Amusement parks are a brutal business. Has this company cracked the code?

Summary

- Wonderla Holidays has leveraged its brand presence, conservative expansions, and cost efficiencies to fly ever higher in a highly seasonal and unforgiving industry. Is its stock worth watchlisting?

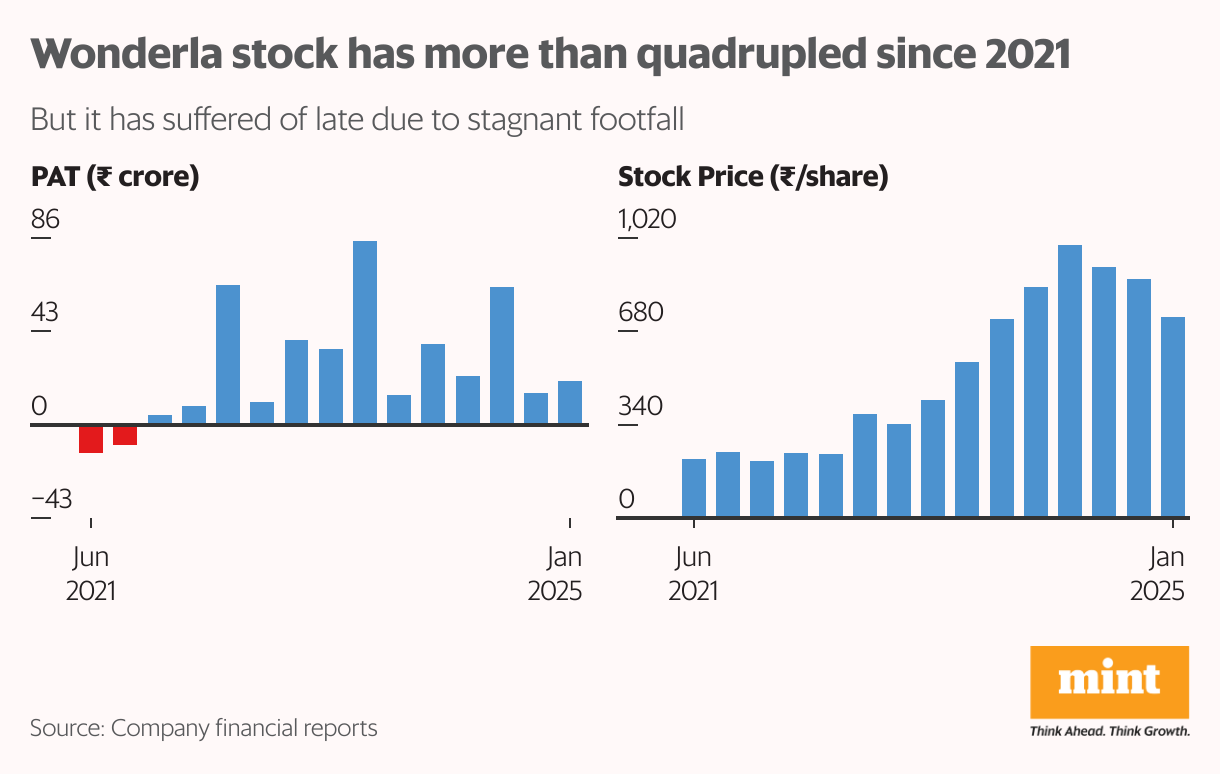

Wonderla Holidays is a multibagger, having delivered a 350% return in less than two years leading up to the end of 2023. The boost in investor sentiment followed upbeat fundamentals since the June 2022 quarter.

Even before that, Wonderla was a strong counter, having delivered a robust 15% compound annual return in the five years leading up to the pandemic. Established in 2000 by the founder of V-Guard, Wonderla operates four parks spread across 278 acres and enjoys strong brand recall. Despite operating in a ruthless industry, it has leveraged its brand presence, conservative expansions, and cost efficiencies to continue flying higher.

Also read: Down 62% since the IPO, Star Health faces the Irdai test

While it has struggled with stagnant footfall, its park-expansion plans recently boosted investor sentiment. It raised more than ₹500 crore through qualified institutional placement (QIP) in December, primarily to fund its new 64-acre park in Chennai. Management has guided for a strong summer quarter and expansion-led growth in footfall. The stock is up almost 7% over the past month.

