Trent’s 1,000% rally takes a breather. Can a Sensex rejig revive its fortunes?

")

Trent’s 39% revenue growth in FY25 is nothing short of exceptional. But when factoring in valuations, the story turns sour.

Trent Ltd, the Tata Group’s multibagger fast-fashion company, is having a tough time. After rallying more than 1,000% in the previous five years, concerns around competition and valuation have humbled the stock this year. So far this year, Trent has lost nearly 22%, while the benchmark Nifty 50 index has appreciated 5%.

But Trent’s fortunes looked up last week when the Sensex rejig was announced. After making it into the Nifty 50 index in September, Trent is set to replace Nestle India Ltd in the 30-stock Sensex, effective 23June. The Trent stock rallied by as much as 3% following the announcement.

With Trent set to have about a 1.5% weight in the Sensex, its inclusion is expected to bring about $300 million of inflows from passive funds linked to the index. But can the liquidity push brush off the fundamental concerns plaguing the stock?

Cannibalization ate away at growth in Q4

In the latest reported quarter, Trent logged a 9.7% sequential decline in revenue to ₹4,334 crore. Of course, the January-March quarter is seasonally slow for Trent, and some decline from the preceding three festive months was expected.

But even compared with the company’s performance in the fourth quarter of 2023-24, Trent’s latest quarterly revenue growth had moderated—to 29% from about 75% a year earlier. This marked a continuation of a slowdown Trent has witnessed throughout 2024-25.

Why? Like-for-like growth—or sales growth across existing stores—dropped from high-single digits in Q3 to mid-single digits in Q4. Annualized revenue per store was flat year-on-year at ₹16.8 crore. The management attributed this to store expansion and “densification" in certain micro markets.

In other words, Trent’s existing stores’ sales are being cannibalized by its own new stores. Notwithstanding the management’s argument that the company is building proximity to consumers by increasing store density, if store-expansion does not come with like-to-like growth, it is only a matter of time before margins get stressed.

Full-year growth was decent despite competition

Competition has been intensifying across businesses for Trent. In its fashion segment, Reliance Retail Ltd’s Yousta, Aditya Birla Fashion and Retail Ltd’s Style-Up, and Shoppers Stop Ltd’s InTune have been weighing on Trent’s prospects. In what could add fuel to the competitive fire, there have been reports of Reliance Retail relaunching China’s popular fast fashion brand Shein in India.

