clock impressive sales growth of 15.5% (CAGR) in the past five years. Ebitda and net profit grew at a CAGR of 19.5% and 18.7%, respectively, over this period. Profit margins also expanded due to operating leverage and a growing share of high-margin jewellery and watches. As a result, RoE and RoCE also expanded, averaging 21.9% and 32.2%, respectively, in the past five years.

Titan is also known for consistently paying dividends to its shareholders, with a five-year average dividend payout and dividend yield of 29.9% and 0.4%, respectively.

It is also investing in expanding in India and abroad. In the next few years, it aims to expand Tanishq’s presence from 265 towns to 300 towns. It also plans to expand its emerging businesses rapidly to capture the growing demand for apparel. The company’s strong growth plans will drive its revenue and profit growth in the medium term.

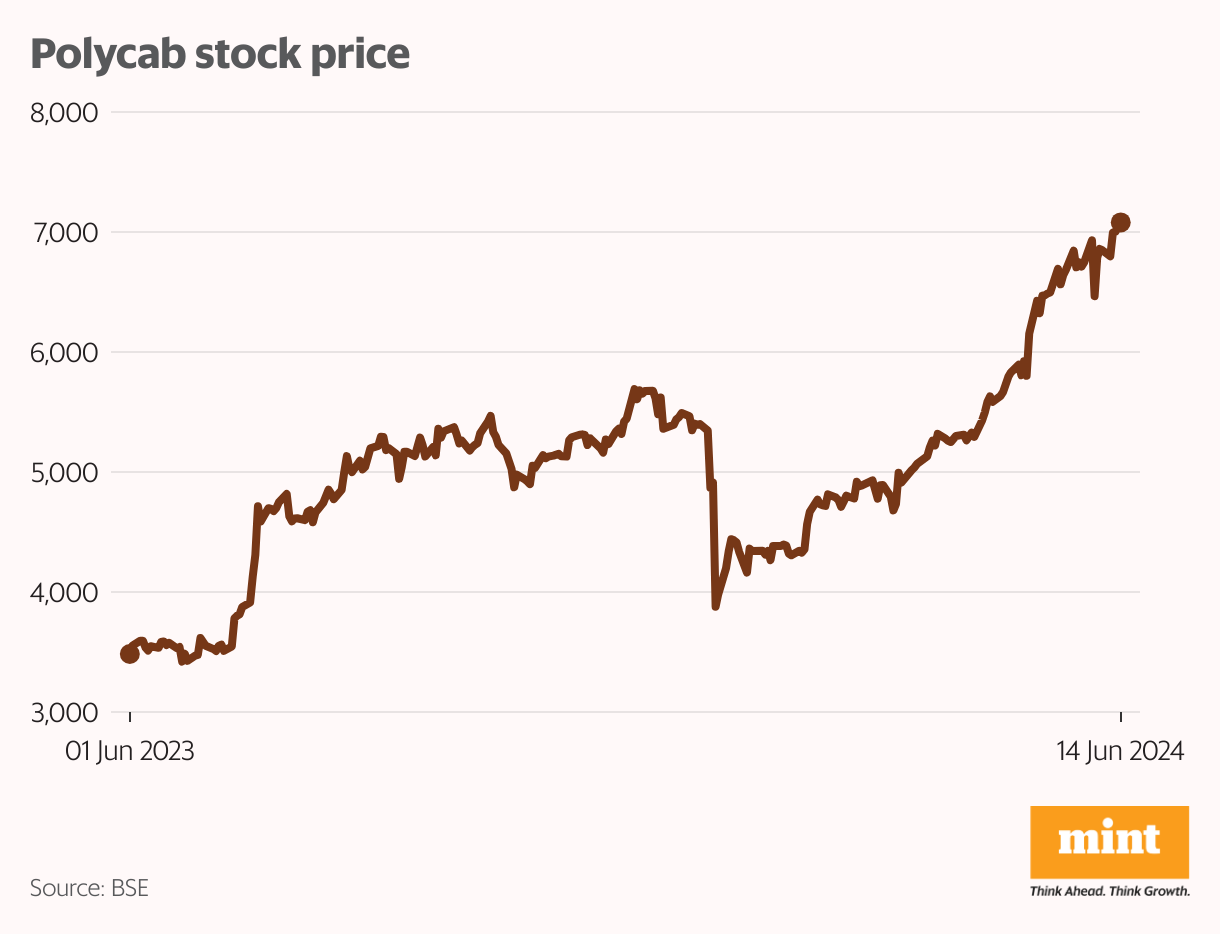

Polycab India

India's leading manufacturer of cables and wires, Polycab has a large portfolio of cables, wires and allied products such as PVC conduits, lugs and glands. It recently entered consumer electrical product segments such as fans, switches, switchgear, LED lights, luminaries, solar inverters and pumps.

The company has a 24% market share in the domestic organised wires and cables sector and is present in more than 76 countries. It has 25 manufacturing facilities, and a network of over 4,300 distributors, 200,000 retail outlets, 23 warehouses, four regional offices, nine local offices, and 17 experience centres in India.

Sales grew at a CAGR of 12.1% in the past five years due to a growing share of the organised cables and wires sector and a large contribution from the consumer electricals business.

Ebitda and net profit grew at a CAGR of 14.1% and 20.7%, respectively, due to the company's ability to pass on increased raw-material costs to its customers. Profit margins thus expanded as well, averaging 12.1% and 8.1%, respectively. RoE and RoCE averaged 18.1% and 25.4% over the past five years.

Polycab India has also consistently increased its dividend payout. The dividend payout and dividend yield averaged 17.6% and 0.7%, respectively, in the past five years.

The company has ambitious growth plans and aims to spend ₹7 billion on capex in each of the next two years.

Three-fourths of this capex will go to the cables and wire business to set up a high-voltage manufacturing plant, and the rest will be allocated to the consumer electricals business for maintenance and removing bottlenecks. It plans to fund the entire capex through internal accruals, indicating that it has adequate liquidity.

The company's expansion plans could further fuel its growth and boost revenue and profits in the medium term.

