Vodafone Idea’s revival plan adds equity, but erodes shareholder value

")

- Vi’s equity swap trims dues but deeply dilutes shareholders. With mounting liabilities and ongoing subscriber losses, its survival now hinges on Arpu growth, 5G rollout, and sustained government backing.

The Indian government just doubled its bet on Vodafone Idea (Vi). But it may be retail investors left holding the bag.

After bailing out the debt-laden telco in 2023 by converting ₹16,133 crore of interest dues into equity, the government is now set to nearly double its stake to 49% by converting another ₹36,950 crore in spectrum dues.

The move aims to keep Vi afloat and preserve competition in the telecom sector—but comes at a steep cost to shareholders, whose stakes will be heavily diluted.

Let's unpack the details.

Deal terms at a glance

The latest support was triggered by Vi’s liquidity concerns. The company informed the Department of Telecommunications that it was unable to furnish either a ₹6,091 crore bank guarantee or ₹5,493 crore in cash—both related to a shortfall from the 2015 spectrum auction.

Vi’s chief exective Akshay Moondra requested government intervention to ease the cash flow burden ahead of rising regulatory obligations.

Read this | After a new lifeline, Vodafone Idea searches for a new CEO

Initially, the government asked Vi to raise funds independently. But it later agreed to convert deferred payments on adjusted gross revenue (AGR) and spectrum usage charges into equity—six months ahead of the moratorium's scheduled end.