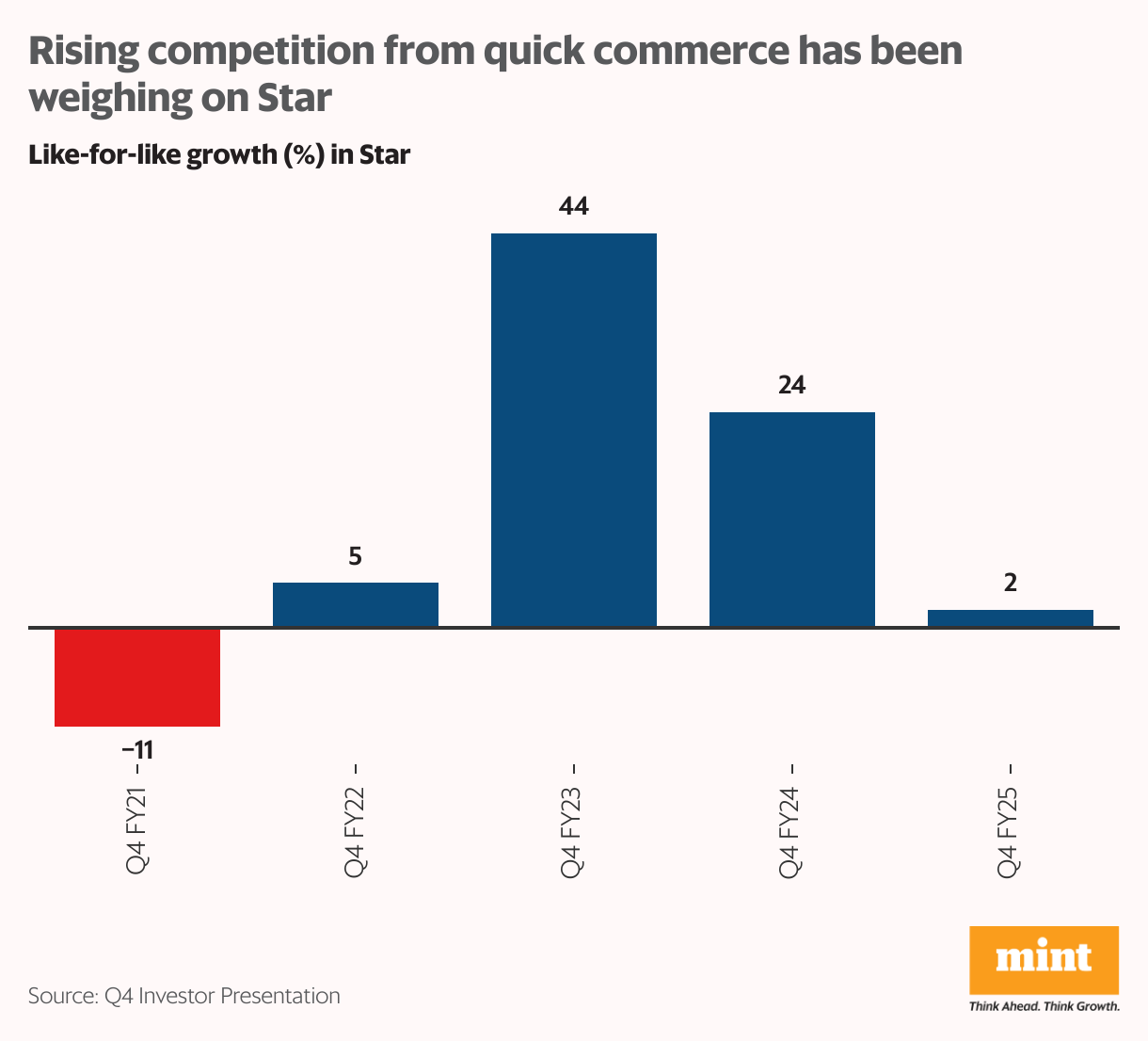

As for Star, Trent’s food and grocery segment, quick-commerce has been rising as a threat. Like-for-like growth in Star slowed to 2% in Q4 from nearly 25% a year earlier. If this persists, it will become increasingly difficult for Trent to profitably scale Star.

Trent’s full-year volume and revenue growth were in the ballpark of 40%. Like-for-like growth during the financial year was in double digits. Emerging categories such as beauty and personal care, and footwear also gained traction, accounting for 20% of the company’s full-year revenue.

Margins remained resilient

As Trent’s like-for-like growth slowed in Q4 its operating leverage took a hit even as store expansion continued. Gross margins also compressed more than expected, possibly due to aggressive discounting for clearing out inventory as well as inventory write-offs.

But on the bright side, other operating costs moderated. Franchisee sales increased, while shutting down non-performing stores helped optimize occupancy costs. As a result, rental expenses witnessed slower growth than the topline. Finance and employee costs also reduced as a proportion of revenue, further supporting margins.

Consequently, Trent’s margin on its profit before tax (excluding exceptional items) expanded by 130 basis points in 2024-25. This beat expectations, as analysts had expected a 30-bps contraction. Ebitda grew 37% year-on-year to ₹656 crore in Q4.

But owing to ₹543 crore of exceptional gains reported in the base quarter, Trent’s standalone profit after tax fell 46% year-on-year. Losses from associates led to a sharper 55% drop in consolidated PAT. The full-year saw PAT expand by 38% to ₹18,141 crore.

Good, bad, and ugly of store expansion

Trent had a widespread retail footprint with 765 Zudio stores, 248 Westside stores, and 30 stores across other lifestyle concepts as of March, taking its total fashion stores to more than 1,000.

