Trading in derivatives? Get ready to show your grades

- Bourses propose testing knowledge, risk profile of retail investors

Mumbai: Want to trade in derivatives? Take an exam. Also, prove your net worth is high enough to stomach the risks. That, in essence, is what a possible entry barrier to derivatives trading could look like as regulatory concerns continue to play out over the risks of retail investors trading in futures and options contracts.

Two frameworks suggested by stock exchanges to markets regulator Sebi (Securities and Exchange Board of India) for consideration by a proposed committee are understanding the product and its risks, and trading in proportion to one’s net worth (measuring a person’s wealth) through KYC (know your customer) norms at the broker’s end.

A proposed regulatory committee comprising officials of Sebi and stock exchanges could consider these two aspects, according to four market experts aware of the matter.

Although the timeline for setting up the panel or its composition is still unclear as the country heads for Lok Sabha polls, the rise in retail and proprietary speculation across derivatives such as equities, commodities and currencies, until recently, has drawn regulatory concern.

“Under the products framework, an investor should have full knowledge of the product she is trading in," said one of the people cited above on condition of anonymity. “Since index options (Nifty and Bank Nifty contracts) are the most popular product among retail investors, it is proposed that they would have to clear mandatory exams on options every year to be able to trade in derivatives."

He added that under the networth criteria, the trading exposure would be based on a person’s wealth.

“For instance, if a retail participant’s networth is ₹10 crore, she can’t take leverage up to ₹100 crore, which is disproportionate to her wealth."

He drew a parallel to warnings on cigarette packets as a way of informing people about the harmful effects of tobacco. “Sebi mandates risk disclosures on broker contract notes and websites about the risks of derivatives trading. You go with your eyes open after seeing the disclosure pop-up, akin to a smoker smoking after seeing the warning on the pocket."

Queries to Sebi went unanswered till press time. BSE and NSE officials were not immediately available for comment.

A Sebi study in January 2023 showed that nine out of 10 individual traders in the equity F&O segment incurred losses, with active traders ₹50,000 on average in FY22. It also found that the number of individual traders in index and stock options went up by nearly eight and five times each in the past three years. The RBI reinforced Sebi’s finding in its bi-annual financial stability report.

In November, Sebi chairperson Madhabi Puri Buch cautioned small investors against taking huge bets in derivatives, adding investors should focus on long-term prospects of the equity market.

A senior executive from an asset management company said one of the committee’s terms of references could be to deepen the market by increasing institutional participation.

“Currently, proprietary traders and retail investors hold the highest share in equities options trading as well as in currency options, which raised the RBI’s hackles," the executive said. “There is a need to increase hedging activity and, to this end, we could see some changes to attract institutions to hedge more. Currently, MFs, for instance, can take derivatives exposure commensurate with their underlying portfolio exposure."

A senior broking official said that the KYC done at the broker’s end would be strengthened to better know the client. The details of networth, awareness, etc. would probably be added to existing details sought on income bracket levels, age, etc., he said, as regulators were concerned about the “rising phenomenon of speculation among retail investors".

Indeed, the share of proprietary traders as a proportion of gross notional turnover on NSE, which commands a 91% market share in derivatives, rose to 59.6% in the 11 months of FY24 (April-February) from 52.7% in the corresponding period of the earlier fiscal.

The share of retail, however, fell over the same period to 26.3% from 27.9%. DII share was steady at 0.1% and FPI share fell to 5.9% from 7.4% over the same period. DII and FPI refer to domestic institutional investor and foreign portfolio investor, respectively.

However, another broker said the very narrative of using notional turnover presented a “misleading picture".