Industry has much room to grow

India has the potential for a strong demographic dividend thanks to its young population. Growing urbanisation and rising disposable incomes bode well for businesses catering to discretionary demand, such as the amusement parks.

Amusement parks also boost tourism, and have thus attracted the attention of some state governments. The central government’s push to improve infrastructure and connectivity have also helped make amusement parks more accessible to the masses.

Finally, the low penetration of amusement parks in India leaves ample room for growth. The industry has grown at a compound annual rate of 20% between 2019 and 2024 and is expected to clock 15% growth over the next few years.

But it's a tough nut to crack

Amusement parks have not caught on among India’s premium customers, thanks in part to long queues. This means the industry needs to focus on the masses, making the target customer extremely price-sensitive. This has made it difficult to manage the tug-of-war between revenue growth and profitability.

Add to this the fact that expenses towards land acquisition and ride capex are front-loaded, while the business is seasonal. More than one-third of business is concentrated in the June quarter. The result? Fluctuating profits and cash flows.

Also read: Force Motors is shifting gears—will the rally keep rolling?

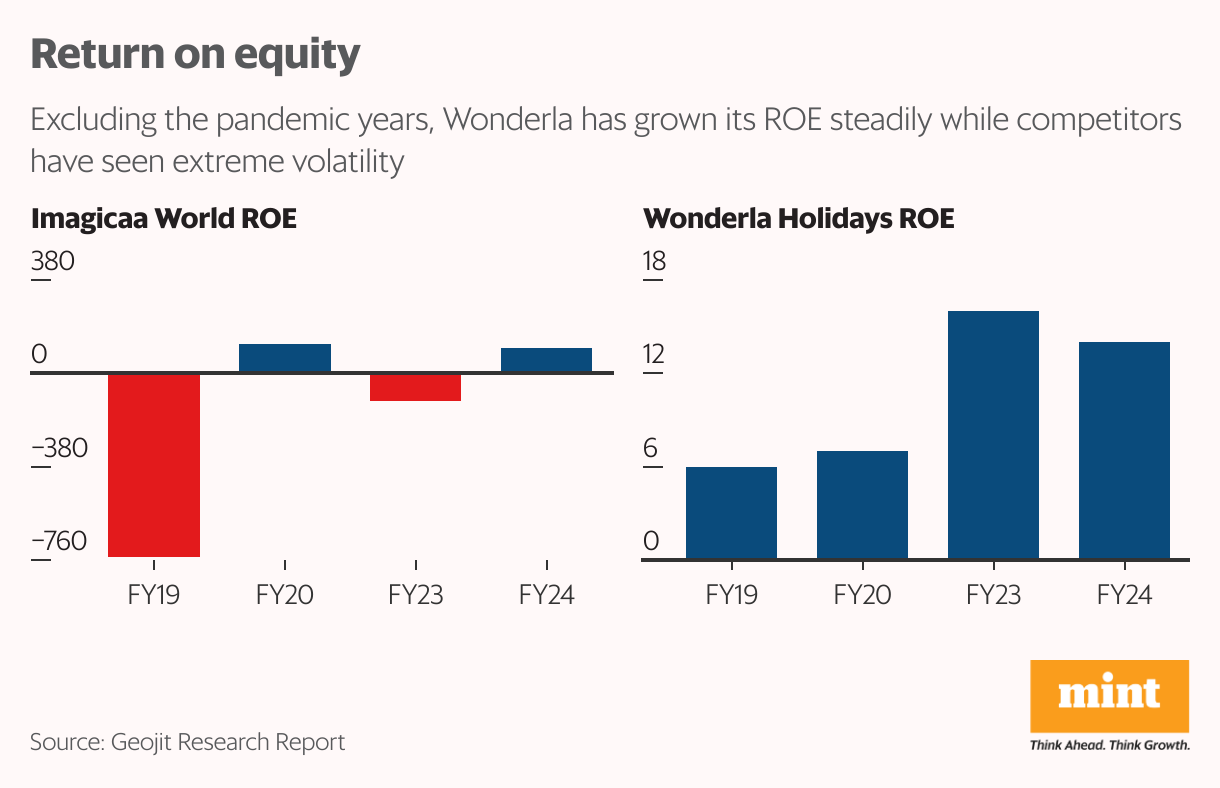

A posterchild for this industry’s ruthlessness is Wonderla’s competitor Imagicaa. Burdened by debt (3.4x debt-to-equity in FY23) and fickle footfall, its profitability and cash flows fluctuated wildly. It had even hung loosely on the brink of bankruptcy before debt-resolution and write-offs recently breathed new life into the business.