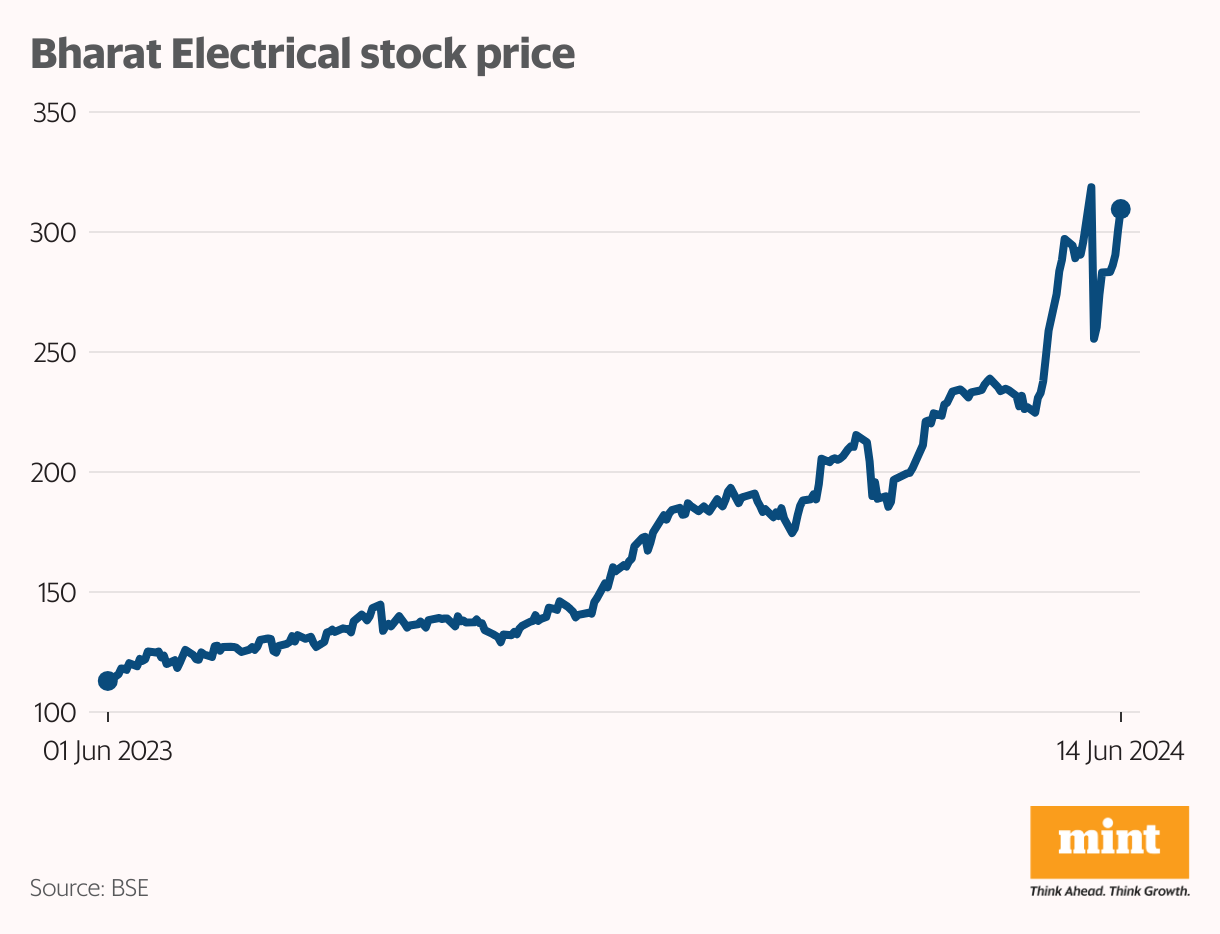

Bharat Electronics

Formed under the ministry of defence, Bharat Electronics is a multi-product, multi-technology conglomerate that provides products and systems to the defence sector.

It has a large product portfolio that includes radars, fire control systems, missile systems, communication systems, tank electronics, and gun upgrades. It recently began producing supplying weapons systems and lithium-ion batteries. It is also undertaking solar power plant projects and has partnered with ISRO for satellite assembly, integration and testing.

It has also secured business from the Security Analytics Center (SAC), and is working on data-diode solutions for DRDO. It also provides an automatic fare collection system for railway and metro projects.

In the defence sector, it works on requirements for drone payloads, data linkages, and ground control stations. It also provides drone guard systems and is developing RF and IR seekers, missiles, and arms and ammunition.

In the past five years, the company’s revenue has grown at a CAGR of 7.8% on account of a large order book. Ebitda and net profit grew at a CAGR of 7.6% and 9.7%, respectively, due to high order execution. Ebitda margin and net margin averaged 21.8% and 15.1%, respectively in the past five years. RoE and RoCE expanded as well, averaging 19.4% and 26.9%, respectively.

Bharat Electronics is also a large dividend payer. Its dividend payout ratio and dividend yield averaged 44.3% and 2.9%, respectively, in the past five years.

While the company is already on its growth path, it has secured several orders from prestigious clients, including the Indian Army. It has also signed contracts to jointly develop long-range, dual-band, infrared search-and-track systems, and a chip factory.

All of this should boost the company’s revenue and net profit in the medium term.

Should you invest in high-growth companies?

High-growth companies are often market leaders in their industries. They can be attractive investments as their stock prices can shoot up quickly. However, the success of these companies depends heavily on prevailing economic conditions, and their stocks can be extremely volatile during uncertain times.

It’s best to treat growth stocks with caution, like any other stock, and consider them only for long-term investment.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com