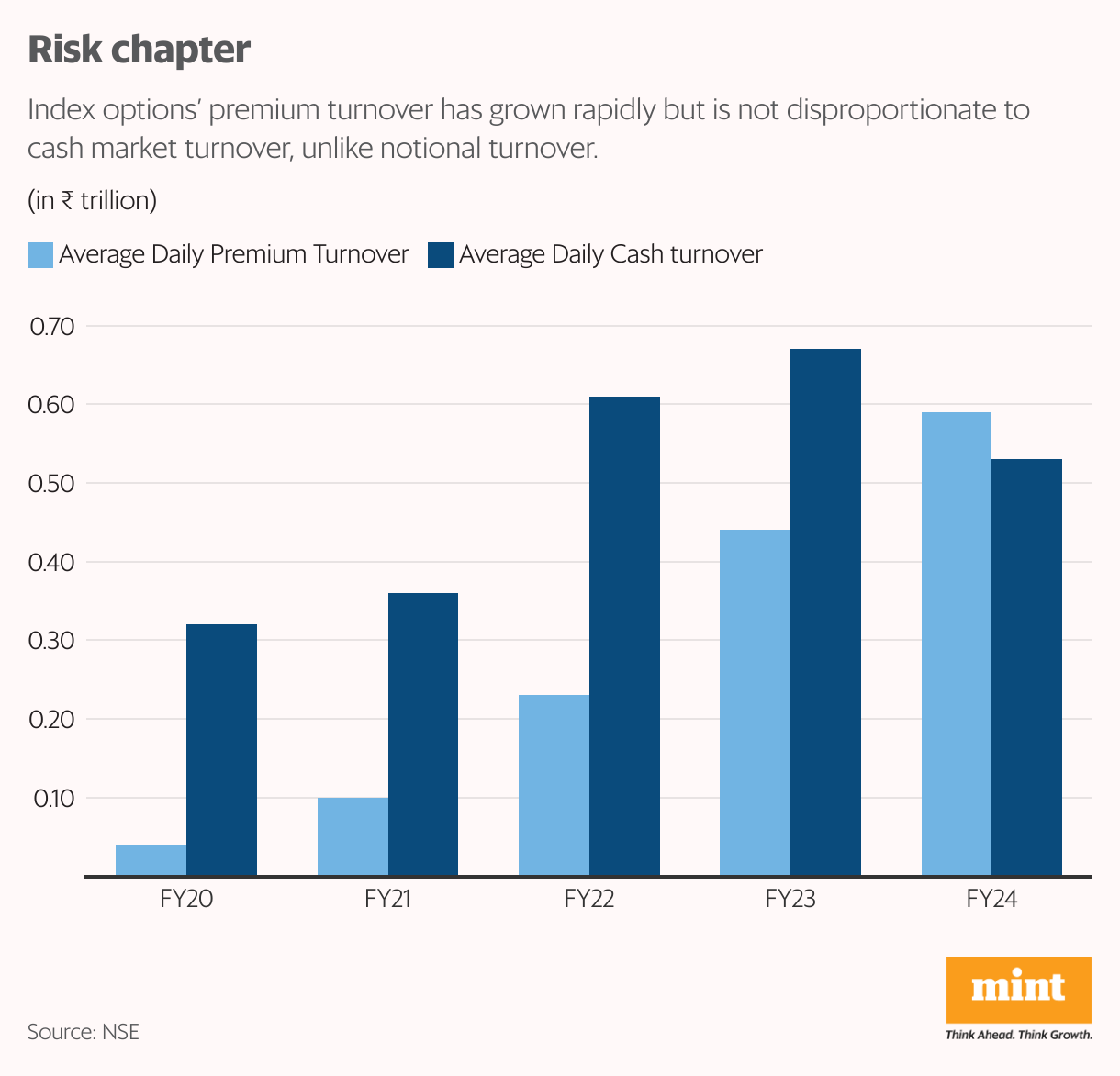

“The notional turnover of options portrays an unrealistic depiction of trading participation," said Tejas Khoday, co-founder and CEO of online discount broker Fyers. “The premium turnover, on which exchange transaction charges and taxes like STT (securities transaction tax) are based, is the better way to view the derivative turnover figures, which is a fraction of the notional turnover. Albeit, premium turnover has been growing at a fast pace, it is still less than cash market volumes till date."

Notional value is the total value or worth of an asset while premium turnover is market value. In FY24, the average daily notional turnover of index options was ₹339 trillion while the premium turnover was just ₹0.6 trillion.

The average daily cash market volume was ₹0.53 trillion. The notional turnover is 640 times the cash turnover, but the premium turnover is just 1.1 times the cash turnover.

While banks’ retail loans grew at a compounded 25.5% between September 2021 and September 2023, unsecured retail lending grew by 27%. Some fears were raised that a portion of unsecured loans found their way into options trading. However, Khoday dispelled such claims.

“Rather than retail participants using unsecured loans to dabble in options, it’s more likely that proprietary traders could have leveraged their capital by pledging their securities as collateral to trade in the derivatives segment," Khoday said, citing the fall in retail participation in FY24 from the preceding fiscal.