Wonderla's secret sauce: Brand recall

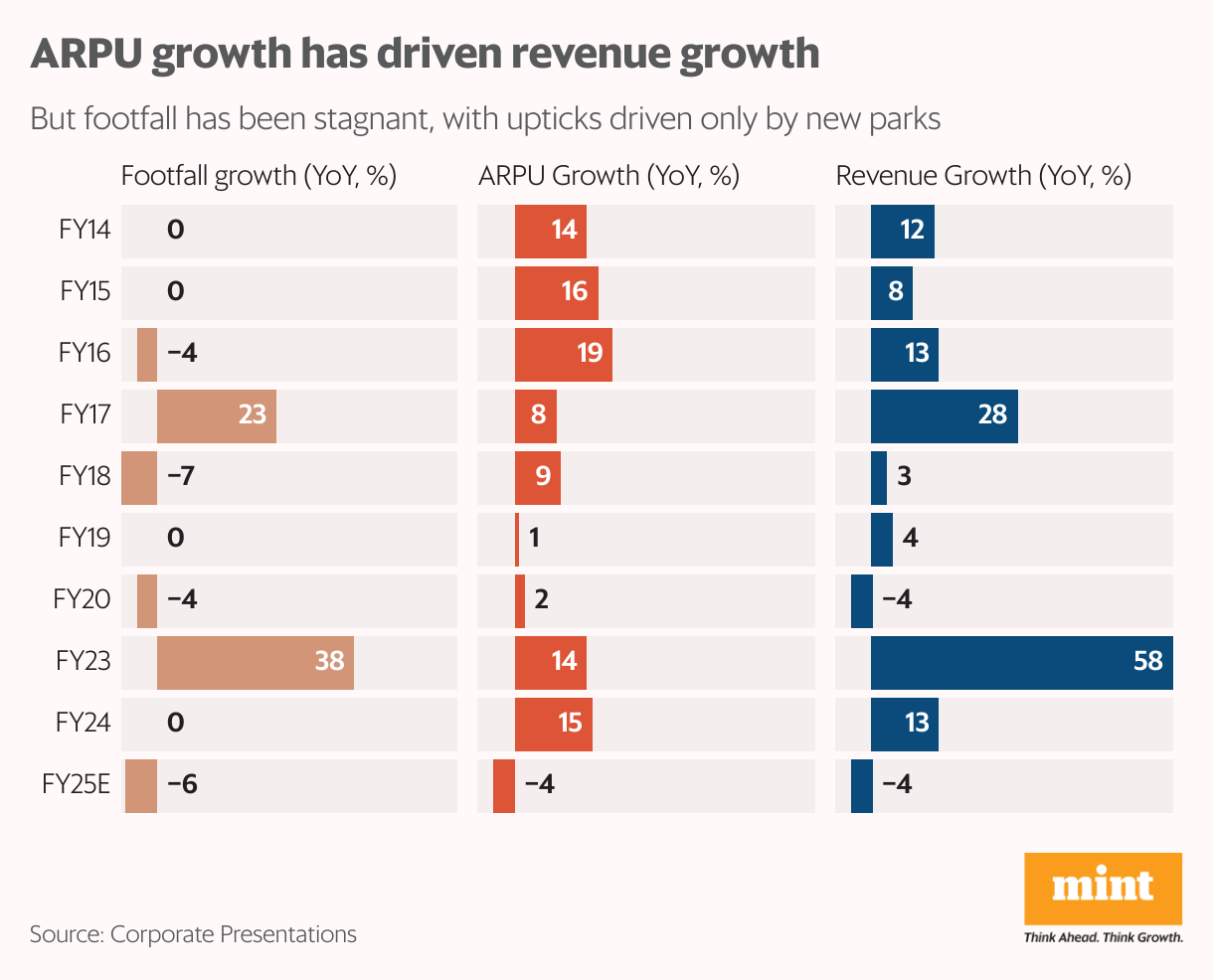

Wonderla recorded a footfall of 3.3 million in FY24, the same as the year before that. It is expected to drop to 3.1 million this fiscal year. Between FY13 and FY25, footfall at Wonderla’s amusement parks has increased at a meagre compound annual growth rate (CAGR) of 2.5%. This is to say that the business typically reports stagnant footfalls, with intermittent spurts following park expansions.