How the equity dilution plays out

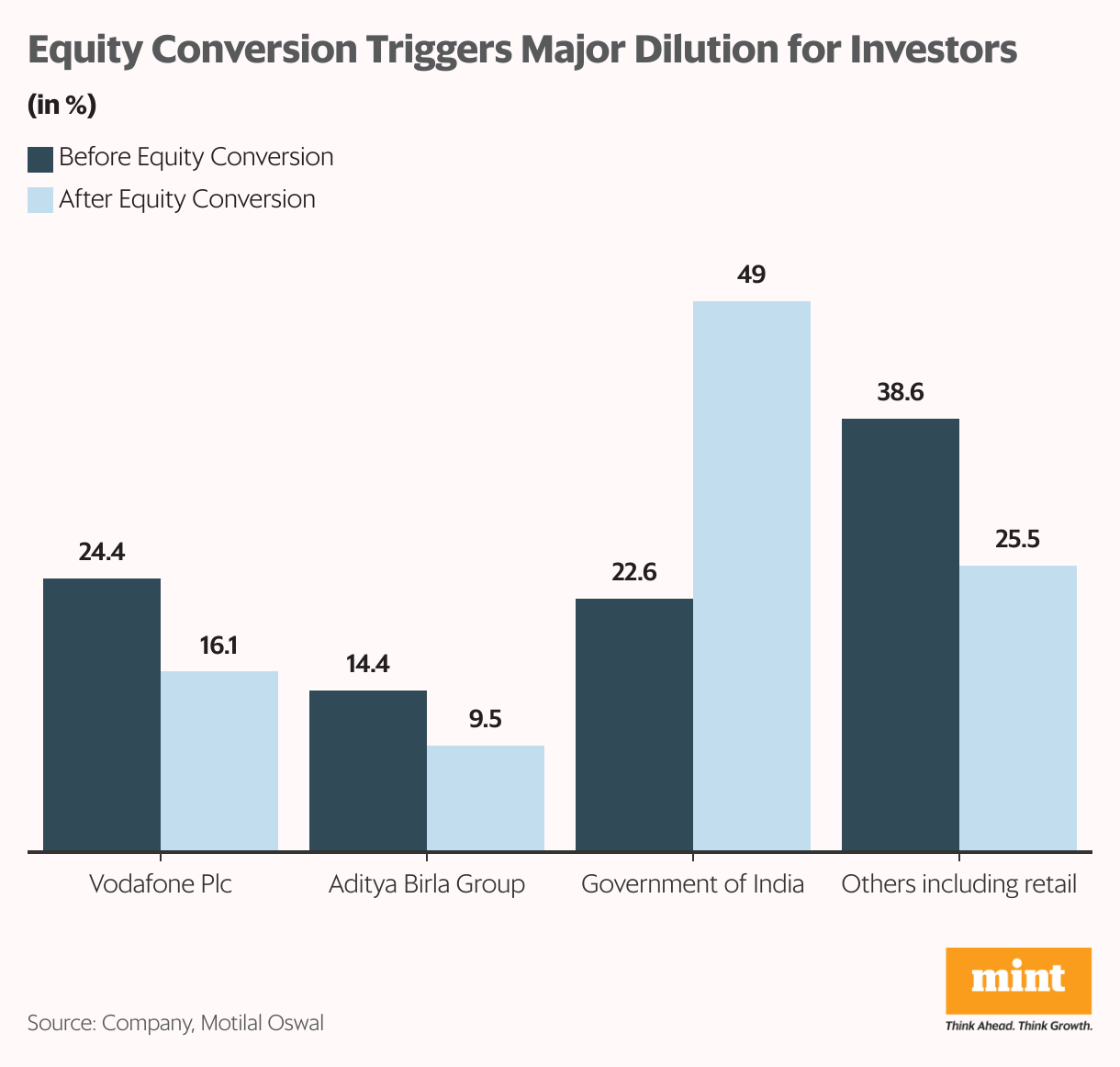

Under the revised arrangement, Vi will issue 3,695 crore equity shares to the government at ₹10 per share. This will double the government’s stake from 22.6% to 49%. Normally, such an increase would trigger an open offer under Securities and Exchange Board of India's (Sebi) takeover rules, but the regulator has granted an exemption.

With the government set to become the largest shareholder, existing stakes will be heavily diluted. Vodafone Plc’s holding will fall from 24.4% to 16.1%, while the Aditya Birla Group’s stake will shrink from 14.4% to 9.5%. The collective shareholding of other investors, including retail, will decline from 38.6% to 25.5%.

For shareholders, this means substantial value erosion.

Vi’s total outstanding shares will increase from 7,139 crore to 10,834 crore. To generate even ₹1 in earnings per share, the company would need to post a net profit of ₹10,834 crore—a tall order for a firm still mired in losses. Even if Vi returns to profitability, the expanded equity base will make it difficult to generate meaningful returns for shareholders.

Heavy liabilities still loom

Despite the conversion, Vi remains burdened with substantial liabilities.

According to Motilal Oswal, Vodafone Idea was scheduled to pay ₹67,000 crore in spectrum dues between FY26 and FY28. The latest equity conversion reduces this burden by ₹42,000 crore in net present value terms. As a result, the actual cash payout required during this period may drop to around ₹8,000 crore.

This comes on top of annual payments of ₹2,200 crore for spectrum acquired during 2021–24. With an estimated annual cash Ebitda of ₹9,000 crore, Vi may be able to cover these obligations through the first half of FY28. However, starting March 2026, the company faces an annual outgo of ₹16,500 crore—a figure that far exceeds current cash flows.

Read this | Why govt’s Vodafone Idea stake will hasten telecom tariff hikes

These numbers suggest that Vi may again require financial assistance in the coming years. But with the government’s stake already at 49%, any further equity conversion risks turning Vi into a state-run enterprise.

IIFL Securities estimates that converting all remaining liabilities could raise the government’s ownership to 81%—a scenario the government is unlikely to welcome.

Subscriber churn continues

While the equity conversion provides Vi with temporary breathing room, the company’s long-term viability depends on retaining subscribers and increasing average revenue per user (Arpu). Vi continues to lag behind Jio and Airtel in rolling out 5G services, contributing to subscriber attrition.

Its market share has steadily declined, with the subscriber base falling to 18.4% in Q2FY25 from 19.8% in Q2FY24. Revenue market share has similarly dipped to 16.4% from 18.2% over the same period. Arresting this churn will be crucial to sustaining operations.