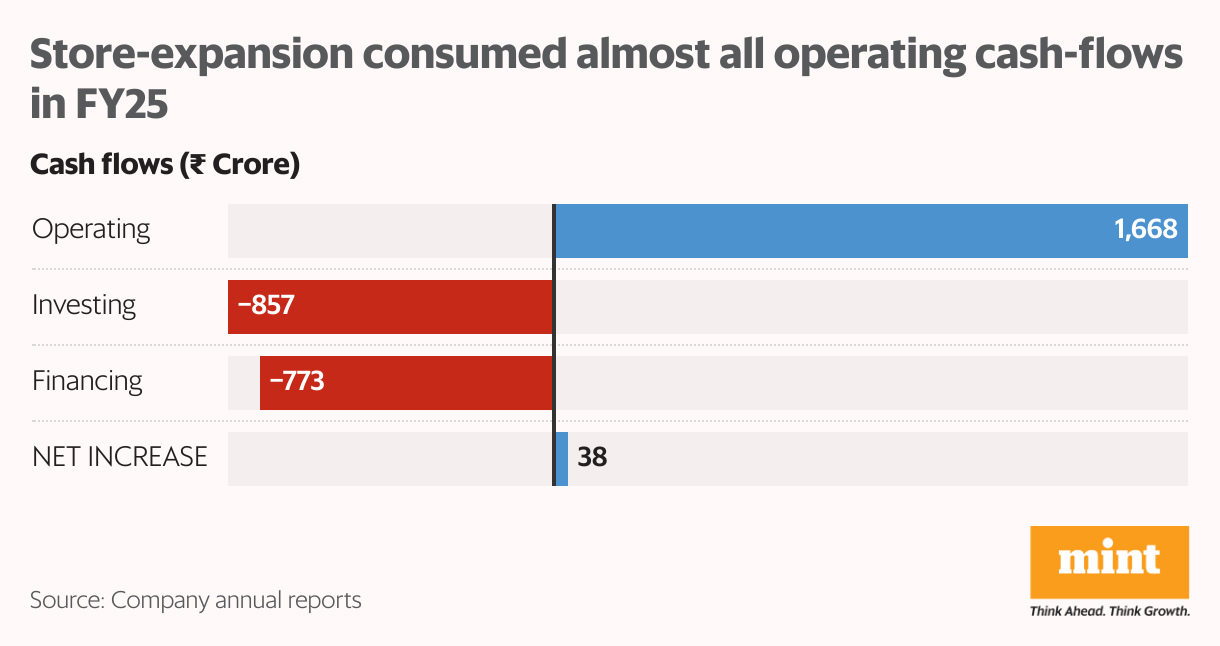

Expansion in FY25 surpassed Trent’s planned 200-odd stores for the year. So FY25 saw operating cash-flows all but consumed by expansion-related outflows.

But while the company net added 16 Westside stores for and 220 Zudio stores in FY25, 140 of these stores were added in Q4 alone. Their full benefit can be expected to flow in from Q1 FY26 (the ongoing April-June quarter).

Moreover, in anticipation of a pickup in urban demand, Trent has added large stores, particularly for Westside. but as the company expanded into 64 new cities in FY25, differences in local fashion sensibilities could lead to slower inventory turnover and even write-offs. Cannibalization is also a key risk.

Well-positioned to capture tailwinds

Trent was established in 1998 with Westside. But the business turnaround came with its value fashion Zudio stores.

India’s growing middle-class, ongoing recovery in rural demand, and eventual return of urban demand are tailwinds for the fast-fashion industry. Catalysts for demand could include the tax-cuts announced in the Union Budget for 2025-26 and the 8th pay commission announced for government employees.

Trent is well-positioned to capture these tailwinds and effectively cater to India’s cost-conscious middle-class consumers. Not only has it cracked the design sensibilities of the target consumer, it also has the wherewithal to offer these trending designs at affordable prices, and quickly. All the while keeping its margins strong.

Also read | Institutional investors are betting big on Patanjali. Should you?

Over the years, with Westside and the partnership with Zara, Trent has built an enviable procurement and supply-chain network. As per reports, Zudio’s inventory turns over in 15 days, against 45-60 days for its competitors. This not only helps Trent keep up with fast-changing fashion trends, but is also crucial in containing costs.

Bulk-manufacturing, focus on private labels or in-house brands, and cost-effective influencer-led marketing have also helped Trent keep a lid on costs.

Faster inventory turnover, small stores, and a healthy mix of owned and franchisee stores have led to quicker breakeven of new stores despite lower gross-margins in fast fashion. This has allowed for faster store expansion.

Trent also has a long runway for growth given its low single-digit market-share.

Also read | This Murugappa Group stock is down 38% from its peak. But why are investors turning bullish again?

Problem with pricing to perfection

Trent’s 39% revenue growth in FY25 is nothing short of exceptional. But when factoring in valuations, the story turns sour.

The stock is trading at 127 times its earnings. It has been priced to perfection, with its previously seen supernormal growth being extrapolated into the future. So even small disappointments have led to sharp corrections.

In this context, Trent’s inclusion in the Sensex alone is unlikely to bring about a sustained rally. Estimated passive fund inflows into the stock amount to hardly 1.5% of Trent’s market capitalization.

Progress on store expansion, like-for-like growth, improved margins, and higher cash-flows should help Trent hold on to its evolving position amid intensifying competition. Its entry into international markets, the cluttered beauty segment, and the lab-grown diamond market will also need to be monitored.

Also read | IDFC’s growth hits a speed bump. Is the stock’s bounce-back at risk?

Ananya Roy is the founder of Credibull Capital and a Sebi-registered investment adviser.

Disclosure: The author holds shares of some of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.