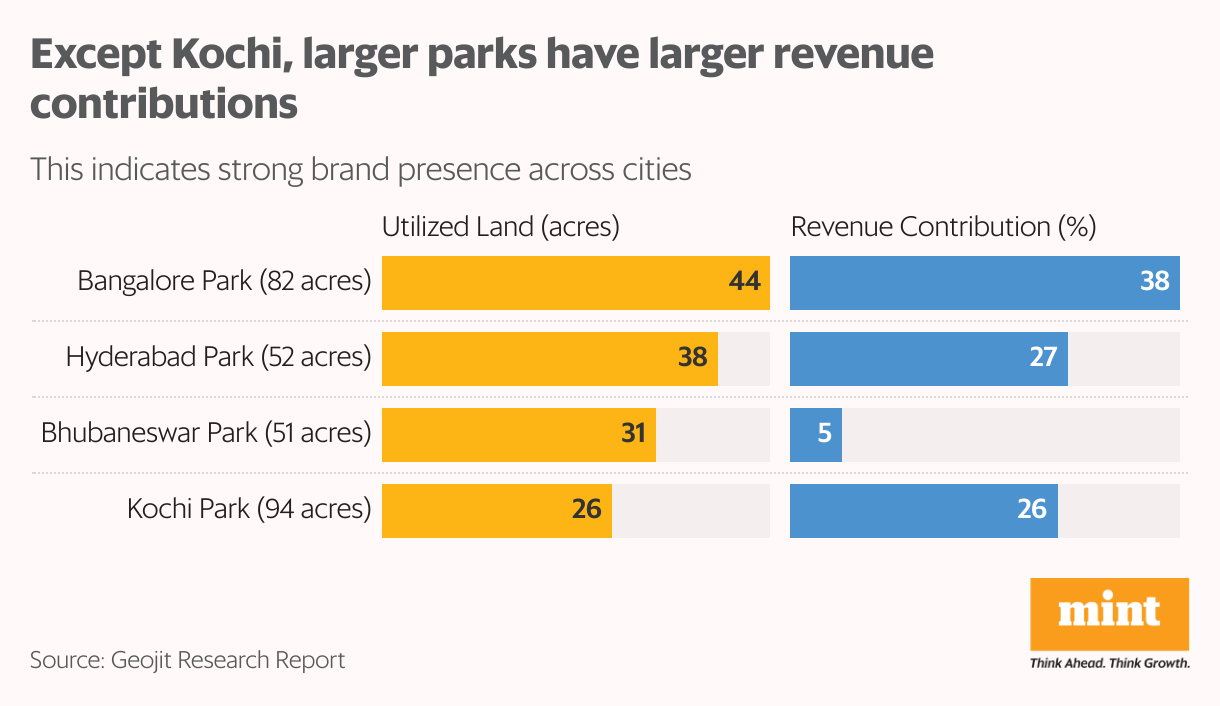

Despite almost flat footfalls, Wonderla has grown revenue at a robust 12% CAGR since FY13. Thanks to consistently strong brand recall across its parks, the higher the utilised area of the park, the larger its contribution to revenues. A strong brand allows it to command increasingly higher average revenue per user (ARPU), which has grown at a CAGR of 11% from FY13 to FY24 ( ₹1,430).