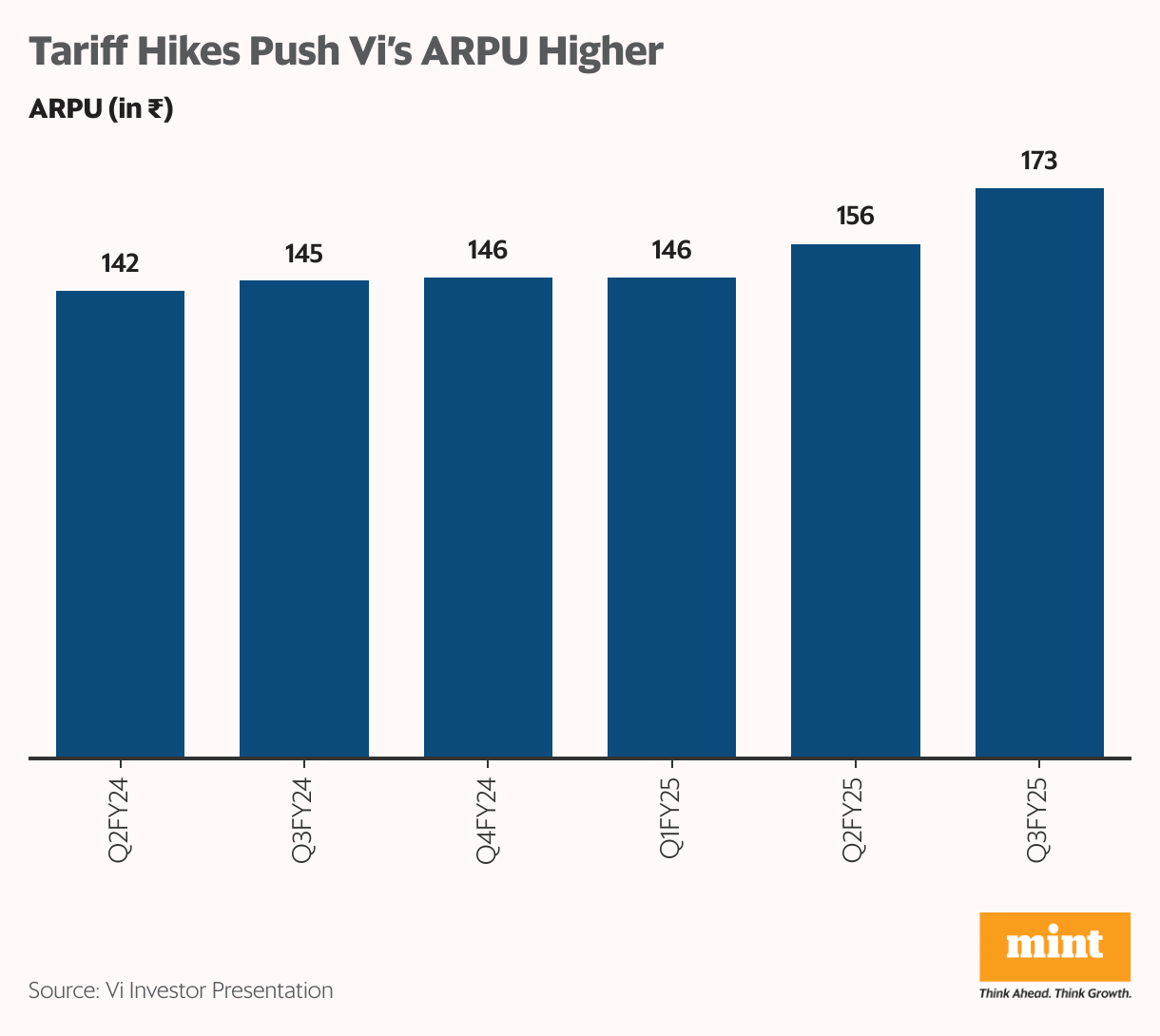

Arpu growth offers short-term relief

On a positive note, Vi’s ARPU has increased for 14 consecutive quarters, largely driven by tariff hikes. ARPU rose from ₹149 in Q2FY24 to ₹173 in Q3FY25, aiding revenue growth despite subscriber losses. Yet, Vi continues to trail its rivals—Airtel reported an ARPU of ₹245 and Jio ₹203, owing to broader 5G availability and stronger customer retention.

Analysts believe continued tariff hikes could help bridge the gap. JM Financial estimates that Vi must increase ARPU to ₹380 by FY28 to meet obligations between FY28 and FY31. Ambit Capital projects a 15% tariff hike in 2025, followed by a 10% compounded annual increase through FY33 to stabilise Vi’s finances.

These projections, however, may be overly optimistic. Since 2019, Vi’s cumulative tariff hikes amount to 67%, and further increases without corresponding improvements in service—especially in 5G—may not be sustainable. Without network upgrades, subscriber churn will likely persist, undermining efforts to raise ARPU meaningfully.

What’s next?

Despite its fragile state, Vodafone Idea remains a key player in India’s telecom market, with a sizable user base and infrastructure. Its collapse would effectively reduce the sector to a duopoly—a scenario neither the government nor the industry wants.

This partly explains the continued government support. Yet, even after the latest intervention, Vi faces mounting obligations and operational challenges. It remains uncertain how far the government is willing—or able—to go to keep the company afloat.

For more such analyses, read Profit Pulse.

Meanwhile, state-run Bharat Sanchar Nigam Ltd (BSNL) is preparing to launch 5G services in 2025, backed by ₹3.2 trillion in government funding. Whether it emerges as a viable alternative or whether both BSNL and Vi manage to stage a comeback remains an open question.

About the Author: Madhvendra has been a passionate follower of the equity market for over seven years and a seasoned financial content writer. He loves reading and sharing his opinions about listed Indian companies and macroeconomic trends.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.