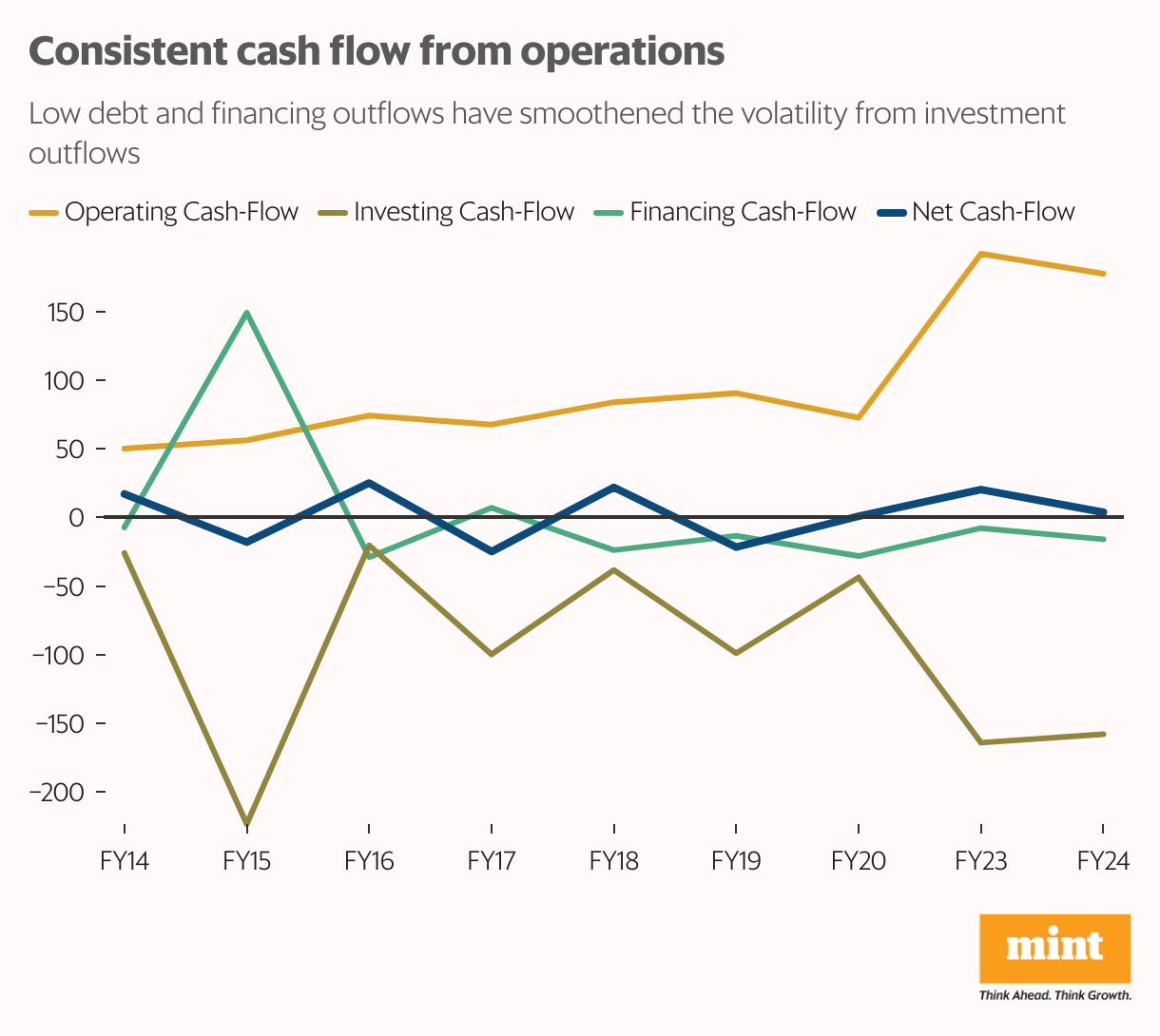

Low debt mitigates seasonal fluctuations

Even though Wonderla’s footfall growth has been driven primarily by park expansion, management has stuck with a conservative expansion plan. Its expansions have been funded largely by internal accruals and raising equity, while debt has been maintained at just 1-2% of its shareholder funds.

Consequent low interest costs have smoothed out some of the cash-flow fluctuations due to seasonal revenues and intermittent expansion. Even with debt-funded expansion plans after FY27, management remains committed to keeping debt low.

Clever with costs

Affordable services are key in the Indian amusement park industry, and costs need to be controlled to protect business margins. Wonderla ensures this by buying large parcels of land at discounts, which also helps it avoid real estate price appreciation from having to buy land incrementally for expansion. About 53% of the land it owns is currently undeveloped, leaving room for low-cost expansion in existing parks.

Also read: Hero MotoCorp has hit a speed bump—can it rebound?

Moreover, for expansion in new areas such as Bhubaneswar, Wonderla has been leasing land from state governments rather than buying it outright. This gives more flexibility, better control over cash-flows, and the potential for faster expansion.

Finally, almost 30% of its rides are assembled in-house, leading to savings on costs and import duties while also allowing for quality control, customised development, and faster innovation and maintenance cycles. Acquiring pre-owned rides from other operators and closed amusement parks has also improved its cost efficiency.

Margins may see medium-term pressure

The next few years should see higher footfall as the Bhubaneswar park gains traction and the Chennai park becomes operational by the end of FY26. Revenue is expected to grow at a CAGR of about 19% between FY25 and FY27.

Over the near to medium term, the expansions will be margin-dilutive as fixed costs including setup and employee expenses accelerate while ARPU takes time to catch up. Going by historical evidence from Wonderla’s park in Hyderabad, the parks in Bhubaneswar and Chennai can be expected to weigh on margins until FY28-29. The Chennai park, given its prime location, is eventually expected to drive revenue growth and profitability by commanding similar ARPUs as the flagship Bangalore park.

Management has guided ₹1,200-1,500 crore of capex over the next two to three years, funded by the recent QIP, debt, and internal accruals. Apart from expanding existing parks, Wonderla also plans to expand its brand footprint beyond south India.

Risks remain

Unseasonal rains and safety incidents could act as dampeners for the business, while delays in expansion could affect revenue growth and profitability.

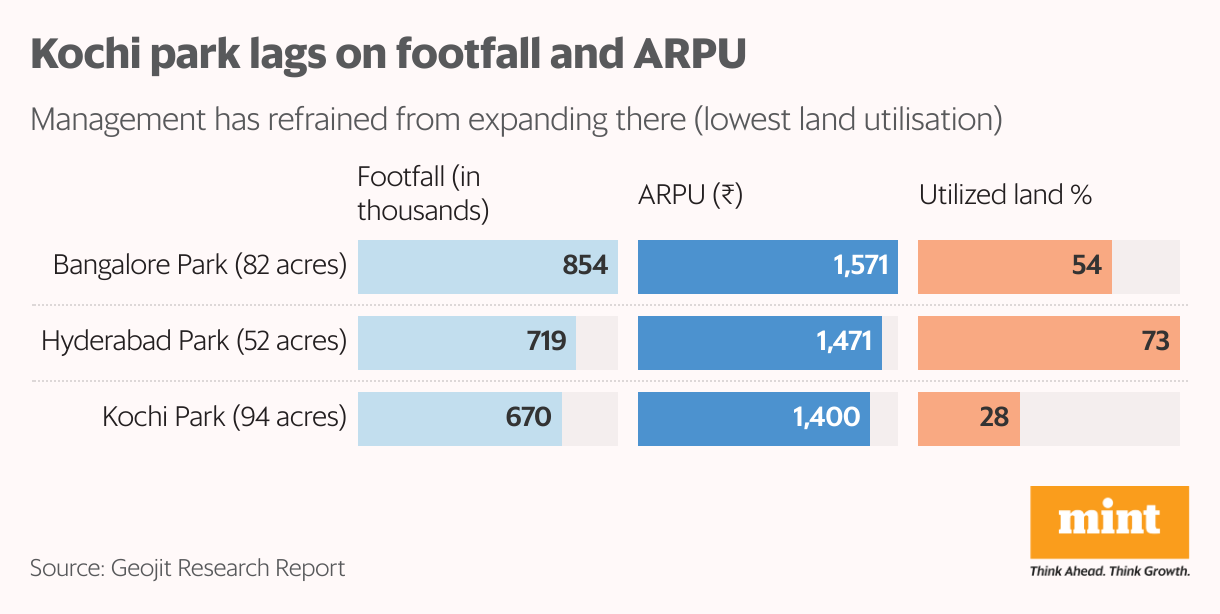

Despite being Wonderla’s first park, Kochi has been lagging. As it trails on footfall and ARPU, management has refrained from expanding the park. Its land utilisation stands at a meagre 28%, well below the 54% and 73% at the Bangalore and Hyderabad parks, respectively. This low land utilisation further drags down Kochi Park’s profitability.

Also read | DLF’s ₹1 trillion bet: Can the real estate major stay ahead of a cooling market?

The Bangalore resort, which contributes 5% of Wonderla’s revenues, has been operating at less than 60% occupancy, which has fallen further to 52% in the nine months to December 2024. The company plans to build similar resorts adjacent to other parks, and a glamping pod expansion in the Bangalore resort. Their appeal among visitors is largely unknown at this point.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.